Life during COVID-19: Financial wellbeing and COVID-19

Key messages

-

In response to the economic impact of COVID-19, Australians are mostly reducing their spending rather than increasing debt. There appears to be a high level of caution with spending, even among those whose income has not changed.

-

The most common financial action taken was to cut down on non-essential expenses. This was followed by reducing spending on essential items such as groceries, and using money saved for other purposes to pay for everyday expenses.

-

Among those who reported a large drop in income, one in seven had asked for a pause on their rent or mortgage payments, one in five had asked for financial help from friends or family, and one in eight had asked for help from a welfare or community organisation.

-

Three out of five respondents said they were at least 'a little concerned' about their current financial situation. Even more people were concerned about their future financial situation, with over 70% at least a little concerned.

-

Financial concerns included coping with job losses and reduced income from employment, businesses or investments; concerns about job security, career prospects and retirement plans; and the financial wellbeing of family members (adult children and family members living elsewhere) and the local community.

I'm now on Job Keeper, there is a big question mark over my business (owned for 13 years).

Female, 42, single-parent household

Changing incomes

Due to the economic impact of COVID-19, many Australians have experienced changes to their employment, including job losses, stand downs and reductions in working hours. As a result, many families have had changes in their income. Families in Australia respondents were asked how their income had changed since COVID-19. Those who were living with a spouse or partner were also asked about changes to their partner's income.1

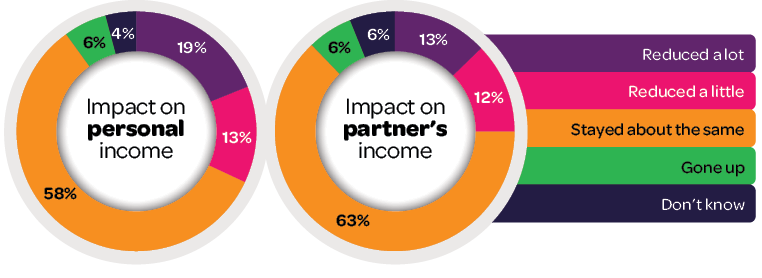

Just over 30% of respondents reported a reduction in their personal income (either a little or a lot) since the start of the pandemic, with 19% saying their income had reduced a lot (Figure 1). Among those who were living with a partner, one in four said their partner's income had been reduced (either a little or a lot), with 13% saying their partner's income had been reduced a lot.

At a couple level, 55% of partnered respondents said that they and their partner had experienced no reduction in income, 18% had either their or their partner's income reduced a little, and the remaining 26% had their or their partner's income reduced a lot (Figure 2). Overall, 61% of respondents had experienced no reduction in their or their partner's income, 16% said that their or their partner's income reduced a little and the remaining 24% said that their or their partner's income had reduced a lot.

Figure 1: Change in own income and partner's income since COVID-19

Note: Weighted estimates. N = 6,696 respondents, 4,740 partners. At the time of the survey, many people were experiencing uncertainty about their job, work hours and income. This, combined with the introduction of the JobKeeper allowance and the JobSeeker supplement, means that it was not unreasonable for some people to be uncertain about how their, or their partner's, income had changed and respond with 'don't know'.

Figure 2: Change in either own or partner's income since COVID-19

Note: Weighted estimates. N = 6,534 respondents, 4,736 couples.

In households with resident children under the age of 18, 49% had experienced a reduction in income, with 30% experiencing a substantial reduction (income reduced a lot).

While reports of income reductions are more common in households with resident children than households with no resident children, this is likely to be at least partly due to age differences between these household types, with more retirees in single-person and couple-only households, while households with children were likely to include working-age parents.

1 In the analysis presented in this report, post-stratification weights (based on age group, gender, state, education and whether the respondent speaks a language other than English) have been used to compensate for bias resulting from over-representation of respondents with certain socio-demographic characteristics. However, it should be noted that the Families in Australia Survey is a non-probability sample and, as such, it is not representative of the Australian population. For further details about the Families in Australia Survey sample, please refer to Hand, Baxter, Carroll, & Budinski (2020).

