Child Care Package Evaluation: Final report

Executive summary

Child care plays an important economic and social role in Australia. For parents, it supports their participation in employment, education and training. For children, quality care can support child development, particularly for vulnerable and disadvantaged children and their families. In recognition of its importance, child care in Australia is substantially subsidised by the Australian Government via fee subsidies and some specific direct funding to some services. Child care services are regulated in relation to quality and other aspects of their operation.

In July 2018 the Australian Government introduced the 'Child Care Package' as a significant reform to child care provision and funding. It involved a major restructuring of subsidies and a range of other measures, and significant additional government expenditure. The core objectives of the Package are to support families to be able to access quality early learning, enable and encourage greater workforce participation and simplify child care payments, and targeting assistance to low and middle income families. Its goal was for child care to be 'simpler, more affordable, more accessible and more flexible'.

The new Child Care Package has 2 key elements:

- Child Care Subsidy (CCS) - this is the main form of Australian Government financial support to parents as a subsidy for child care costs. Key elements of this are: a subsidy paid as a proportion of the cost of care up to an hourly fees cap with the rate tapering, from 85 per cent, with increasing income, and with the total value of subsidy capped for some households; along with limits on the number of hours of care for which the subsidy is paid, determined by the level of parents' participation. The subsidy is usually paid to the service as an offset to the fee that would otherwise be paid by the parent.

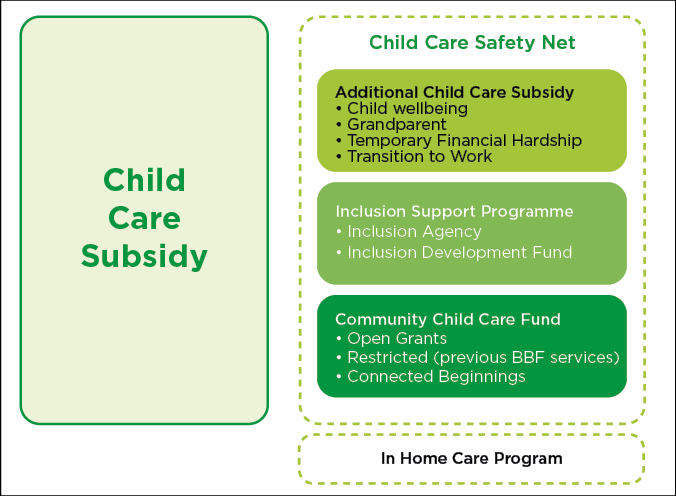

- The Child Care Safety Net comprising:

- Additional Child Care Subsidy (ACCS) - additional fee assistance directed at families and children who may face barriers in accessing affordable child care

- Inclusion Support Program (ISP) - support for services to build their capacity and capability to include children with additional needs in mainstream services

- Community Child Care Fund (CCCF) - grants to child care services to help them address barriers to participation and to support service sustainability, and for services in areas of high unmet demand.

It also involved regulatory change, a new IT system and the incorporation of some 'Budget Based Funding' (BBF) services into the main child care system.

Prior to the Child Care Package, there were 2 main forms of child care assistance for parents: Child Care Benefit (CCB) and Child Care Rebate (CCR); along with a range of complementary programs addressing children with additional needs, and families with barriers to access and services.

The Australian Institute of Family Studies, ANU Centre for Social Research and Methods, UNSW Social Policy Research Centre and the ANU Social Research Centre were commissioned by the Department of Education, Skills and Employment ('the Department') to undertake an evaluation of the new Child Care Package ('the Package'). The evaluation commenced in December 2017 prior to the introduction of the Package in July 2018.

The evaluation primarily considers the impact of the new child care subsidy system (comprising the Child Care Subsidy (CCS), Additional Child Care Subsidy (ACCS) and the Community Child Care Fund (CCCF). It also covers the Inclusion Support Program and the In Home Care Program, which are subject to separate reporting, with some findings synthesised into this overall evaluation.

The evaluation drew heavily upon the administrative data on the children's and families' use of child care along with surveys implemented by the Department and by the evaluation team, as well as extensive qualitative data from consultations and location-based case studies. It also drew upon contemporary literature and data published by the ABS and others.

The evaluation was impacted by external events, particularly COVID-19, which resulted in the suspension of the child care funding system for a period during 2020. As a result, the evaluation only draws on data to the end of 2019 and does not include data from 2020 as originally intended. We, however, consider that the elements of the Package were sufficiently implemented, and the evaluation had collected adequate information, to enable conclusions to be drawn on the program outcomes and impacts.

Use and provision of child care

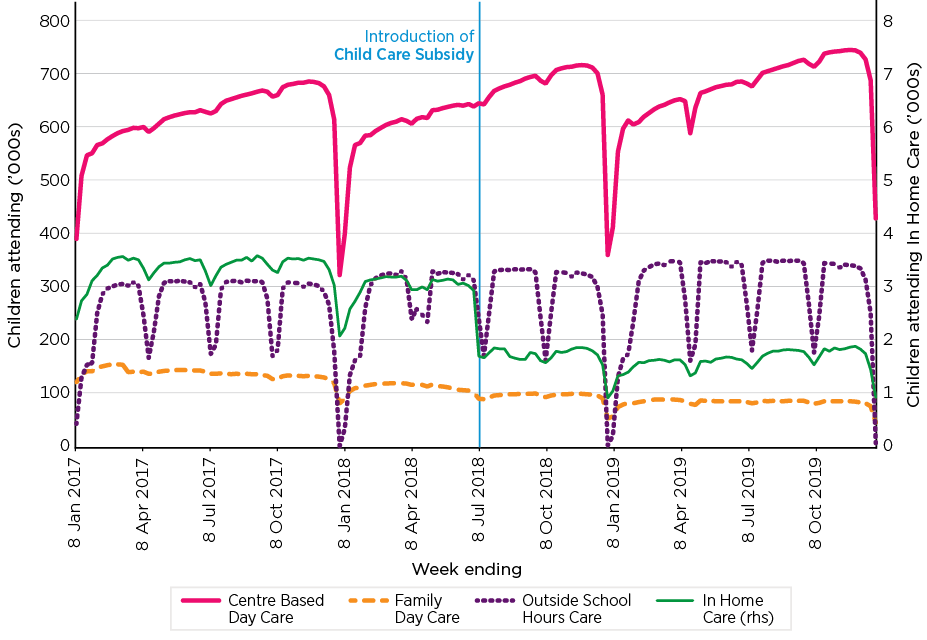

- In the December quarter 2019 over 1.3 million children from 933,648 families used a child care service in Australia provided by 13,118 child care services. Of these services 61.8 per cent were Centre Based Day Care services, 34.4 per cent were Outside School Hours Care services, 3.5 per cent were Family Day Care Services and 0.3 per cent were In Home Care services.

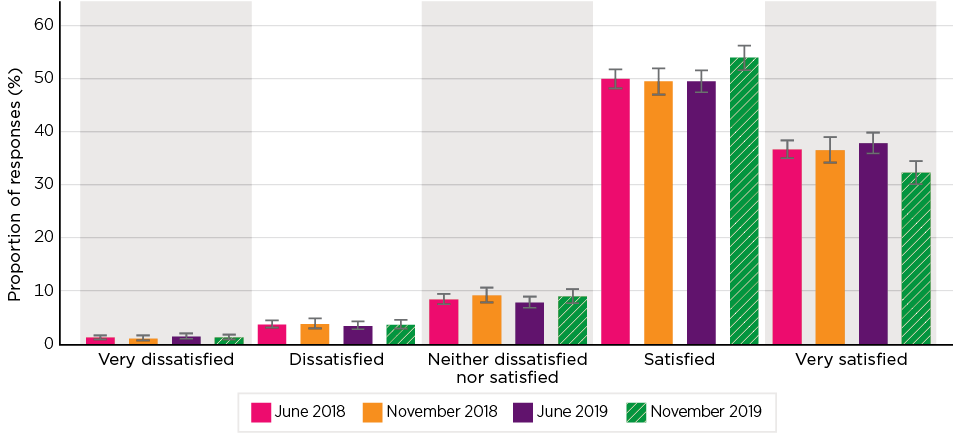

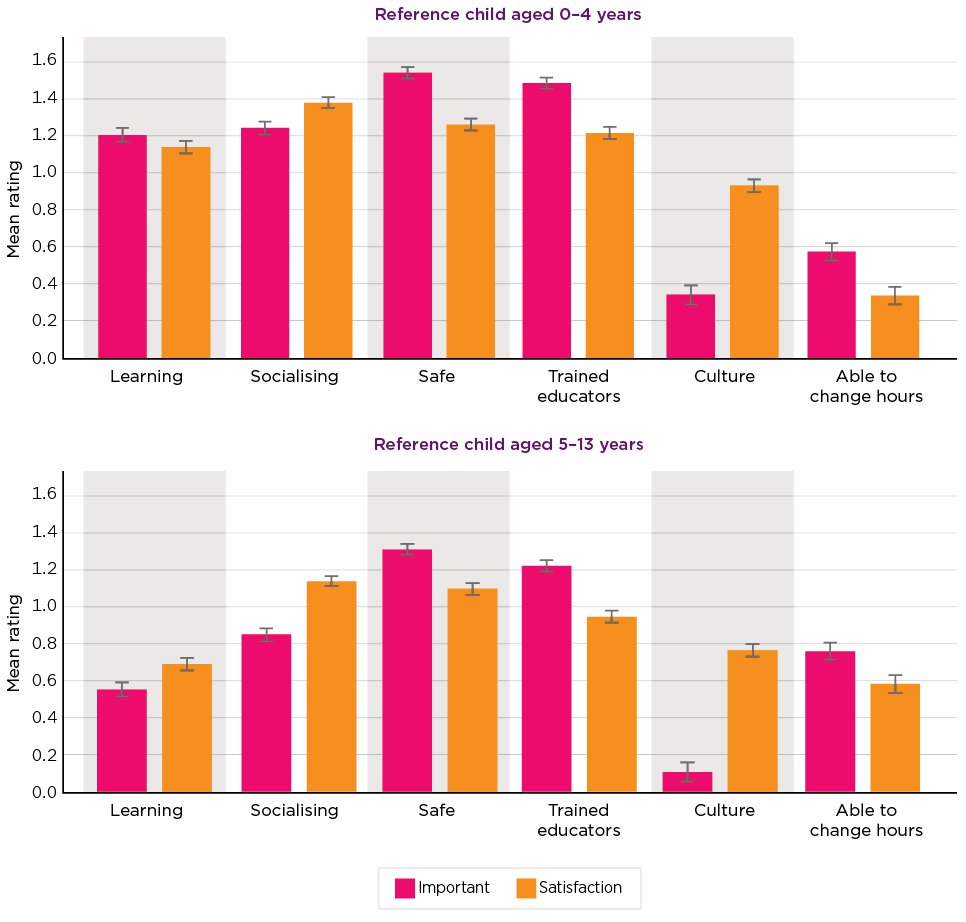

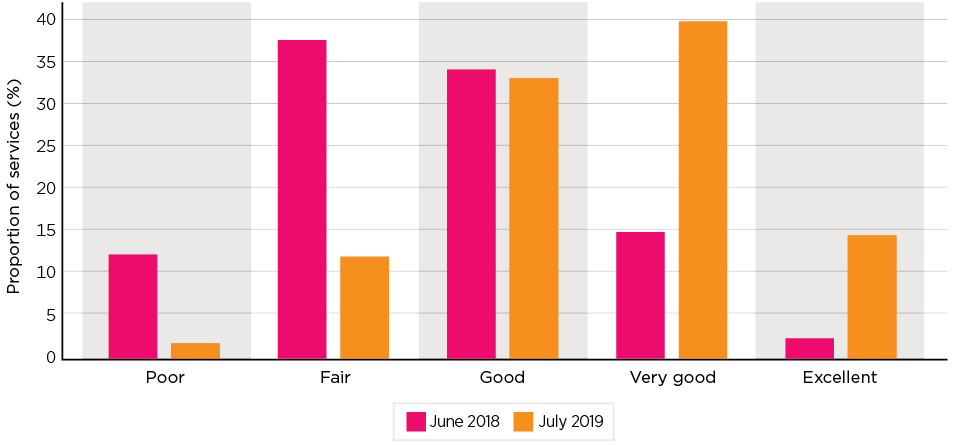

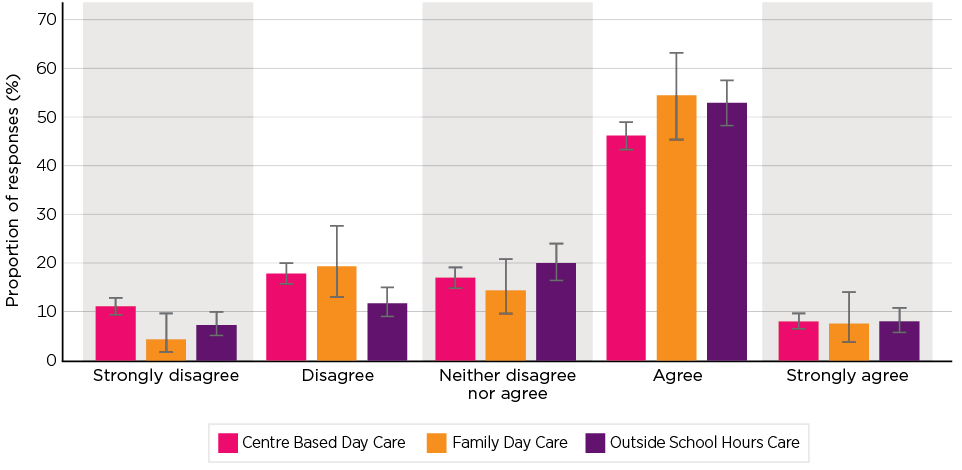

- Overall, parents have a relatively high level of satisfaction with the quality of child care, with around half stating that they were 'satisfied' and a bit over a third saying they were 'very satisfied'. There was no change in parental satisfaction with the quality of child care with the introduction of the Package.

The evaluation assesses the Child Care Package against 4 key outcomes and 3 key impacts that reflect its policy objectives. In addressing these the evaluation has largely adopted a comparative focus; that is, whether the Package has had any positive or negative impacts relative to outcomes under the previous funding arrangements.

Outcome 1: Child care services are accessible and flexible relative to families' needs, including disadvantaged and vulnerable families

Accessibility

- Access to child care has several dimensions including quality and cost. While access and flexibility for all families is considered, a particular focus is on outcomes for children from more vulnerable groups.

- Analysis of data at the time of the implementation of the CCS and the following 18 months shows no marked changes in access to child care. There are though large differences in access geographically, and issues for children with additional needs.

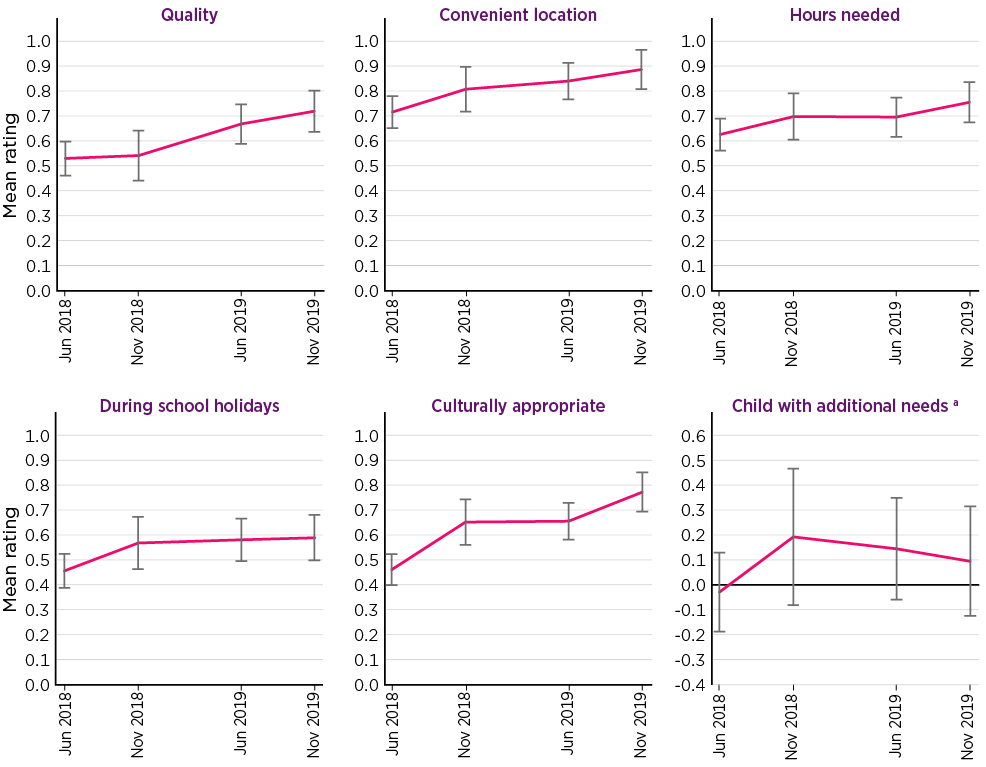

- Parents generally had a positive view about the accessibility of child care. There was an increase in the satisfaction of parents with a child aged 5-12 years using care with regard to ease in finding quality child care and with child care in a convenient location but not across other measures. For parents with a younger child in child care - that is, for the main group of parents - there was no improvement in satisfaction.