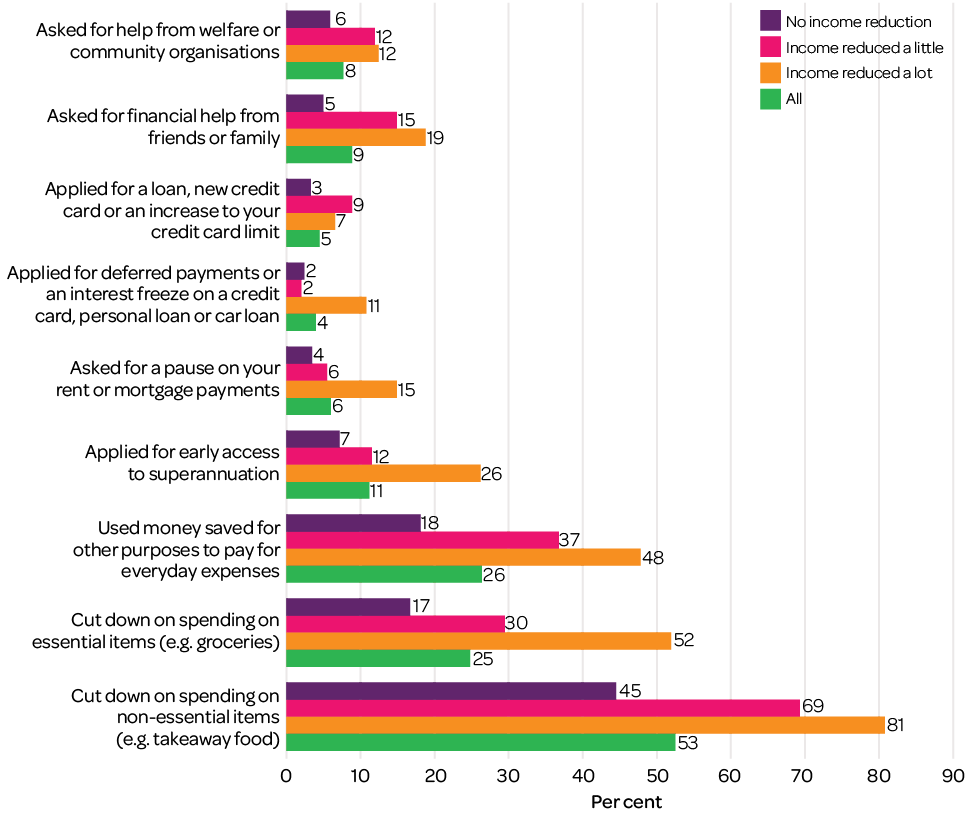

Actions taken due to the financial impact of COVID-19

Respondents were asked if they, or someone in their household, had taken any action in response to the financial impact of COVID-19. See Figure 3 for the full list of actions. Over 60% of all respondents had taken at least one of these actions.

Among those who reported a large drop in in their own or their partner's income, 89% had taken at least one action, and 50% had taken three or more actions. Even among those who had not experienced a drop in income, 54% reported having taken some action in response to the financial impact of COVID-19.

Figure 3: Actions taken in response to the financial impact of COVID-19

Note: Weighted estimates. N = 6,428. Those who did not report a reduction in their or their partner's income may have had other household members (such as adult children) who were impacted financially.

Cutting down on spending

Overall, the most common action taken as a result of COVID-19 was to cut down on non-essential expenses, with over half of all respondents (53%) and over 80% of those who had a substantial reduction in their own or their partner's income saying they had done this.

Don't go out for meals or play the poker machines.

Female, 68, couple-only household

Pretty much all we are spending money on now are groceries, utilities and small amounts of petrol. Female, 44, couple household with children

Some reported cutting down on essential items such as groceries - 30% of those who had a small reduction in income, and 52% of those who reported a substantial drop in income.

Asked for cheaper rate on utilities, delivery costs, not using the car, not using heating.

Female, 31, multiple-adult household

Cut medical and dental. Don't follow-up specialist medical visit.

Male, 62, single-person household

Many reported dipping into money that had been saved for other purposes. Just over a quarter of all respondents and almost half of those who had a large reduction in income said they had done this.

We had been saving towards buying a bigger home for our growing family. We may have to dip into our house deposit savings for everyday expenses at some point down the line now that I have gone on maternity leave and my husband's hours are reduced thanks to Covid-19.

Female, 31, couple household with children

In addition to deferrals on mortgage payments, some banks have announced support packages for their customers that include repayment relief and/or freezing repayments on credit card repayments, personal loans and car loans. Approximately 5% of all respondents said they had applied for a new loan, credit card or increased credit card limit, and 4% had asked for deferred payments or an interest freeze on a credit card or loan. Among those who reported a substantial drop in their or their partner's income, asking for deferred payments or an interest freeze on a credit card, personal loan or car loan was more common (11%) than applying for a loan, new credit card or increased credit card limit (7%).