- Some parents report having greater difficulties in accessing child care for children with additional needs. There is also evidence that exclusionary practices within the child care sector are impacting access.

Flexibility

- As part of the Package, regulatory requirements related to the hours and days services must be open and some other regulatory requirements that limited flexibility were removed. Services were encouraged to look at more flexible offerings, including shorter sessions, in response to these changes, and the limits on subsidised hours of care provided under the CCS.

- There are mixed levels of parental satisfaction with flexibility. Capacity to change hours received the second lowest parental satisfaction rating (only above affordability). Other aspects of flexibility were more neutrally rated by parents. These ratings have not changed following the introduction of the Package.

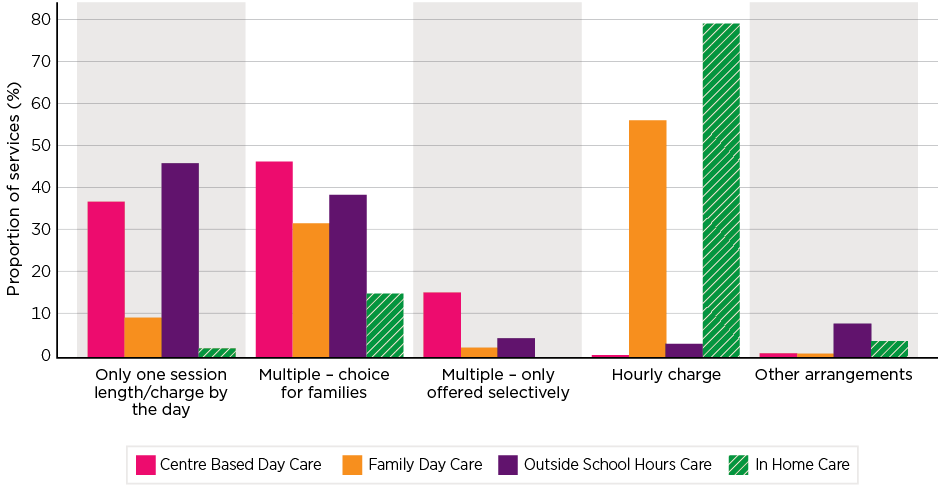

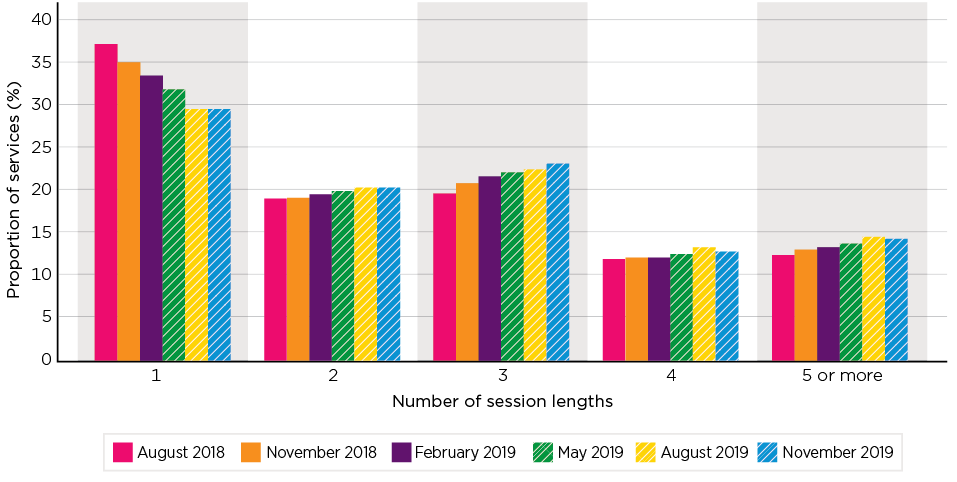

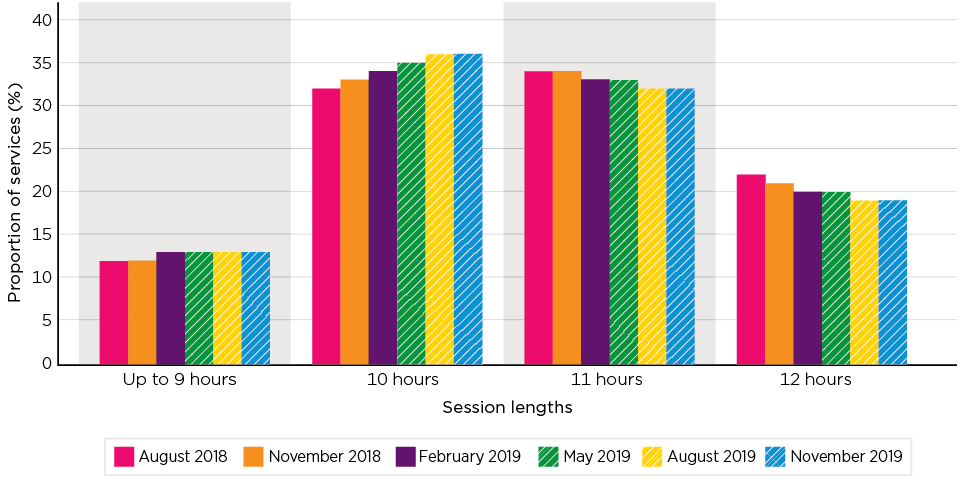

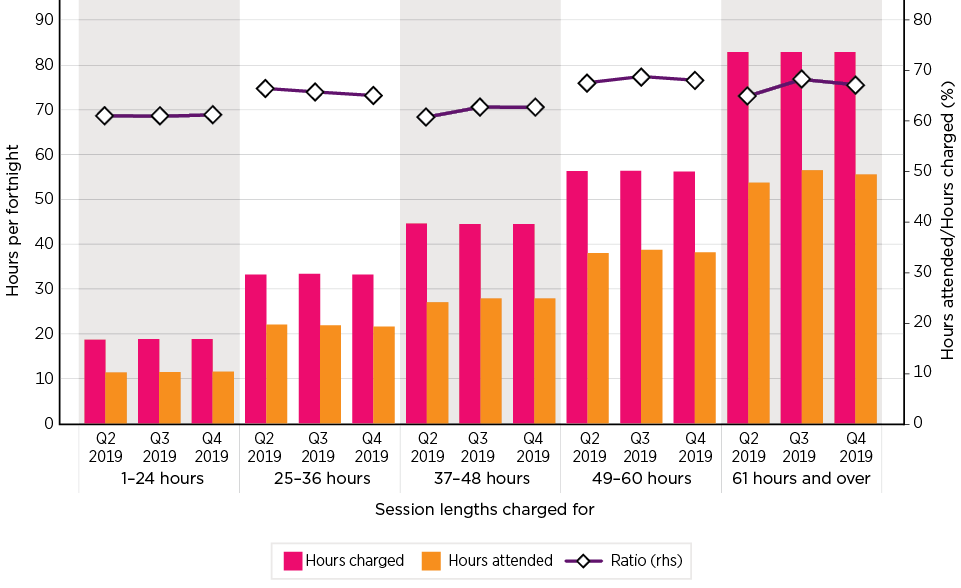

- There was little change in the hours for which care was available since September 2018. Within the Centre Based Day Care sector there has been some shift to services offering shorter sessions and multiple sessions in a day. About one in 20 children are using shorter sessions following the changes, and only 2.2 per cent of children are using 6-hour sessions. Analysis, however, suggests that much of this change has been designed to work around the structure of the CCS to maintain revenue and limit parents' costs, rather than representing any real change in provision. Where shorter sessions have been introduced, they often have fixed and limited start and end times.

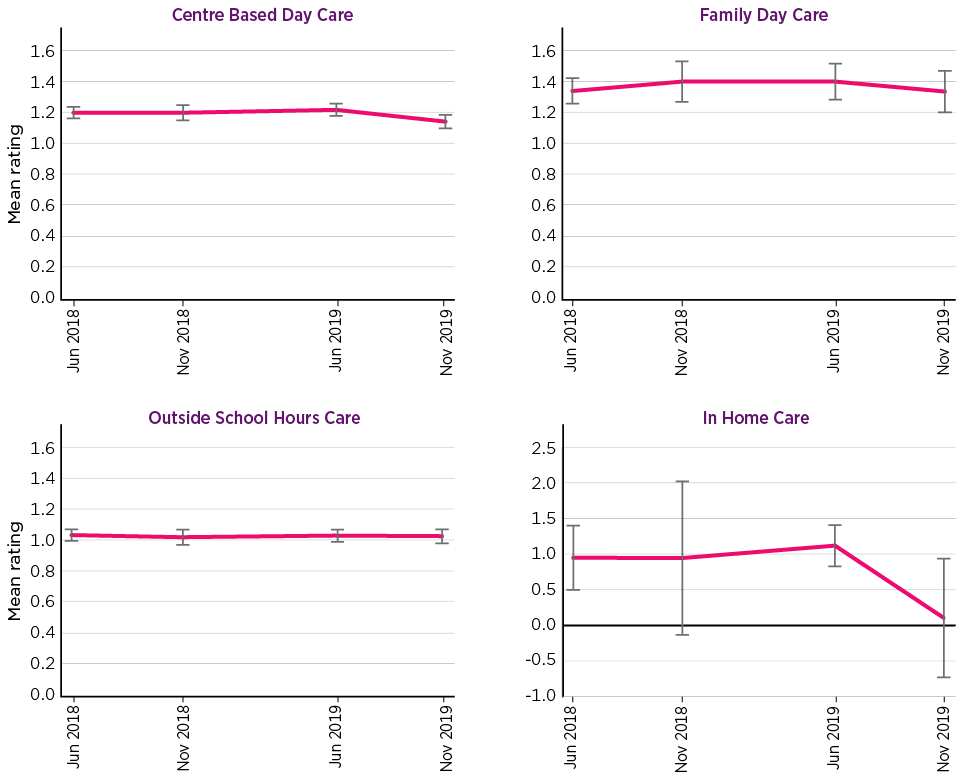

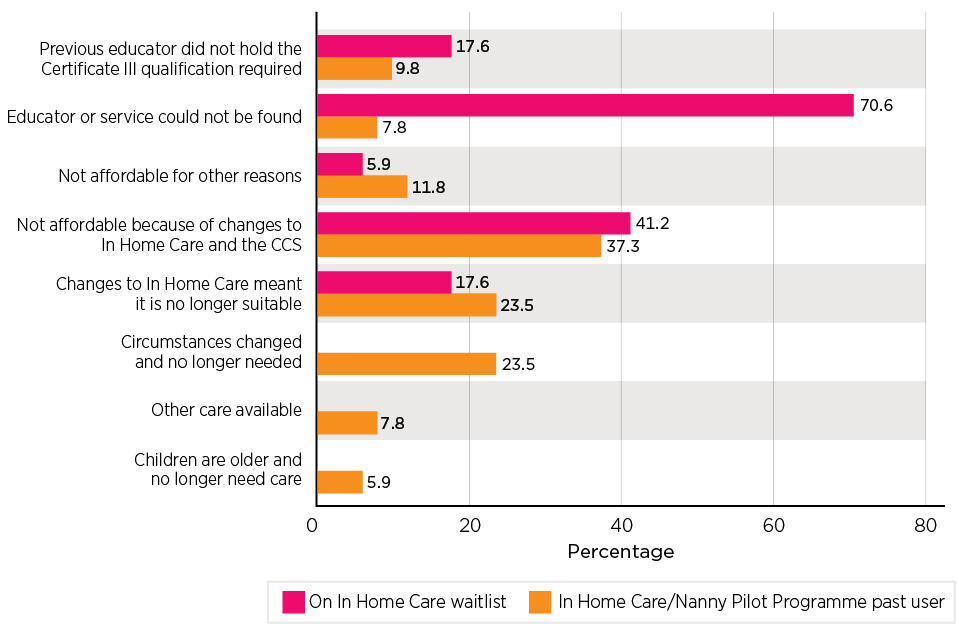

- In Home Care does provide a form of flexible care to families, and there is a high degree of satisfaction with In Home Care among those who use it. But there have been challenges with the program, particularly related to the availability of suitably qualified educators. The Family Day Care sector also has the capacity to deliver flexible care.

- The key barriers to providing more flexibility in child care are economic. The failure of services to respond to the demand for these types of flexible care largely reflects the costs involved.

In summary, the introduction of the Child Care Package has had little impact on the accessibility or flexibility of child care provision. There is though considerable variability in experiences of access to child care, and barriers to access for some children, particularly those with additional needs whose access may be affected by exclusionary practices by services. These exclusionary practices warrant further investigation to better understand the extent of them, as well as their cause and impact.

Outcome 2: Access to child care support is simple for families and services

- A key feature of the Package was the replacement of the 2-part, CCB and CCR, subsidy arrangement with the single CCS. This was accompanied by regulatory changes for services to reduce some constraints and streamline processes, along with a new IT system. These were all seen as elements that would improve the simplicity of the provision of child care support. At the same time, more detailed activity testing and the use of Centrelink for all access to subsidies can make the system more difficult to navigate. The system has become simpler for some and more complex for others.

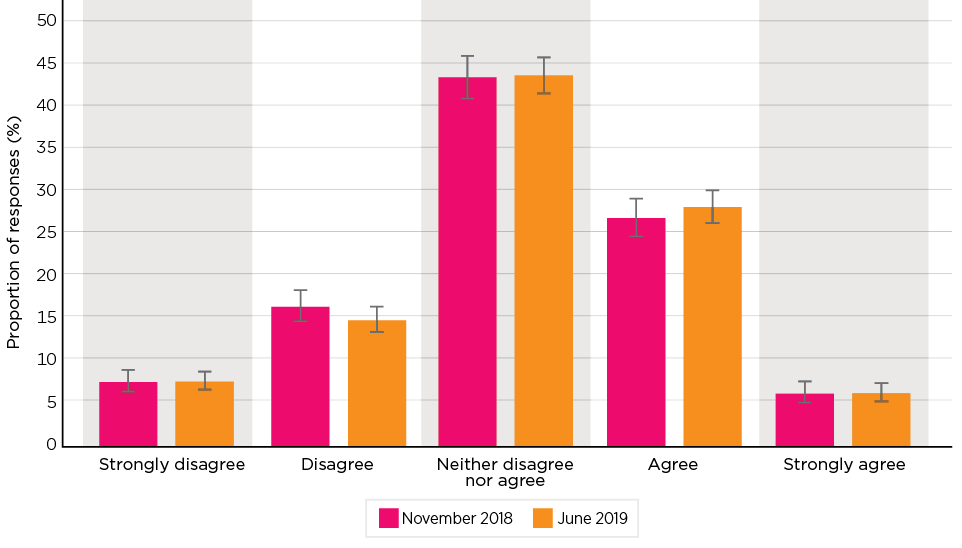

- Parents were only weakly supportive of the system being easier to understand than the previous system, with the largest group neither agreeing nor disagreeing that the CCS system is simpler. Low to middle income earners were more likely to see the new system as being simpler than those on higher incomes.