I applied (and received) an increase to my credit card limit to bring my daughter home from the United Kingdom during the pandemic.

Female, 49, couple-only household

Getting help with housing costs

Around one in seven (15%) of those who reported a substantial reduction in their or their partner's income had asked for a pause on their rent or mortgage payments.

Among those paying rent, other housing-related actions taken, reported in open-text responses, included negotiating a rent reduction from their landlord or asking to defer a rent increase. For those paying off a mortgage, other actions included refinancing their home loan, reducing mortgage repayments or interest rates, changing repayments to interest only, or making only the minimum repayment.

Refinanced home loan to a better rate. Bought shares.

Male, 52, single-person household

Had to suspend school fees and reduce mortgage payment.

Female, 54, couple household with children

Early access to super

One in nine respondents (11%) said that they, or another household member, had applied for early access to their superannuation. Among those who had experienced a reduction in their or their partner's income, one in four (26%) said that someone in their household had accessed their superannuation savings early.

Help from family, friends and welfare organisations

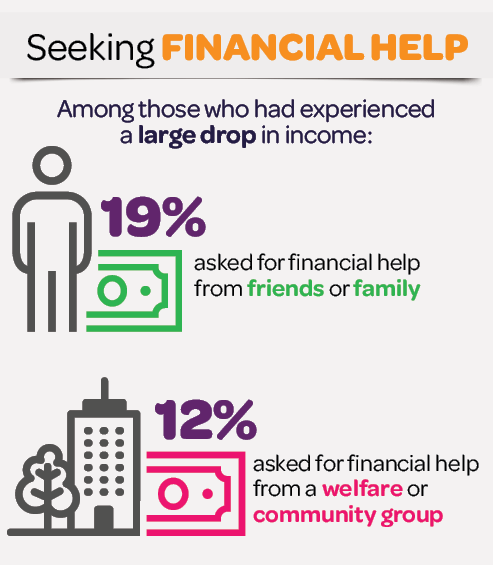

Overall, one in 11 respondents (9%) said they had asked for help from friends or family, and one in 12 (8%) said they had asked for help from a welfare or community organisation. Among those who had experienced a large a drop in income, 19% had asked for financial help from friends or family and 12% had sought help from a welfare or community organisation.

Accepted gifts of food and money from family and friends (didn't ask, but accepted).

Female, 48, couple-only household

Differences in types of financial actions taken

Among respondents who said that they or their partner had experienced a reduction in income (either a little or a lot), the likelihood of taking some of these actions differed by age, and whether or not they had resident children under the age of 18. For example:

- Reports of cutting down on essentials and using savings were less common among those over 40 than among younger people.

- Asking for help from family and friends and welfare organisations was less common among those in households with resident children under 18 - and also less common among respondents over the age of 40.

- Reports of household members applying for early access to superannuation was less common among respondents aged 50-59 than for those in other age groups. This may be because they are approaching the superannuation preservation age where they can access their superannuation savings.

- For other actions, such as asking for a pause on rent or mortgage payments and cutting down on non-essential spending, there were no significant differences according to age or the presence of children in the household.

Actions of older Australians

The financial impact of COVID-19 has created particular challenges for older Australians. For retirees, actions taken were mainly related to changes to pensions and superannuation, including reducing superannuation drawdowns and applying for the Age Pension and concession card.2

Reduced partner's super pension payment so don't have to withdraw super funds for next 6 months or so.

Female, 53, couple-only household

Superannuation loss affected our self-funded retirement plan.

Female, 62, couple with resident children over 18

Applied for Commonwealth Health card due to change in deeming rates.

Male, 69, couple-only household

Reduced our super-based pension payments to 2% from 4%.

Male, 69, couple-only household

If my husband hasn't regular casual work we will need to apply for Govt. pension for both of us. We don't have very much superannuation left.

Female, 66, couple-only household

Other actions taken

Those who said they had taken other actions, not listed in the survey, in response to the financial impact of COVID-19 were asked to describe the types of actions they had taken. These responses varied depending on whether or not they had experienced a drop in income.

Among those who had experienced a reduction in their or their partner's income, commonly reported actions included:

- applying for JobKeeper or JobSeeker payments

- arranging payment plans for electricity and gas bills

- requesting reductions in school fees

- suspending health insurance payments

- consolidating other debts at a lower interest rate

- delaying or cancelling major purchases such as cars and renovations

- consulting with an accountant, financial planner or their bank.

Among people who had not experienced a drop in income, many reported saving money on child care fees, petrol and eating out. While some reported making changes to their savings and investments, financial actions taken as a result of COVID-19 were commonly aimed at helping their family or their community.

I have saved money on things like fuel and entertainment but have tried to reinvest this into local businesses to keep them afloat, e.g. cafes.

Female, 45, single-parent household

I am aware that we are very lucky to have higher incomes, but I don't have a huge sense of job security as I work in the not-for-profit sector and we are anticipating taking a hit in our funding. We have probably spent more money during this period, as we have tried to support local business in buying takeaway food once a week (for example, which we don't normally do).

Female, 41, couple household with children

Australians reducing spending

Overall, these results suggest that, in response to the economic impact of COVID-19, Australians are mostly reducing their spending rather than increasing debt. There appears to be a high level of caution with spending, even among those who have not had a reduction in their own or their partner's income.

We have cut down spending significantly in case we lose our jobs over the next two years. We also have been giving money to family members to help them.

Female, 30, couple-only household

We are spending our savings to get by. It's stressful but we are people who always have a rainy day fund.

Female, 35, couple household with children

2 As part of the government stimulus package in response to COVID-19, two key measures were introduced to help retirees manage the financial impact of COVID-19. The minimum required pension drawdown rates have been halved for the 2019/20 and 2020/21 financial years. This means that retirees can reduce the amount they draw down from superannuation accounts, so they do not have to withdraw those assets at a time when their value is reduced. Depending on age, there is a minimum amount that must be withdrawn as a pension payment from an account based pension each financial year. Pre-COVID, the percentage drawdown required ranged from 4% for people aged under 65 to 14% for people aged 95 and older. (see www.ato.gov.au/rates/key-superannuation-rates-and-thresholds/?page=10). Deeming rates for age pensions (the assumed return on financial assets for the purpose of the income test) were also reduced. For some, this has resulted in increases in pension payments; and among those who were not previously eligible for a pension, some are now able to receive a part-pension and a concession card.

Concern about family financial situation

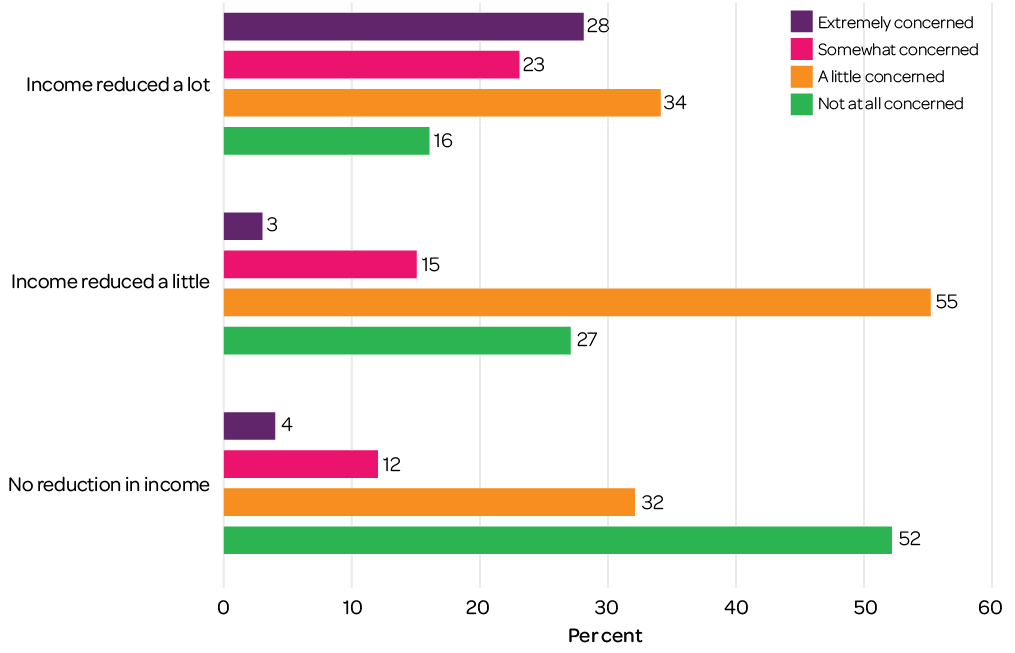

When asked about their level of concern about their family's current financial situation, three out of five respondents said they were at least 'a little concerned' (36% said they were a little concerned, 15% somewhat concerned, and 10% were extremely concerned).