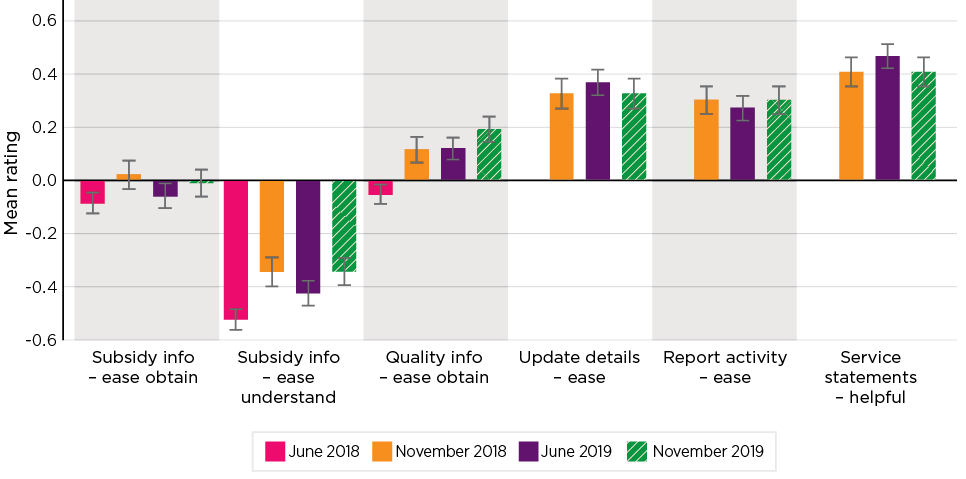

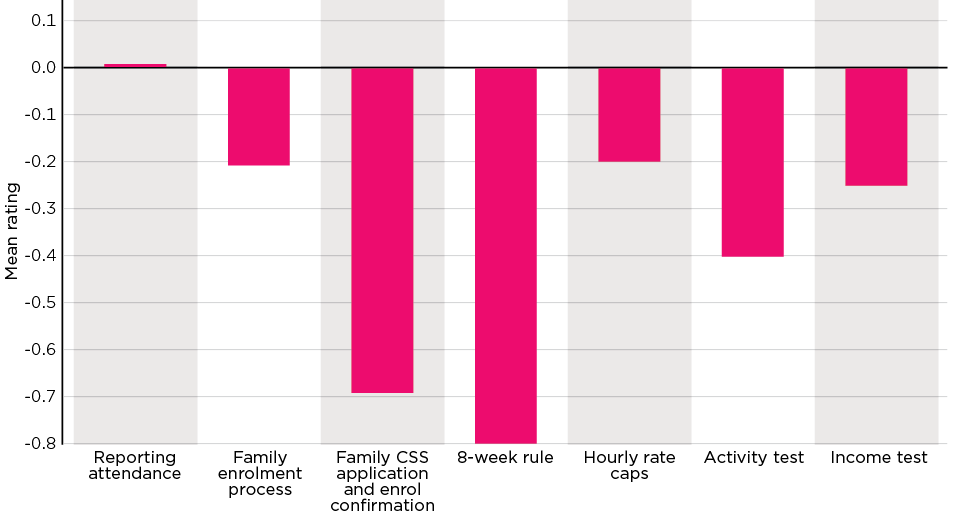

- For most people, the processes operate relatively smoothly. However, when issues arise, resolution of these are reported as being difficult. Two specific issues had prominence in responses to the evaluation data collections. The first was the 2-stage process associated with agreeing: the Complying Written Agreement and then confirming the enrolment. The second was the operation of both the DESE Helpdesk and Centrelink Helpdesk, with strong negative feedback on these including tardiness and issues not being resolved. There were also concerns raised about the functionality and ease of use of the Centrelink calculator relative to that produced by DESE prior to the transition.

Outcome 3: Child care is affordable to families especially those with limited means

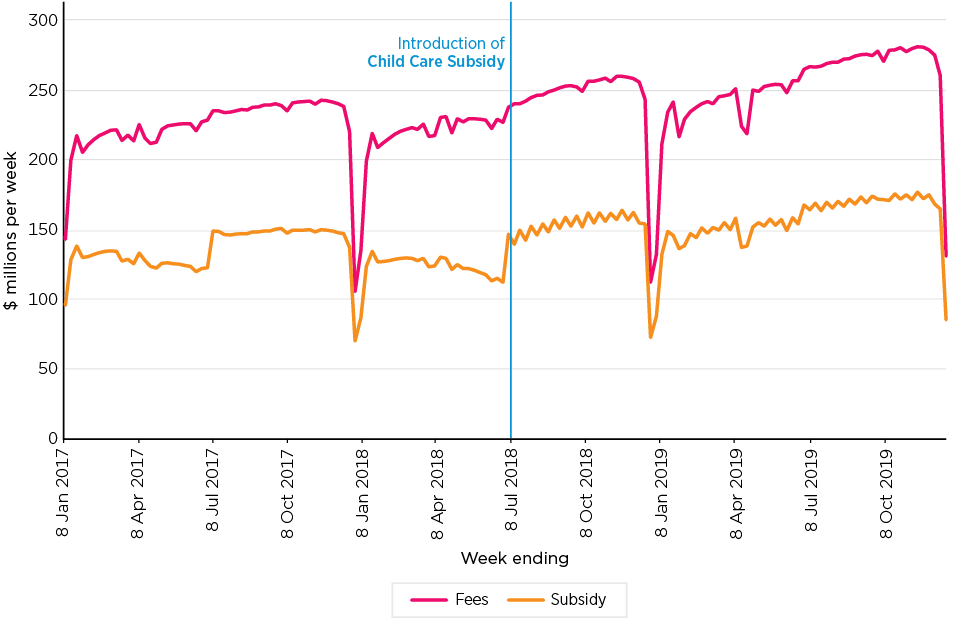

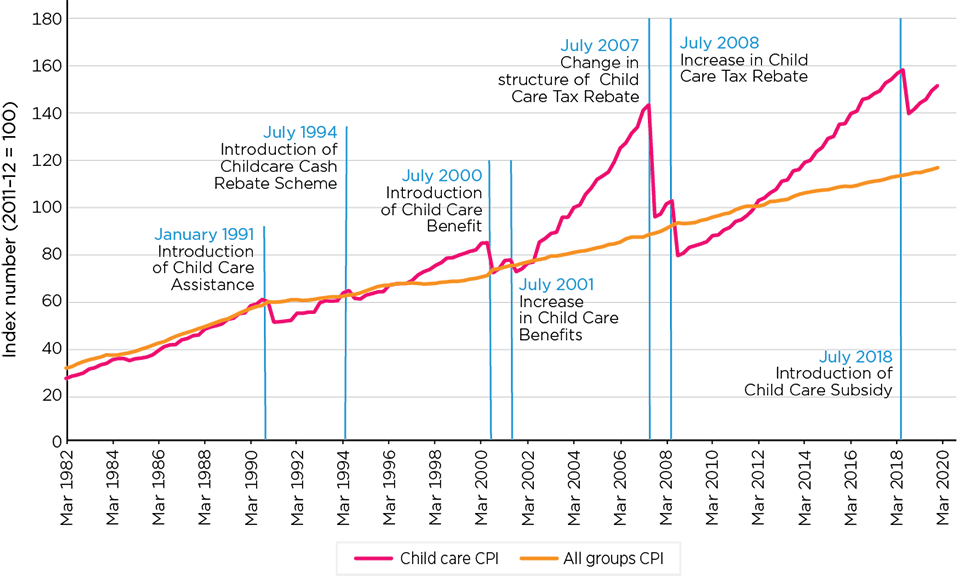

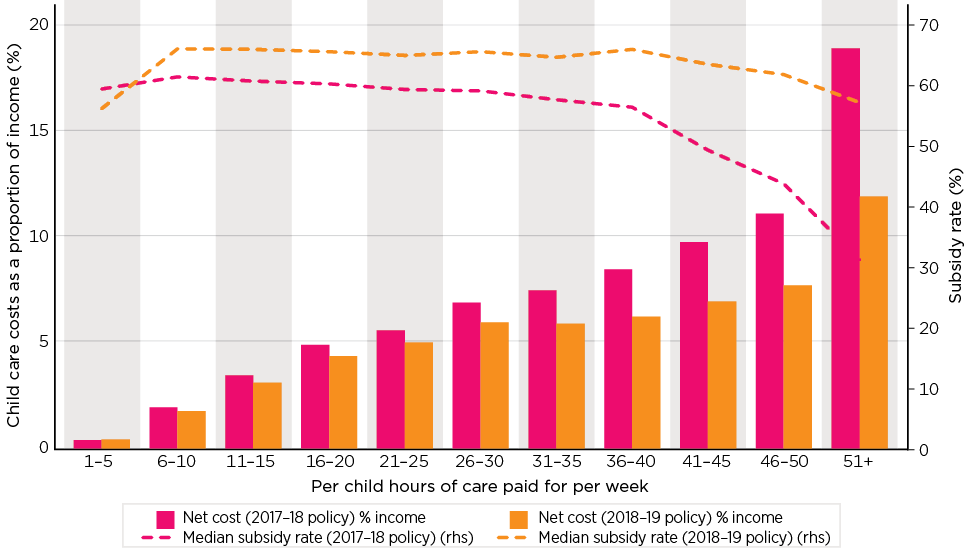

- Improving affordability of child care for low and middle income families was central to the Child Care Package, with the new CCS also including a taper reducing, and then ceasing, the payment of subsidies to high income earners, along with a cap on subsidies for some. The hourly fees cap, indexed by CPI, limited the level of subsidy and was seen as a means of putting downward pressure on fees. The shift to the CCS is estimated to have resulted in additional government expenditure of 6.3 per cent or $453 million in 2018-19 as compared to what would have been spent under the previous system.

- There had been a long history of government interventions to reduce the cost of child care as measured by the CPI. These historically, while reducing the cost in the short term, did not impact the long-term trend, with the cost of child care trending well above the CPI but consistent with trends in earnings.

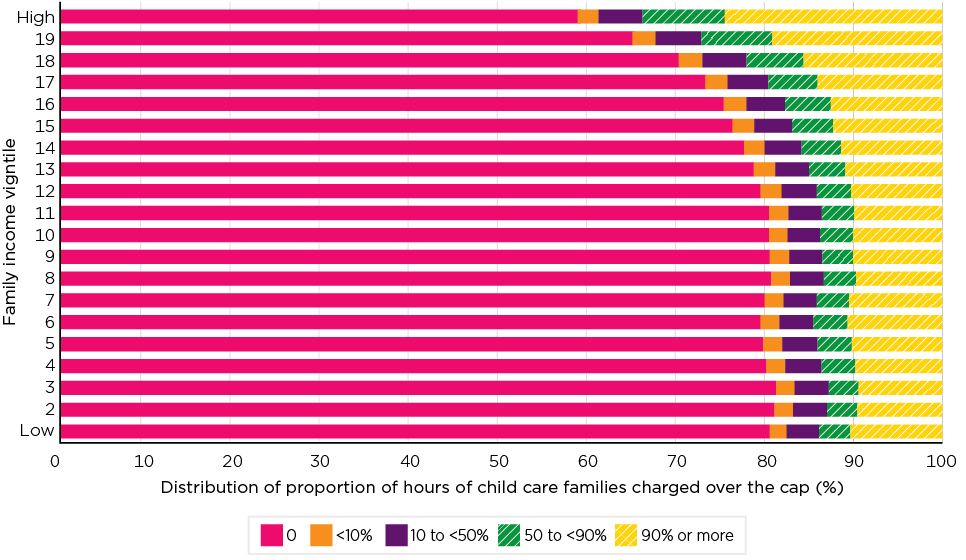

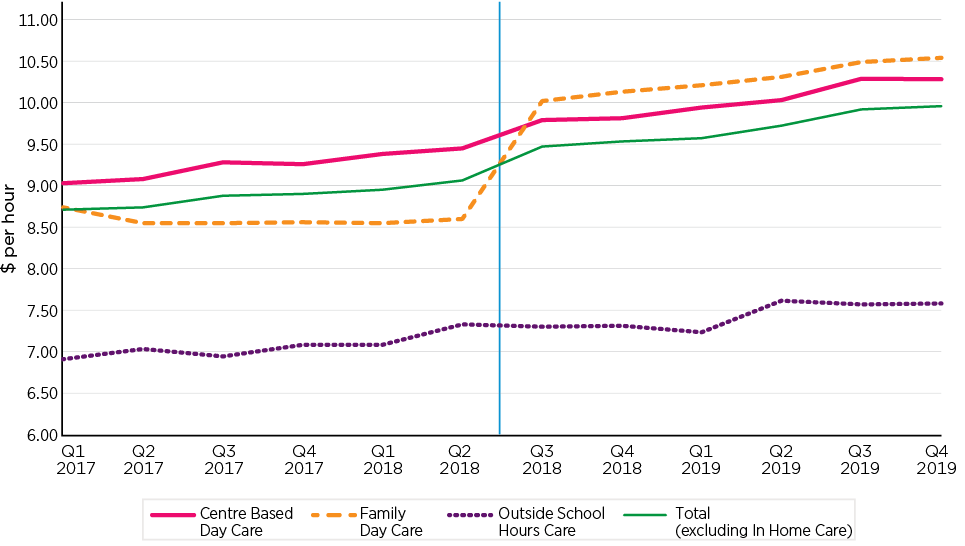

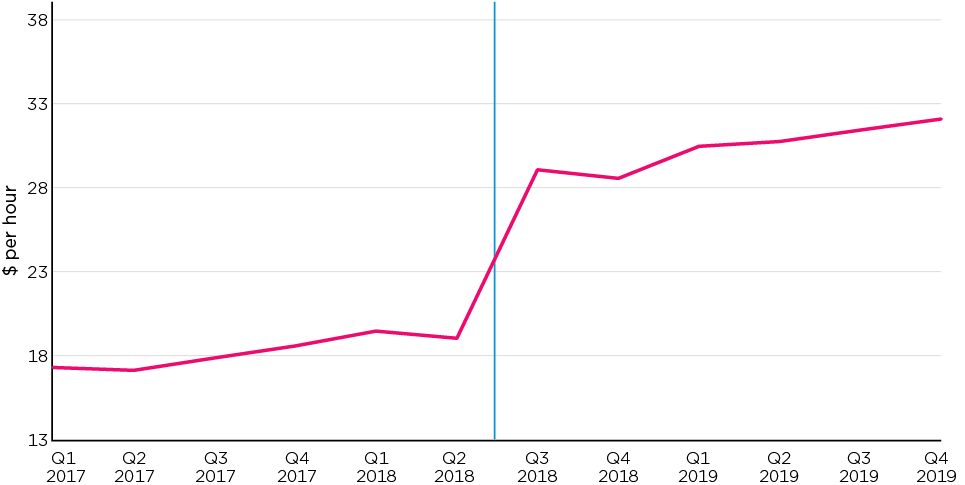

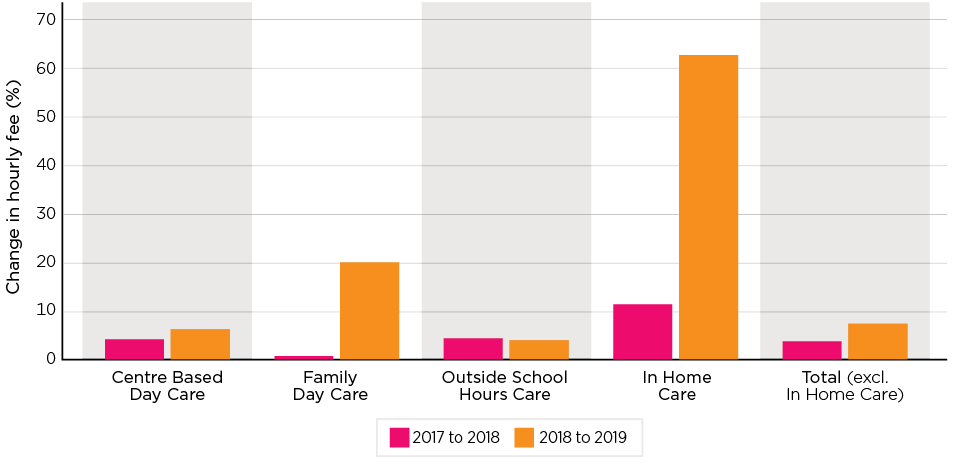

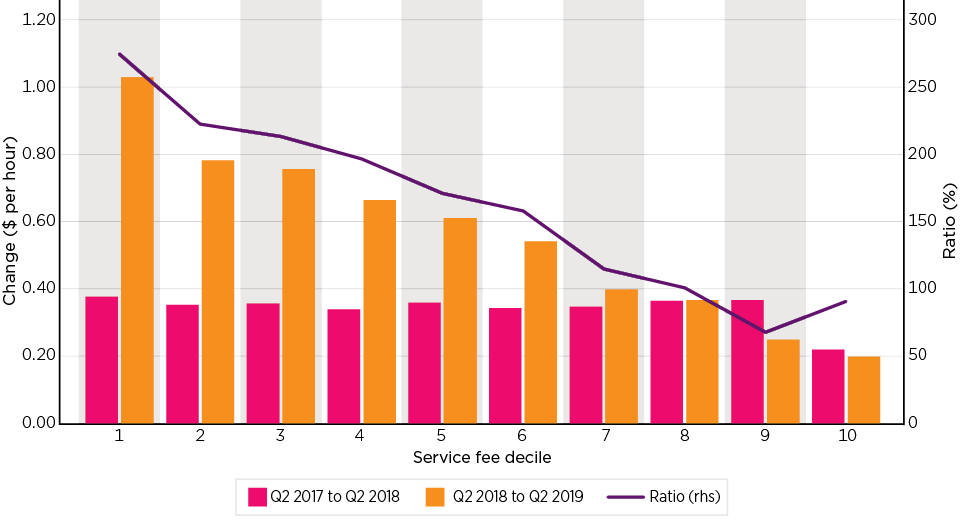

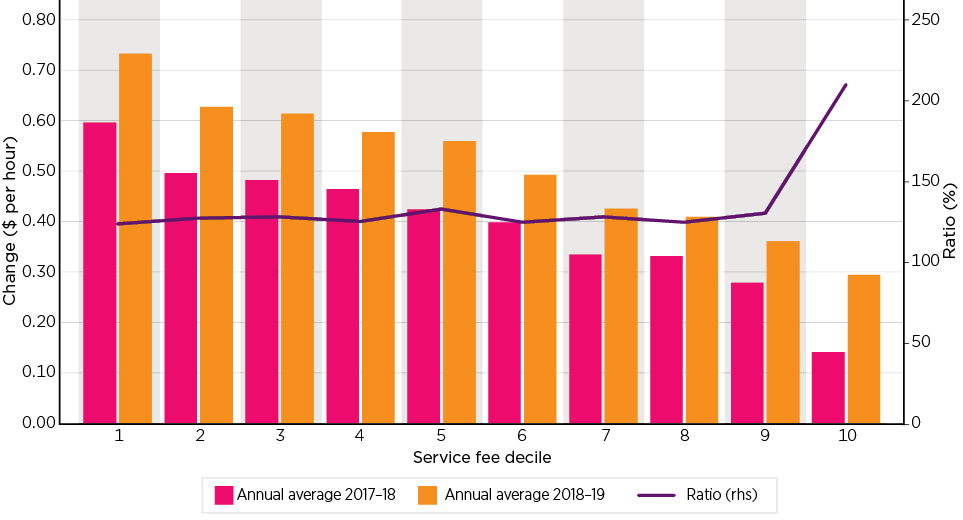

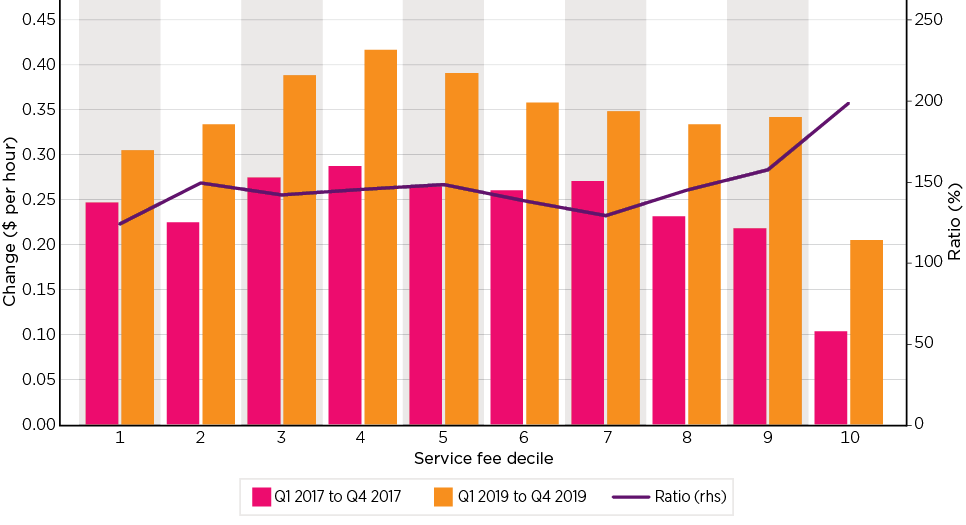

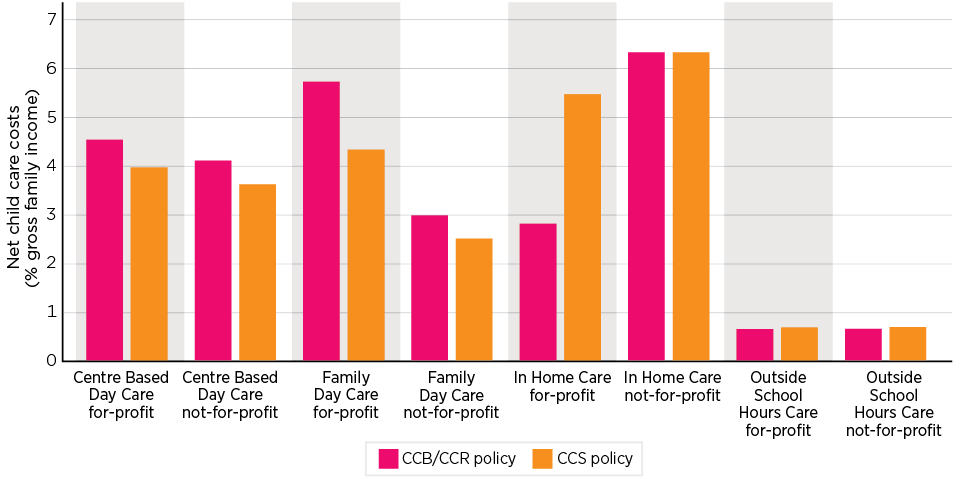

- Fees charged by services have increased at a similar rate following the introduction of the Package to what they were before the changes, with the exception of In Home Care - where associated with the new program structure, the hourly fee is dramatically higher than under the former program- and in Family Day Care, with a continuing shift from sessional to hourly charging. Moreover, the subsidy fees cap is regularly exceeded by services. This suggests that the Package has not been effective, to date, in reducing increases in child care fees.

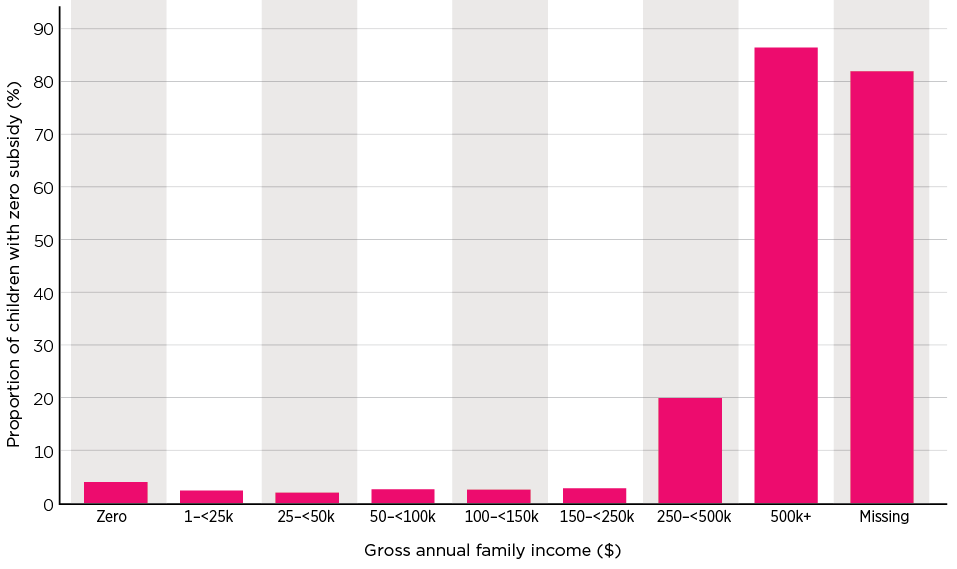

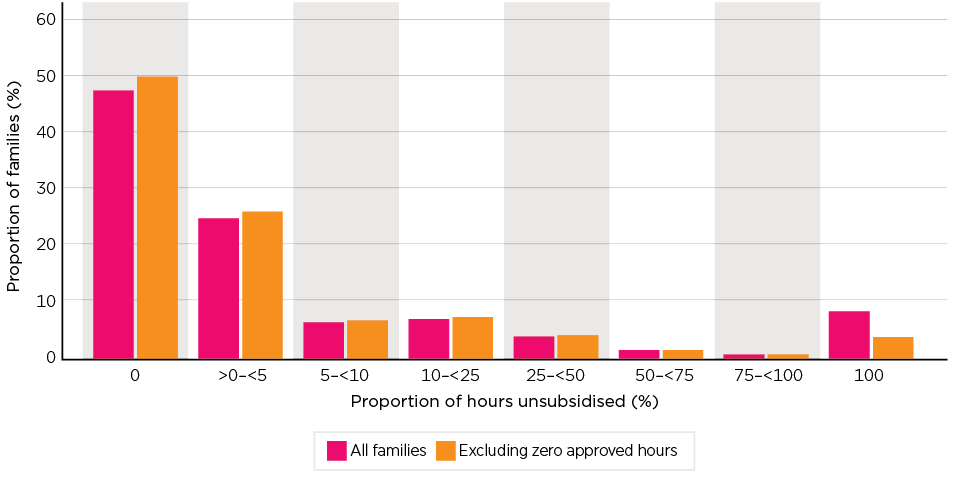

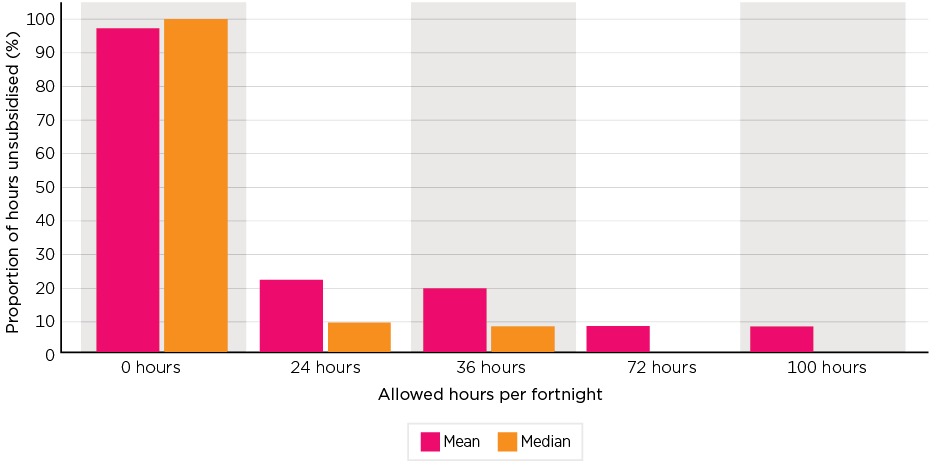

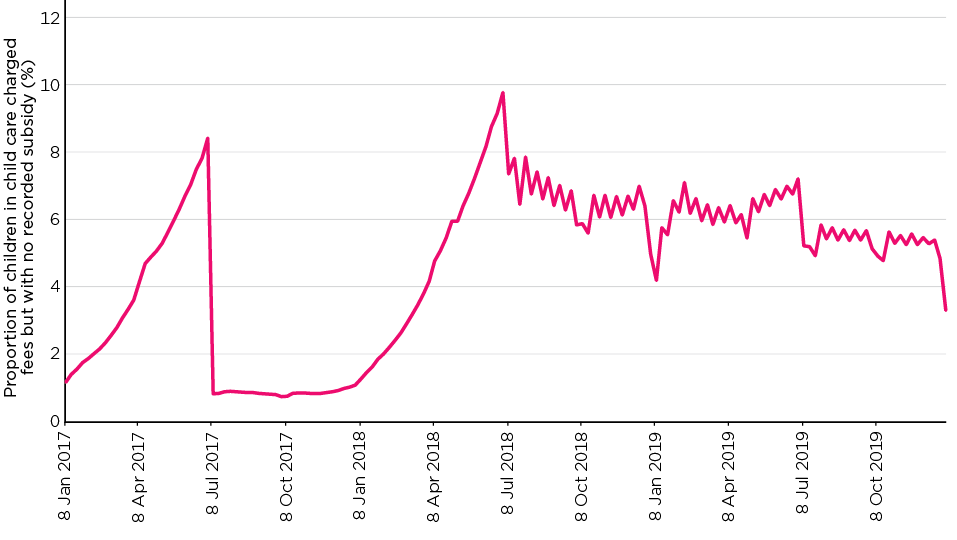

- In 2018-19, 13.3 per cent of hours of child care paid for were unsubsidised and 52.6 per cent of families have some unsubsidised hours. While much of the volume of unsubsidised hours relates to people who have no receipt of CCS, the incidence of unsubsidised hours of care, although varying, persists across all points of the income distribution including those on low income, and across the bands of approved hours.