Of course, those whose income had been reduced as a result of COVID-19 expressed higher levels of concern than those who had not experienced a reduction in income. Among those who reported that their or their partner's income had been reduced a lot, almost 30% said they were extremely concerned about their family's current financial situation (Figure 4). But even among those who had not experienced a drop in income, around one in six reported being at least somewhat concerned.

Figure 4: Concern about family's current financial situation, by change in income

Notes: Weighted estimates. N = 6,390. 'Income reduced a little' and 'Income reduced a lot' refer to reported change in own or partner's income.

Compared to concerns about their current financial situation, people were more concerned about their future financial situation, with over 70% at least a little concerned (39% a little concerned, 18% somewhat concerned and 15% extremely concerned).

Among respondents who had experienced a large drop in their or their partner's income, one in three reported being extremely concerned about their family's future financial situation (Figure 5). For those who reported that their (or their partner's) income had dropped a little, levels of concern were not as high, with 55% saying they were a little concerned, 18% somewhat concerned and 8% extremely concerned. Even among those who reported no reduction in income, over 60% were at least a little concerned, and around one in four were either somewhat or extremely concerned about their family's future financial situation.

Comments in the survey indicated that concerns about their family's financial situation go beyond concern for themselves and their partner. They included concern about the financial situation of adult children living at home and family members living elsewhere; and ranged from feeling lucky to not have been impacted financially to issues faced by those who have experienced job loss or a drop in income from employment, businesses or investments. There were also comments about the impact on retirement plans and concerns about job security and career prospects (Figure 6).

Figure 5: Concern about family's future financial situation, by change in income

Notes: Weighted estimates. N = 6,369. 'Income reduced a little' and 'Income reduced a lot' refer to reported changes in own or partner's income.

Figure 6: Impacts of COVID-19 on financial wellbeing

My partner's business will not recommence until the borders reopen. Job Keeper has made a huge difference to us. We are concerned that if Job Keeper is stopped after six months, the business will not survive and he will be out of work.

Female, 34, couple household with children

The uncertainty is a killer. I was feeling rather smug as my partner is in construction and I thought that was a protected industry as they can at least go to work. Then he and 100 in his company are made redundant. No notice. I don't feel so smug anymore. I thought perhaps if two of us were working (me at reduced but still working) that we could buy a home to capitalise on the expected fall in prices. That was just yesterday, today we have no hope and if he can't get a new job we will likely never have any hope of owning a home.

Female, 39, couple household with children

We are stressed about future work/income for me at the end of maternity leave (if I will be made redundant or have salary cut) and also how to manage child care for a baby starting day care when I return. We also have been relying on me going back to work to buy a new home as we currently have 2 children in a 2-bedroom apartment and experiencing difficulty with lack of space.

Female, 36, couple household with children

We are in a generation where superannuation was not compulsory so our saving time, while could have been all our lives, was not as possible. Wages weren't as high even when well qualified but then again housing wasn't as expensive. I think this time has just highlighted for me…the fragility of life and how important it is to have financial security. This is particularly frightening when I see our limited savings diminish before my eyes.

Female, 69, couple-only household

Reference

- Hand, K., Baxter, J., Carroll, M., & Budinski, M. (2020). Families in Australia Survey: Life during COVID-19 Report no. 1: Early findings. Melbourne: Australian Institute of Family Studies.

About the survey

Life during COVID-19 was the first survey in the Families in Australia Survey (AIFS' flagship survey series). The first wave ran from May 1 to June 9 2020, when all states were in various stages of lockdown. There were 7,306 respondents. A second survey wave is planned for November 2020.

Contact

For more information, visit the Families in Australia Survey project page or email [email protected].

© GettyImages/BraunS

Warren, D., Baxter, J., & Hand, K. (2020). Life during COVID-19: Financial wellbeing and COVID-19. (Families in Australia Survey report). Melbourne: Australian Institute of Family Studies.

11 November 2020

Download Research report

Related publications

Life during COVID-19: Early findings report

This report contains early findings from a major survey that ran May-June 2020, exploring how Australian families coped…

Life during COVID-19: Help and support

This report looks at how we helped, and were helped by relatives, friends, community groups and professionals during…

Life during COVID-19: Staying connected when we're apart

This report focusses on how Australian families stayed connected when physically separated during the COVID-19 pandemic.