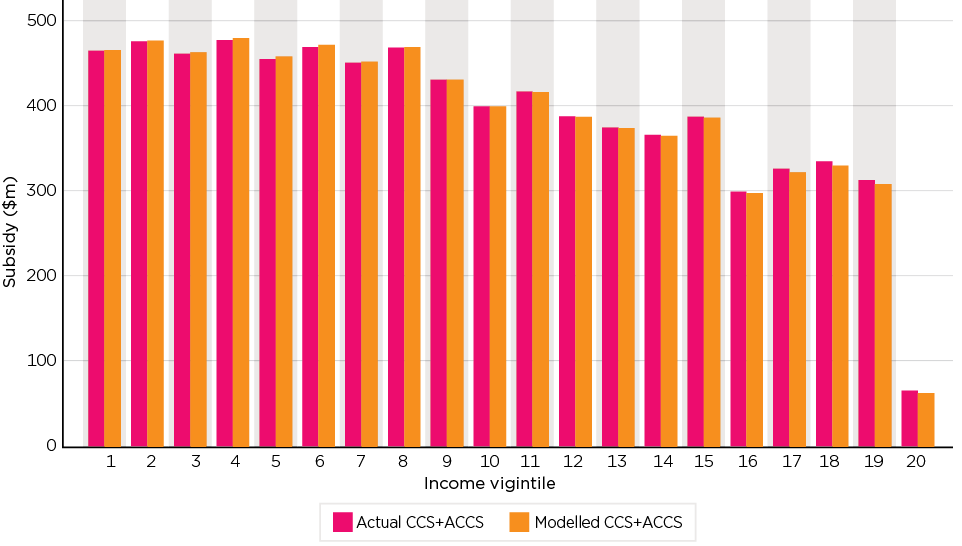

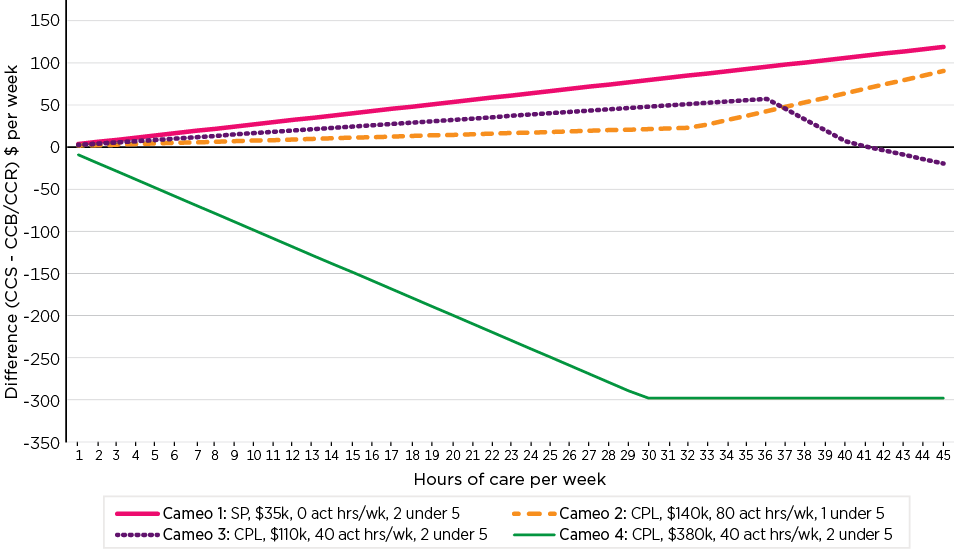

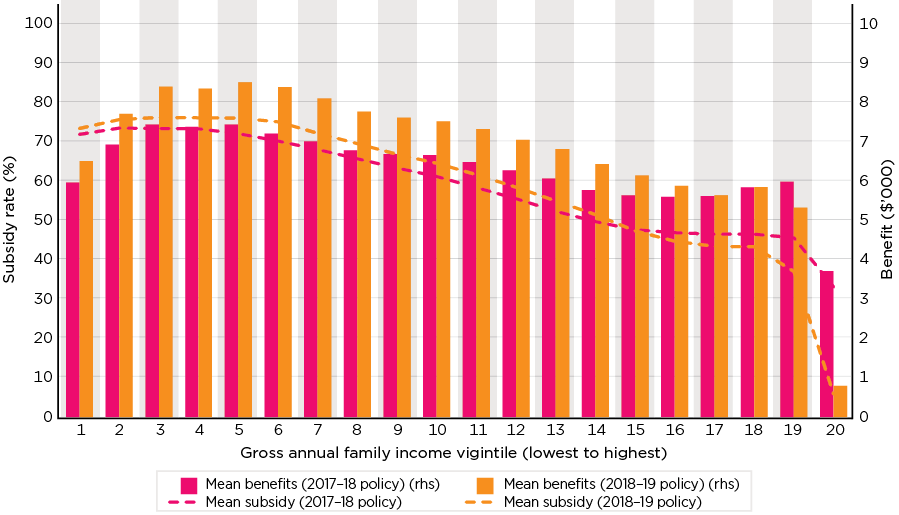

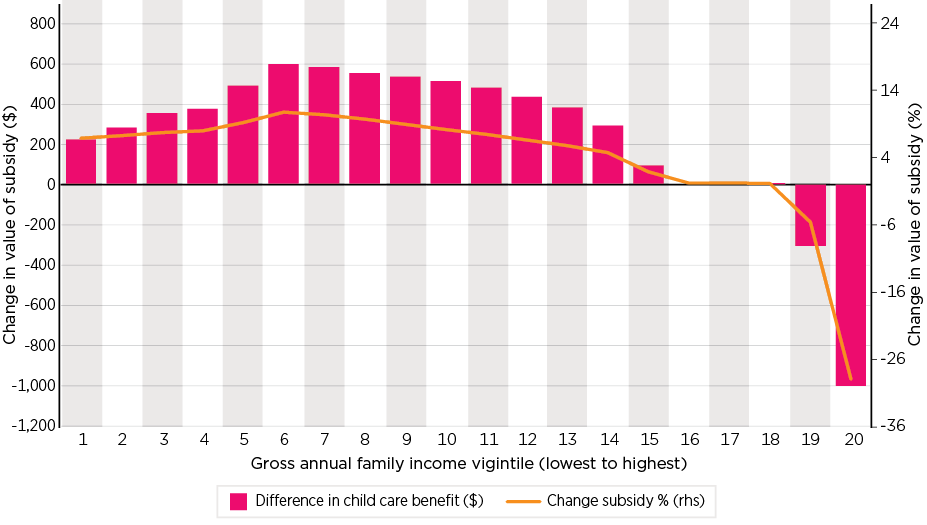

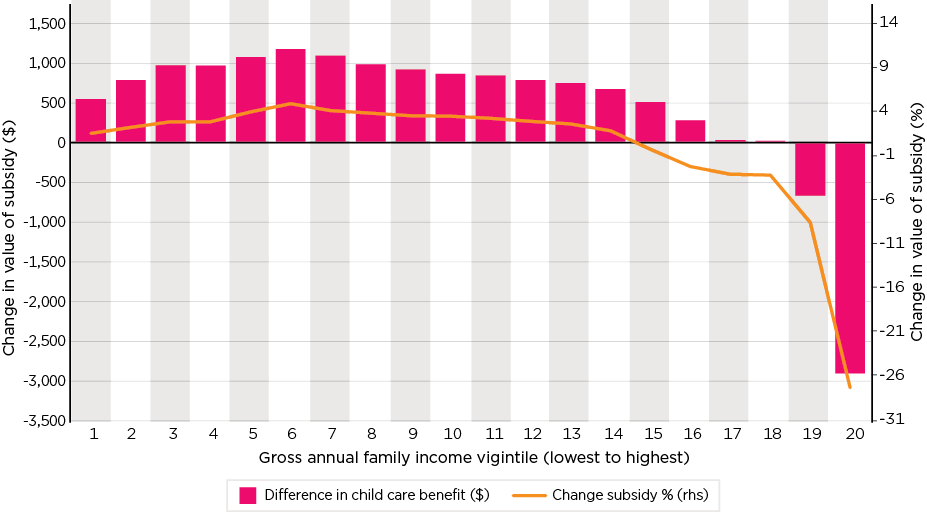

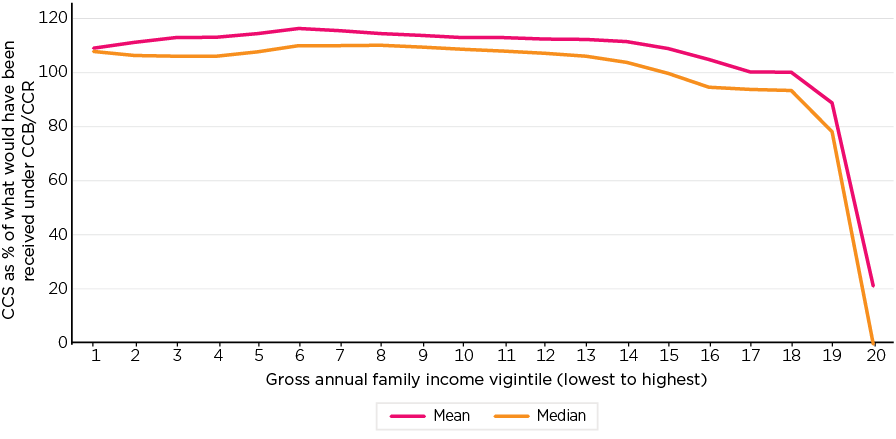

- Extensive modelling was undertaken of the impact of the CCS relative to the CCB/CCR system. This used the 2018-19 population of child care users and estimated, using their actual current fees, income and usage, the value of assistance under the CCS and the old subsidies. This found that the CCS had:

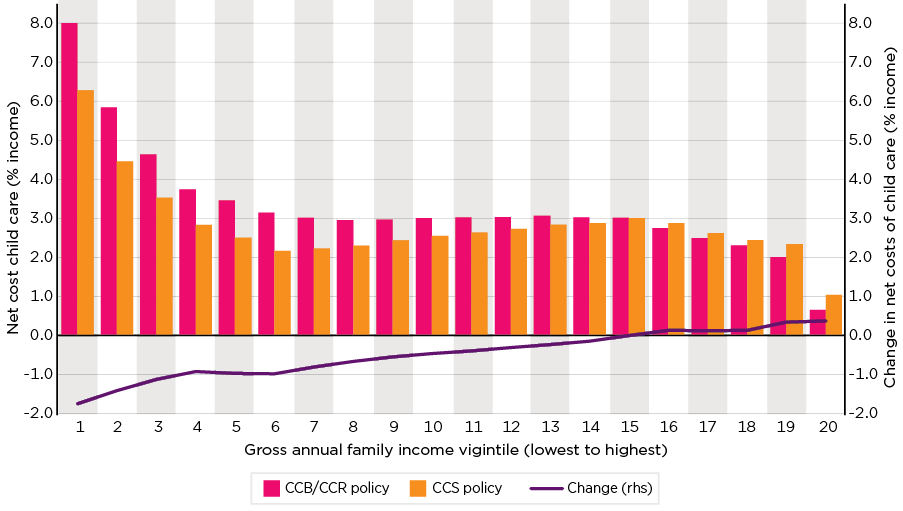

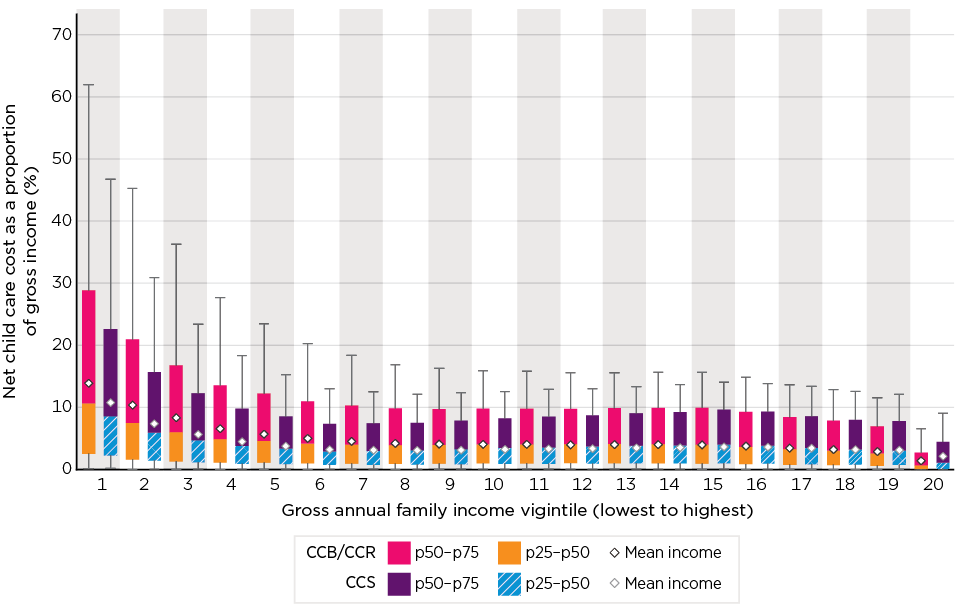

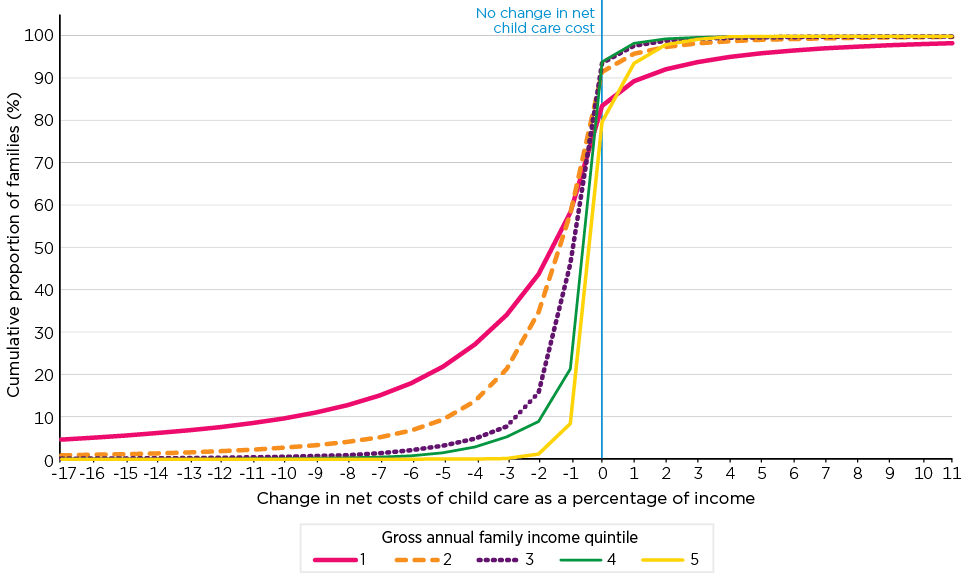

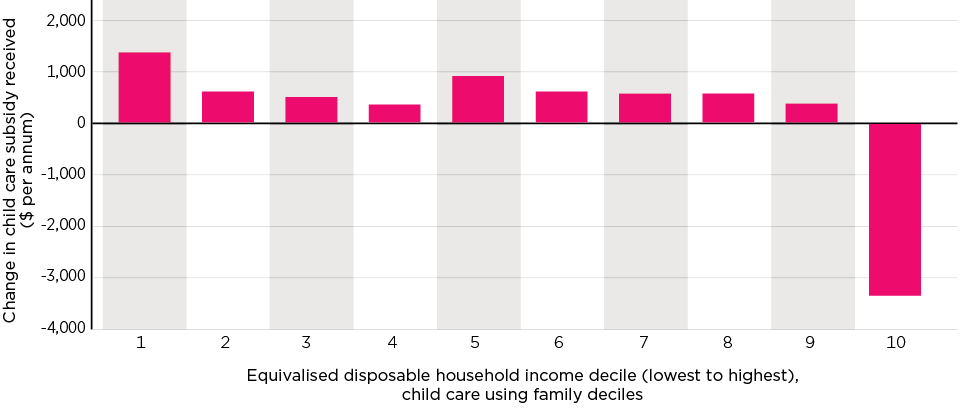

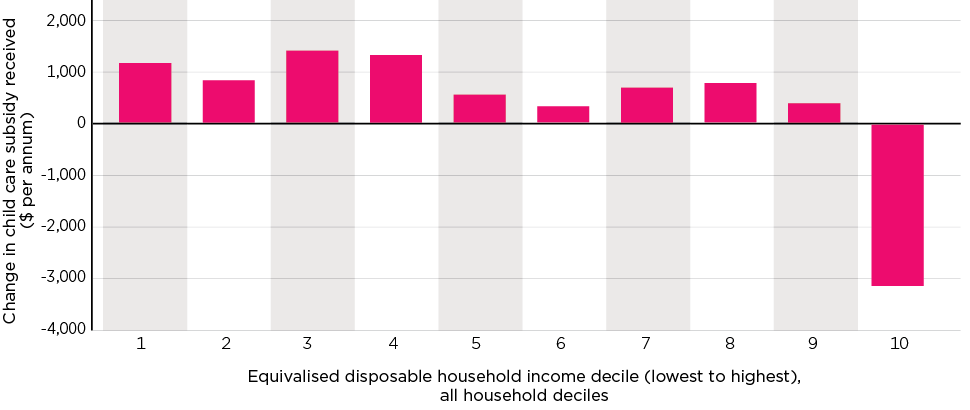

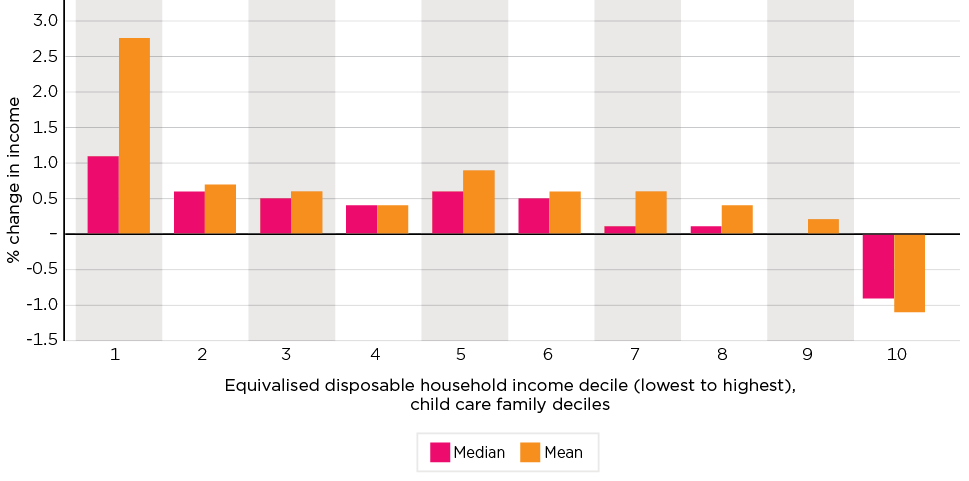

- Reduced the net cost of child care for 62.2 per cent of families using child care, had little impact on the cost for 8.6 per cent and increased the net cost for 29.2 per cent. The annual average income of those that gained was $95,848 compared to $177,240 for those whose cost increased although, overall, there is little difference in net child care costs for the income range $157,335-$240,818 per annum.

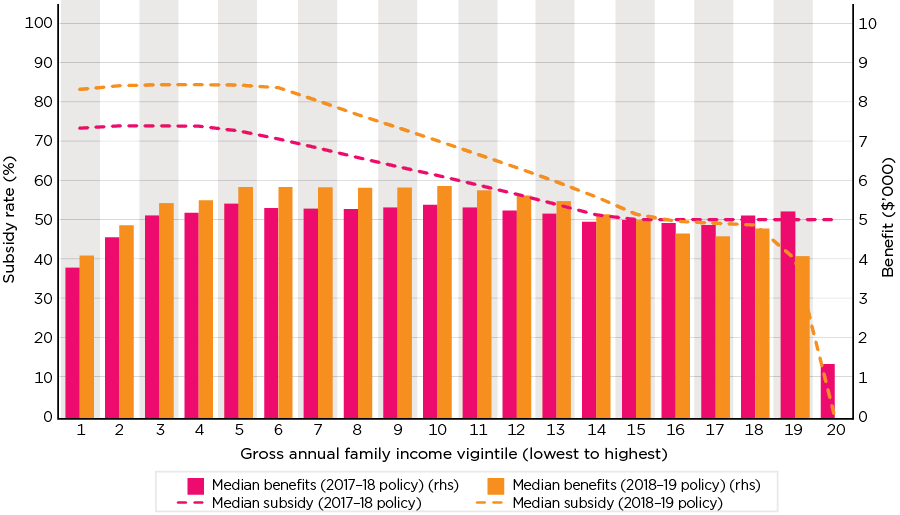

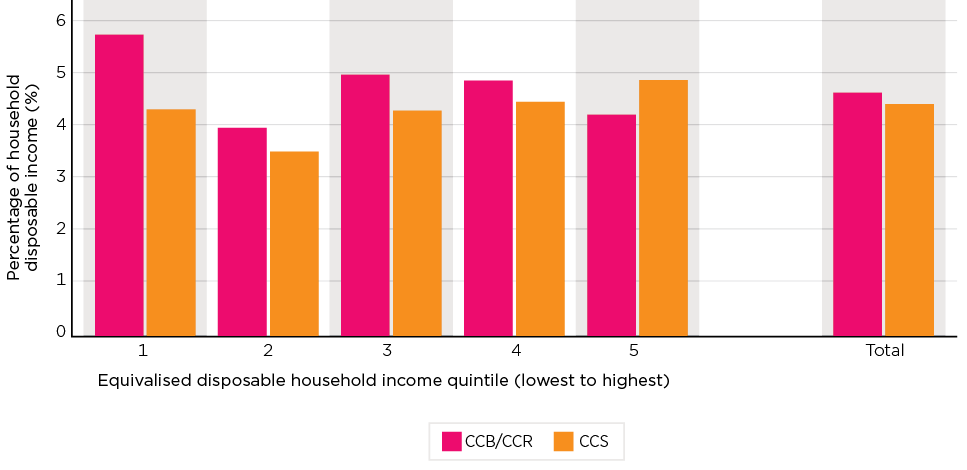

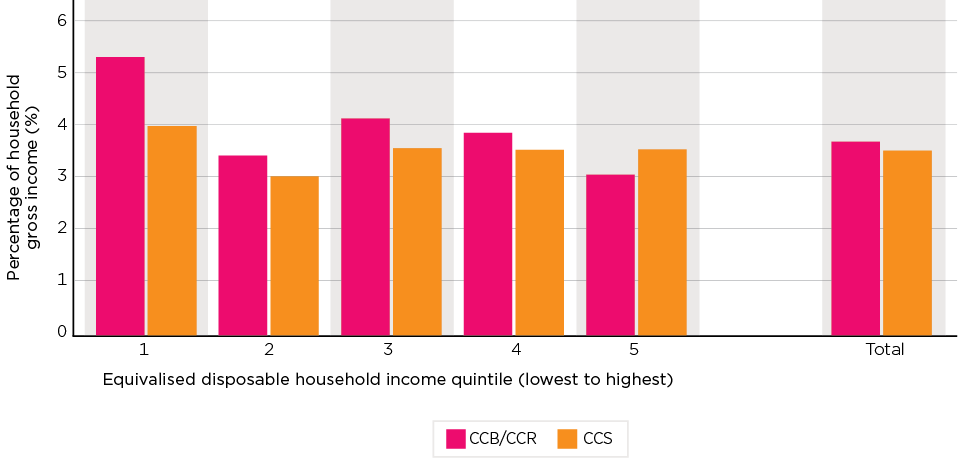

- For those with a reduced cost under the CCS, the average proportion of gross income spent on child care fell from 6.7 per cent to 4.5 per cent, with annual net spending falling from $5,412 to $4,026, and the median cost fell from 4.4 per cent of gross family income to 3.2 per cent, and actual spending from $3,472 to $2,436.

- Across all families the Package has reduced the median annual net cost of child care from $2,957 to $2,507 per annum. As a proportion of gross family income, it has fallen from 3.0 per cent to 2.7 per cent.

- The gains were strongest for low income families, families with larger numbers of children using child care, families using longer periods of care and for those using for-profit Family Day Care. Once controlled for family characteristics there were no strong regional effects.

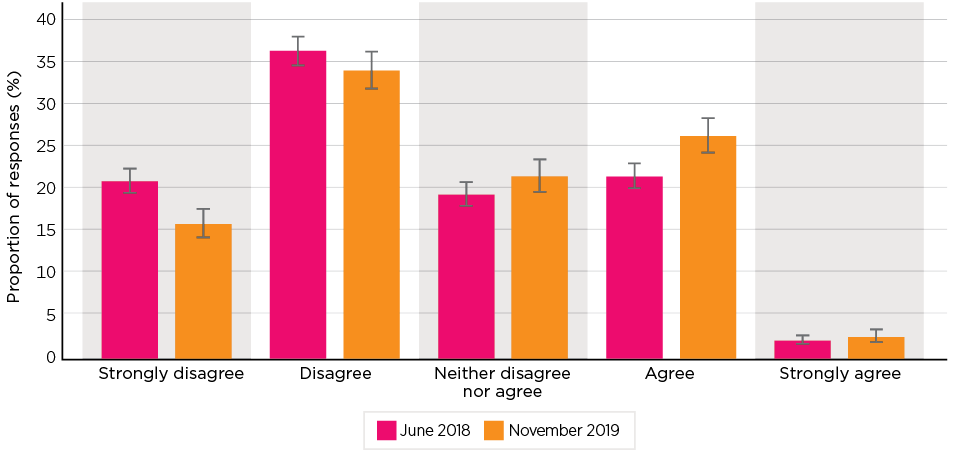

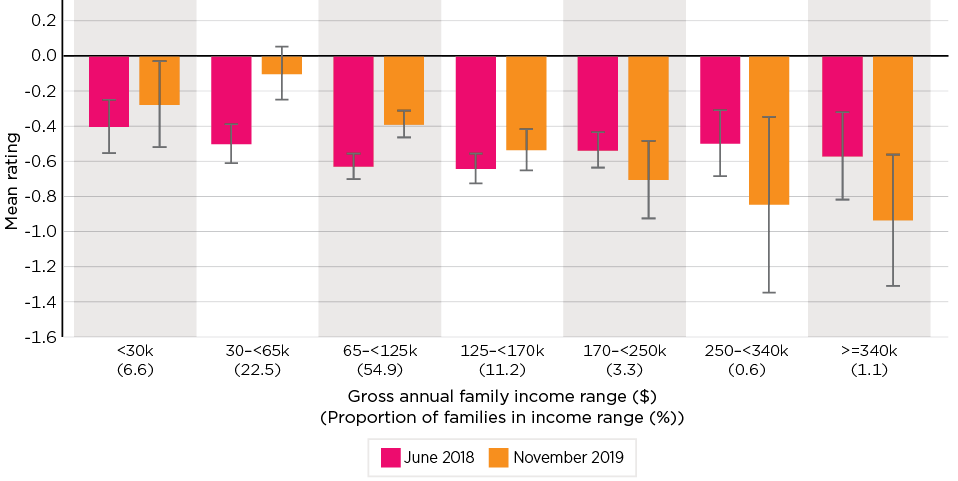

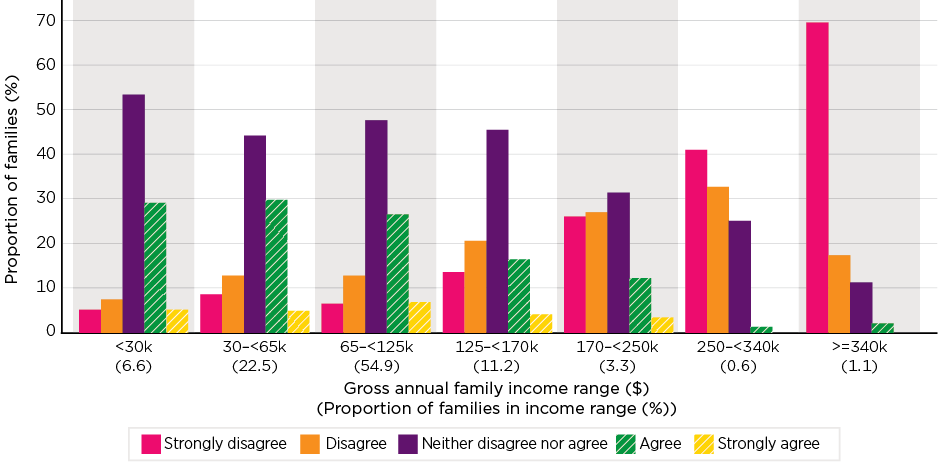

- Parents' survey responses showed a marked and statistically significant increase in parents reporting that child care was affordable following the introduction of the CCS. However, in November 2019, parents with a youngest child aged under 5 were still more likely to disagree (54.7 per cent) than agree (28.4 per cent) that child care was affordable, although those with older children were more equally balanced.

- The Consumer Price Index shows that the changes resulted in an 11.8 per cent decline in the costs of child care in September 2018. Prices have been adjusted at a faster rate than the overall CPI since June 2018. By March 2020 almost three-quarters of the reduction in the child care CPI had been lost.

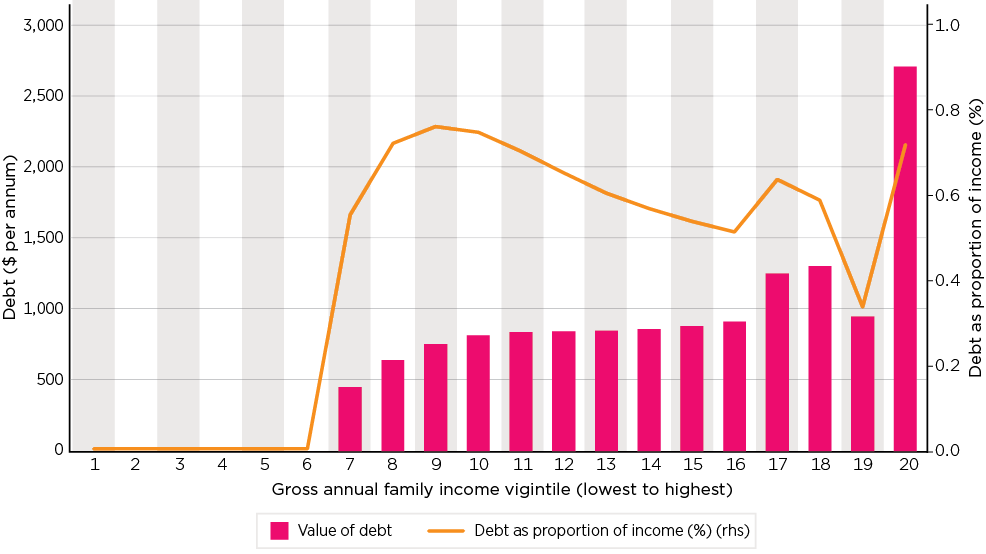

- The annual subsidy cap only impacts a small number of families (about 14,500 in 2018-19) mainly in the income band of $186,958-$251,248, and it is estimated that it only reduced government expenditure on CCS by $24 million in 2018-19.

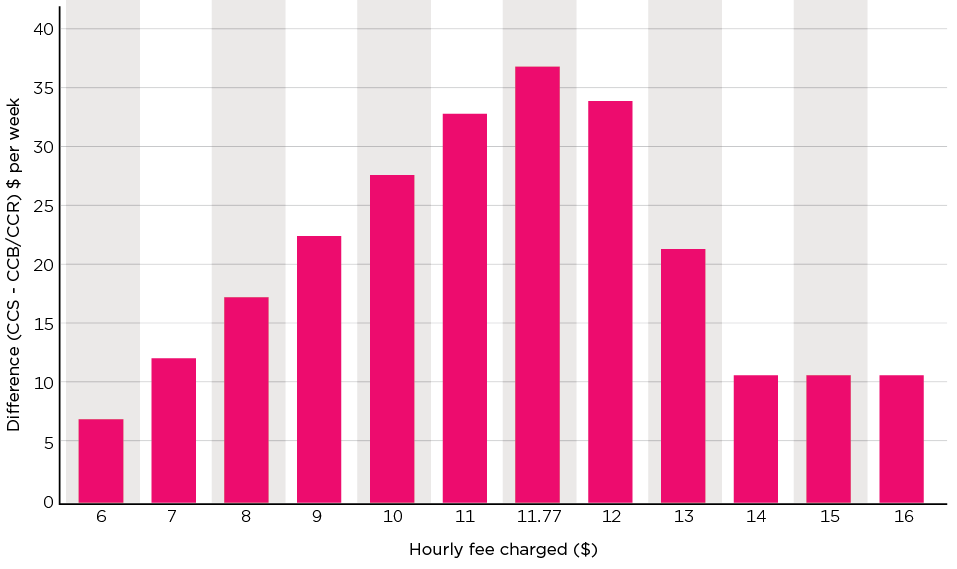

- More broadly, while the higher benefits from the Package have reduced the immediate cost of child care to families, there is little evidence in the data available to the evaluation of the hourly fee cap working as a constraint on fees being charged by services. Additionally, there is a significant group of parents being charged for hours beyond those subject to the CCS.

Outcome 4: Child care services are viable and the sector robust

- It is noted that this evaluation is of the operation of the system to the end of 2019 and thus does not take account of the economic and social disruptions associated with COVID-19.

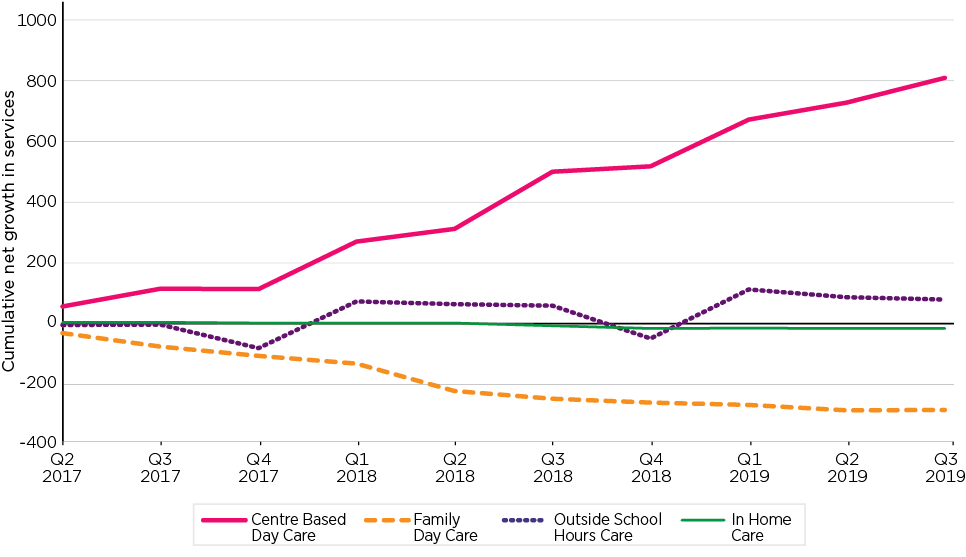

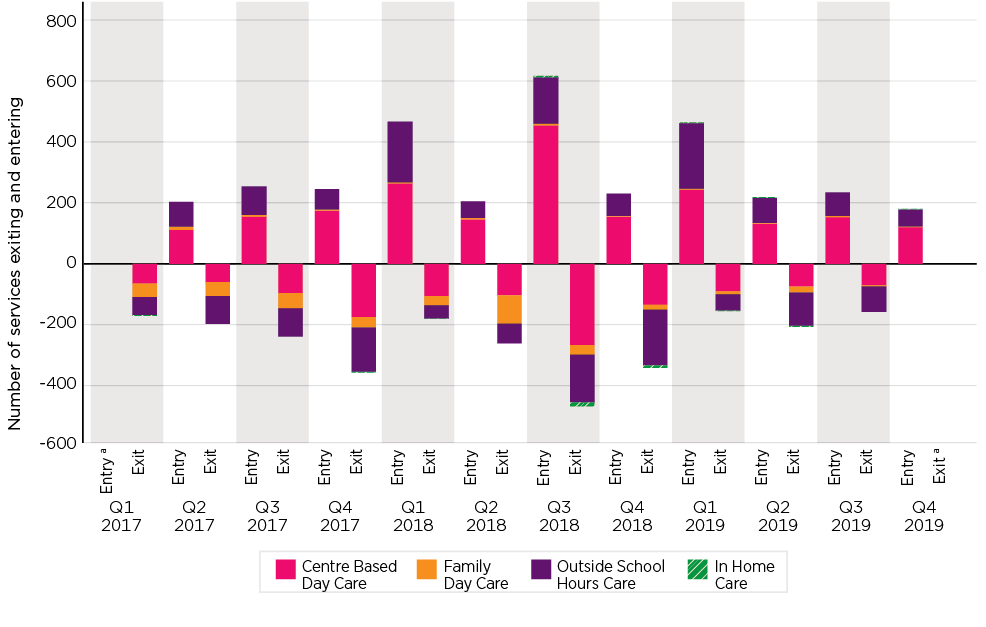

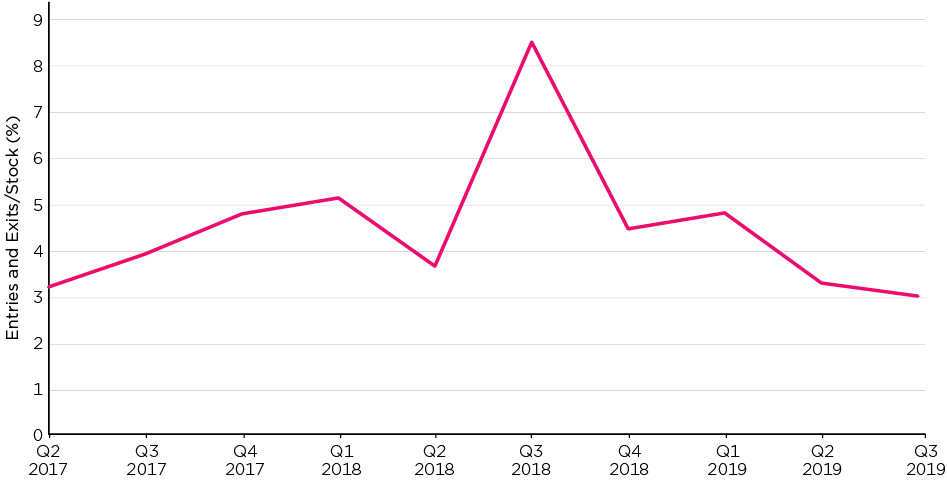

- In 2018-19 child care subsidies accounted for some 60.7 per cent of services' revenue from care provision. The largest parts of the sector, Centre Based Day Care and Outside School Hours Care, are considered to be robust and viable. Other than a spike at the point of introduction, there was no change in the level of new services entering and exiting.

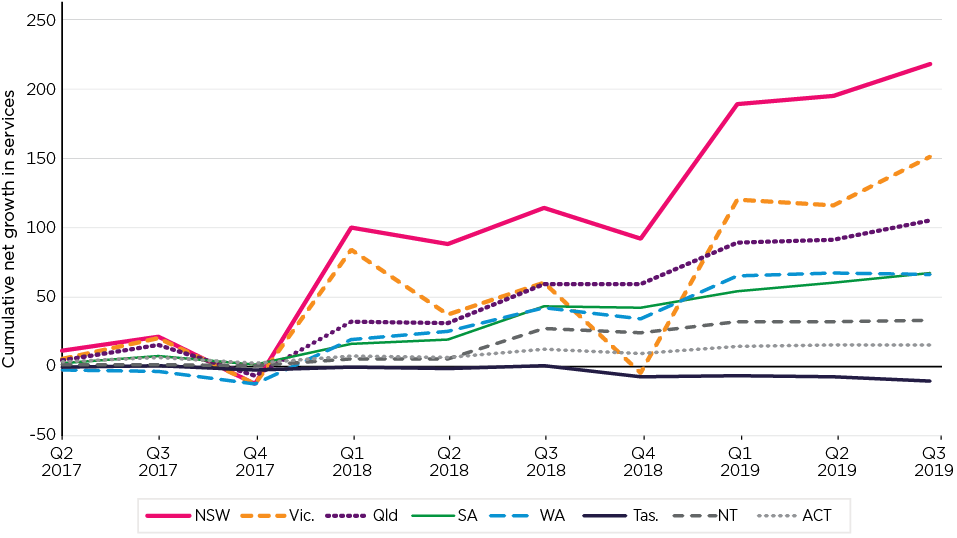

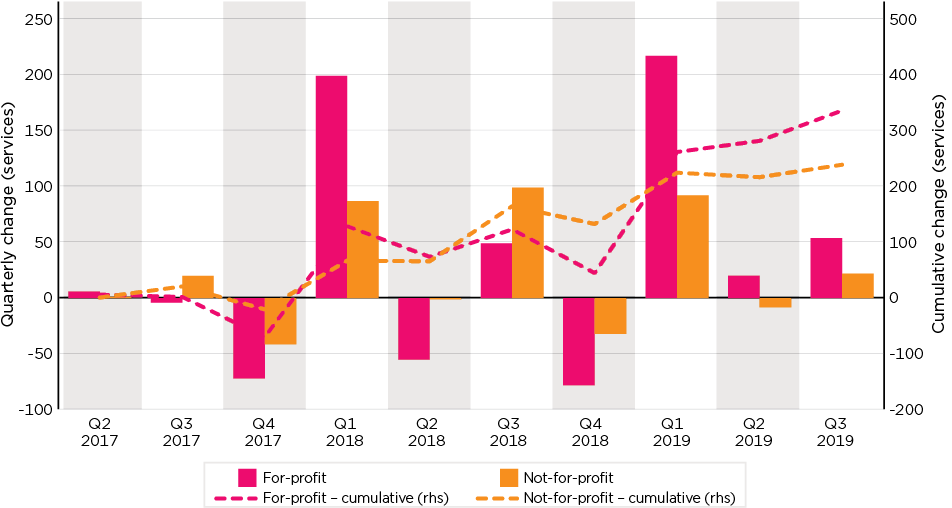

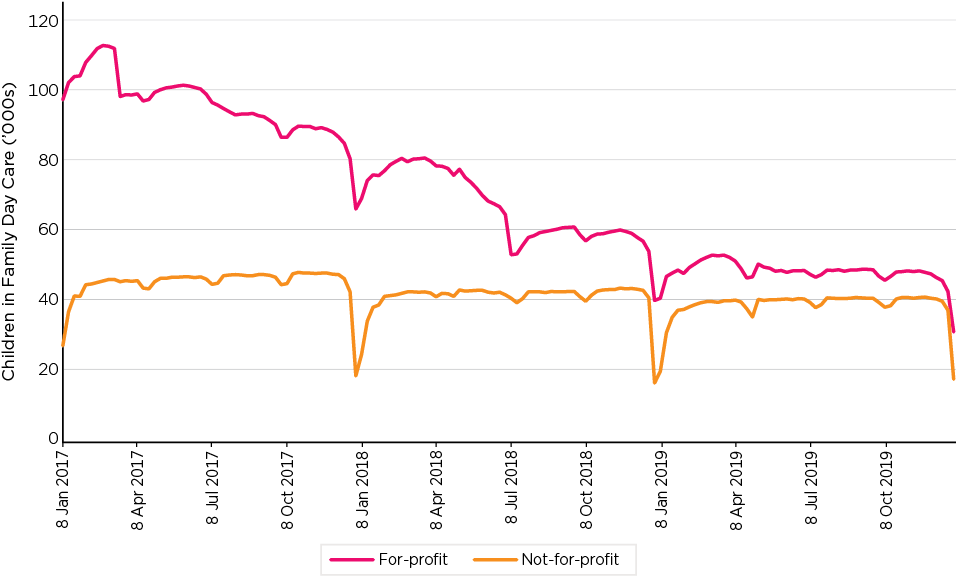

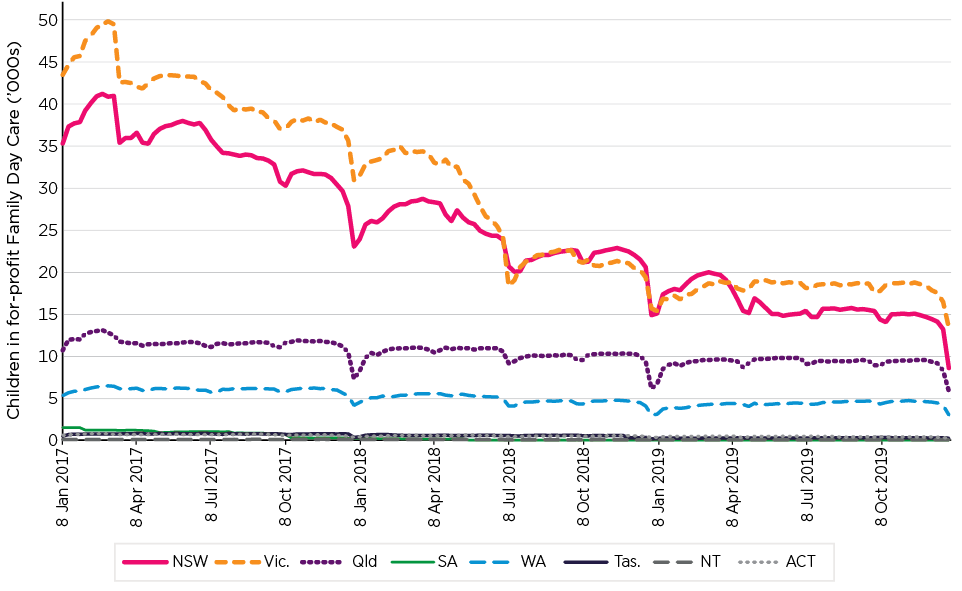

- Since Q2 2017 there has been strong growth in the number of Centre Based Day Care services and a marked decline in Family Day Care, with 79.6 per cent of exits in this sector being associated with government compliance activity.

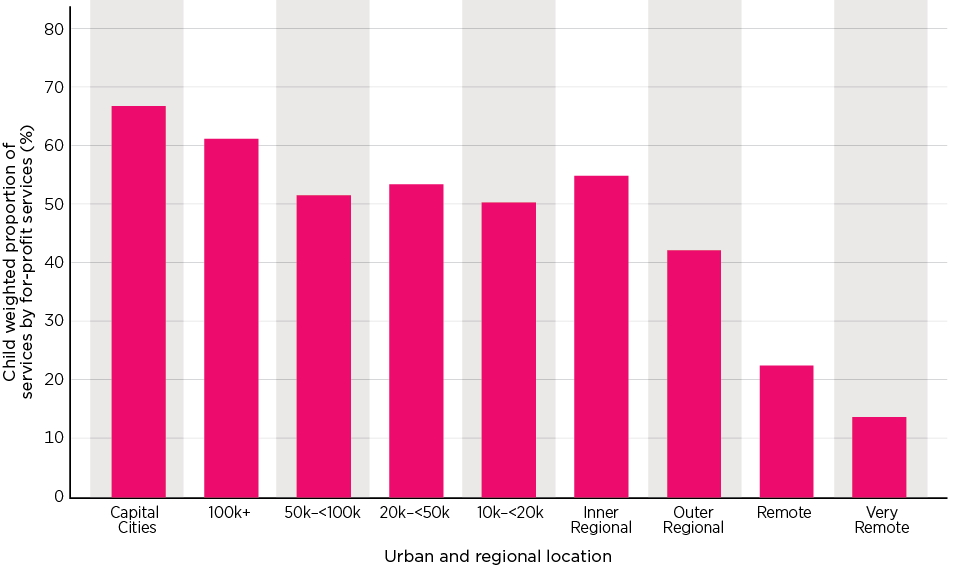

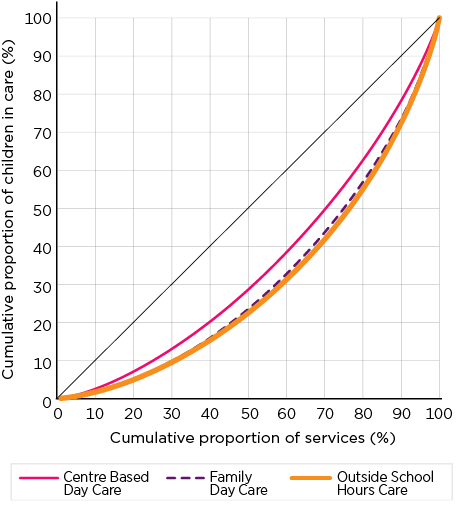

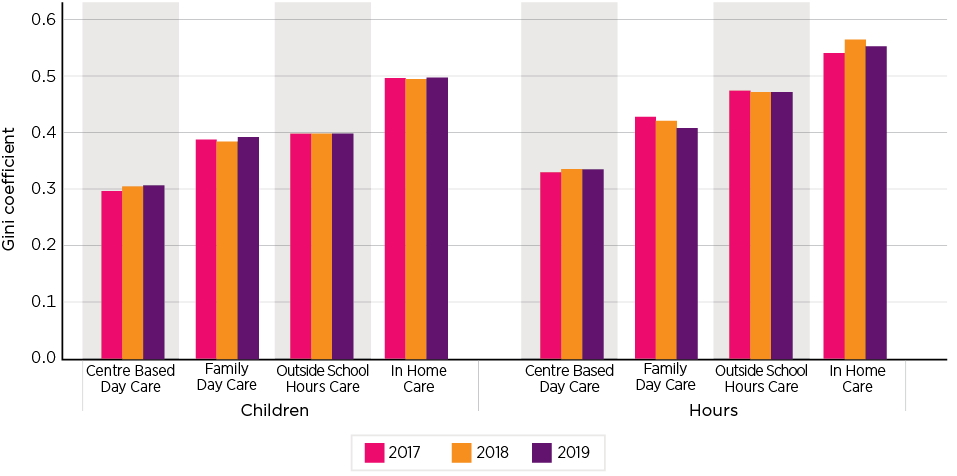

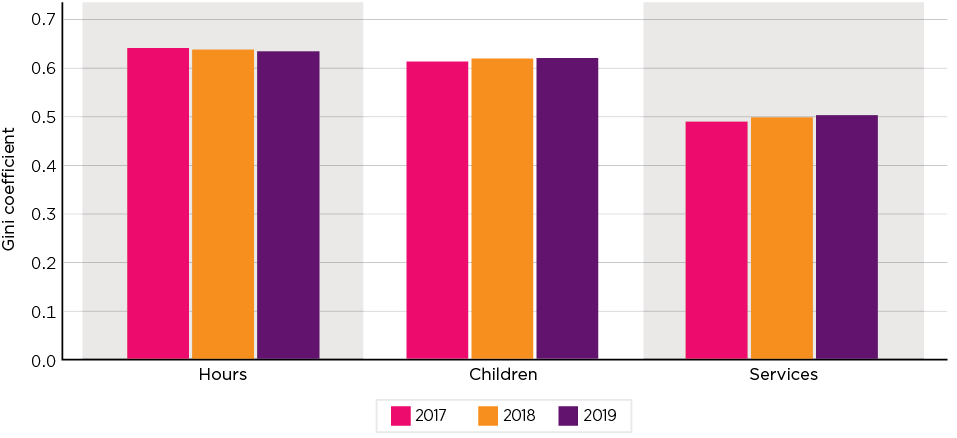

- The roles of these sectors vary considerably across locations, with the not-for-profit sector providing an increasing proportion of services outside the capitals, especially in non-urban locations. There has been a trend towards consolidation across the sector. At the provider level, the Outside School Hours Care sector is the most concentrated and the only sector identified as consistently becoming more concentrated (i.e. the extent to which market share is concentrated among a small number of providers) over the past 3 years.

- Analysis of self-reported service viability indicates that most services viewed themselves as viable, although there was a slight, but statistically significant, drop in this pre and post the introduction of the Package. Relative to Centre Based Day Care, the In Home Care sector was much more negative, and Family Day Care somewhat more negative about their viability, while Outside School Hours Care services were more positive.

In summary, the introduction of the Package appears to have had little impact on the viability of the sector as a whole. The for-profit Family Day Care sector has been the focus of compliance actions and, in larger states, its role has declined dramatically; at the same time, there has been a small but steady reduction in the for-profit sector. In the In Home Care sector, the new program and the increase in subsidy rates are still bedding down and longer-term viability is unclear. A number of services, in particular former BBF services, are effectively underpinned by the CCCF, with the program appearing to be acting, and potentially required, as an ongoing complementary funding stream for services that are unlikely to be viable under the CCS alone.

Impact 1: Parents of children can engage in work, education and the community

- The Package was designed to increase parents' participation in employment. More affordable, flexible and accessible child care was designed to increase the financial returns from employment and to allow parents to increase their workforce participation.

- ABS Labour Force Survey data, surveys of parents conducted for the evaluation and child care system administrative data show small increases in parental activity, including employment, since the Package was introduced. However, these increases are not inconsistent with increases over a period of years.

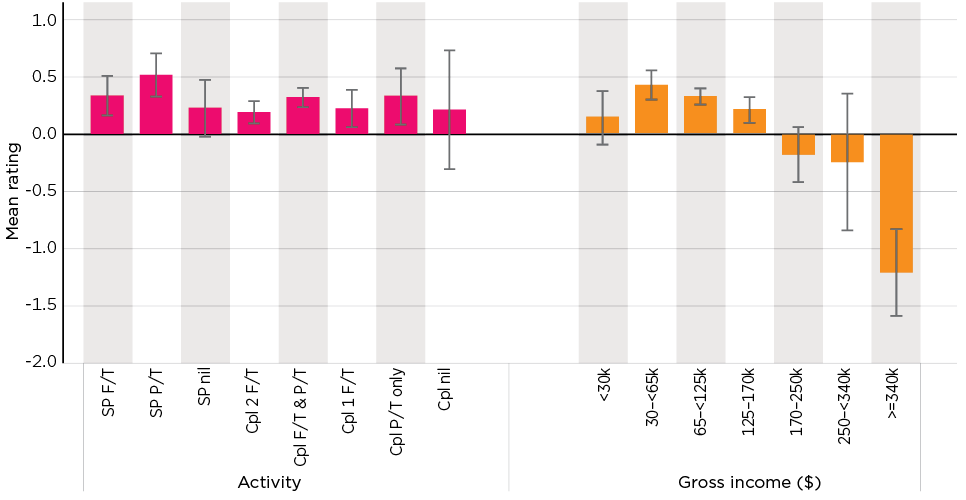

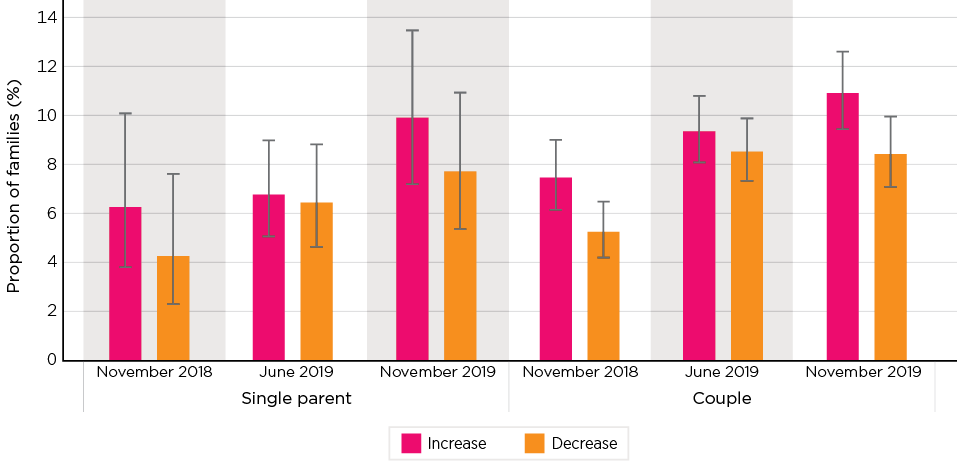

- When asked about changes in employment in response to the Package, some parents reported increasing activity and others reducing, consistent with expected economic behaviour. On average, the proportion reporting an increase was higher than those reporting a fall; by some 1.5 percentage points for single parents and 1.9 percentage points for couples. These results though were not statistically significant. There is no data available on the actual magnitude of this increased activity.

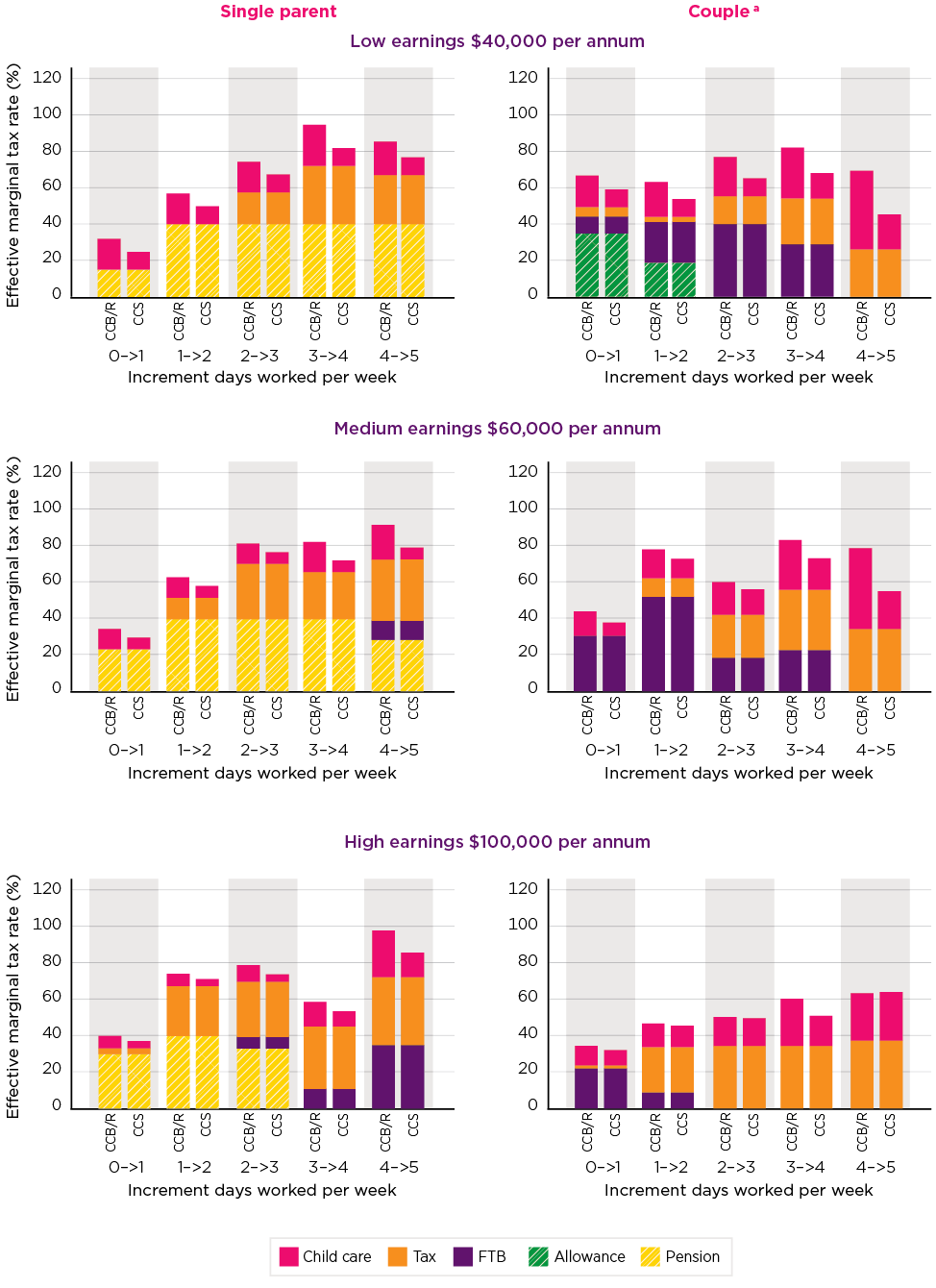

- The introduction of the Package has reduced the Effective Marginal Tax Rates (EMTRs) facing parents increasing their work activity, although they remain very high for some. A range of scenarios were modelled and across these there was an average reduction of 8.5 percentage points in the impact of EMTRs on the earnings parents would gain from working an additional day. After these reductions, the median EMTR was 67.5 per cent, and a quarter of the scenarios had an EMTR of over 78.3 per cent. Generally, single parents had higher EMTRs than a second earner in a couple, and the EMTR tended to be higher when people moved, for example, from 4 to 5 days work, than from zero to one day.

In summary, the evidence suggests that the Package has had diverse impacts on parents' participation in employment. While, on balance, positive, the extent of this is small, and the overall trends are not inconsistent with historical trends in the workforce participation of families with children.

Impact 2: Vulnerable and disadvantaged children are engaged and supported

- The introduction of the Package has had little impact on the overall use of child care among low and lower middle income families. Analysis indicates a small increase (0.2 of a percentage point) in participation for children aged 0-4 years who live in families in receipt of FTB, and a slightly larger but still small fall (0.6 of a percentage point) for those 5-12 years. There is no clear pattern on access for population subgroups, including those at a higher risk of vulnerability. Relative to overall changes, children of parents on a humanitarian visa, some children whose parents were in receipt of full-rate income support and some lower income single parents had a decrease in access, while Aboriginal and Torres Strait Islander children had a more positive shift. However, these changes are mostly small and do not represent a substantive change in access.

- While access levels are close to overall community rates for some groups, such as children with identified health conditions, there are substantially lower participation rates for a number of vulnerable groups. These include Aboriginal and Torres Strait Islander children, low income families, especially those reliant on income support, some groups of children with CALD backgrounds, including children of humanitarian visa holders. A central issue is the extent to which these groups do not just require 'equal access' and are not obtaining this but, rather, for many of these children early childhood education can play a critical role in addressing their disadvantage.

- The reduction in the minimum hours of subsidised care from 24 hours a week to 24 hours per fortnight has disproportionately impacted children in more disadvantaged circumstances.

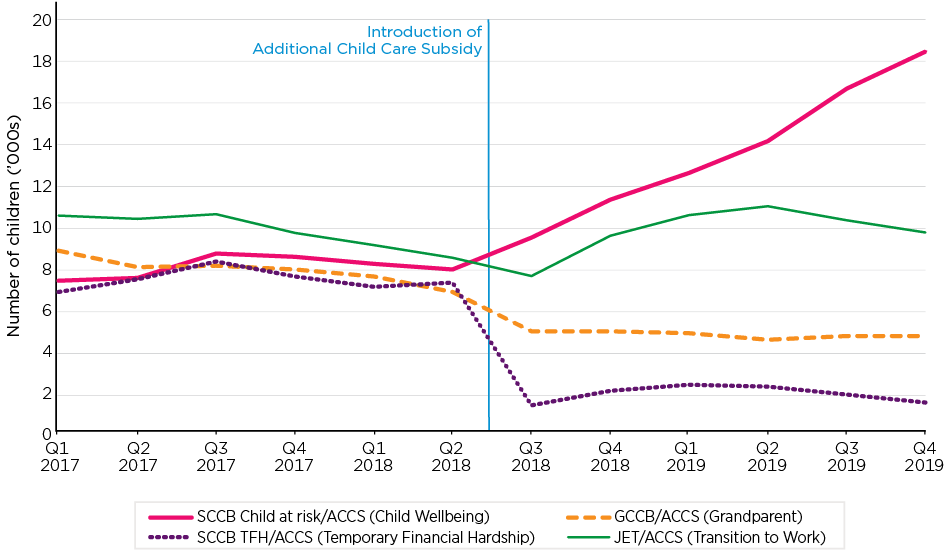

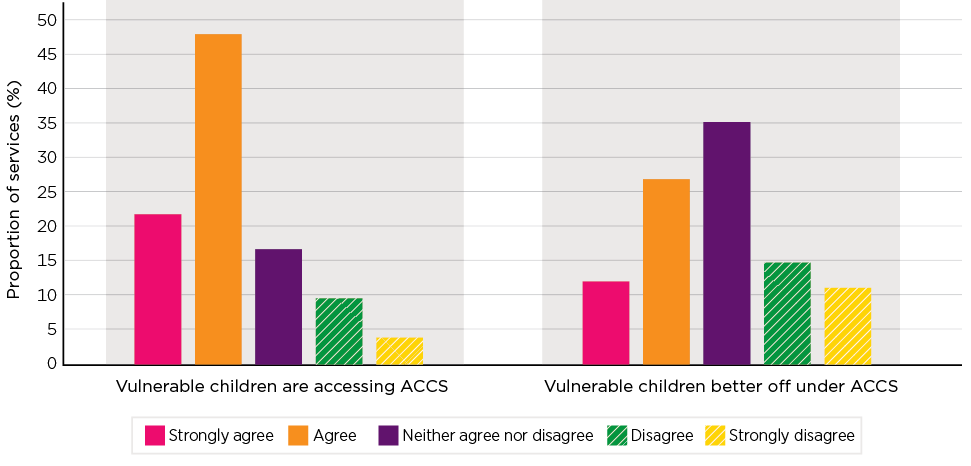

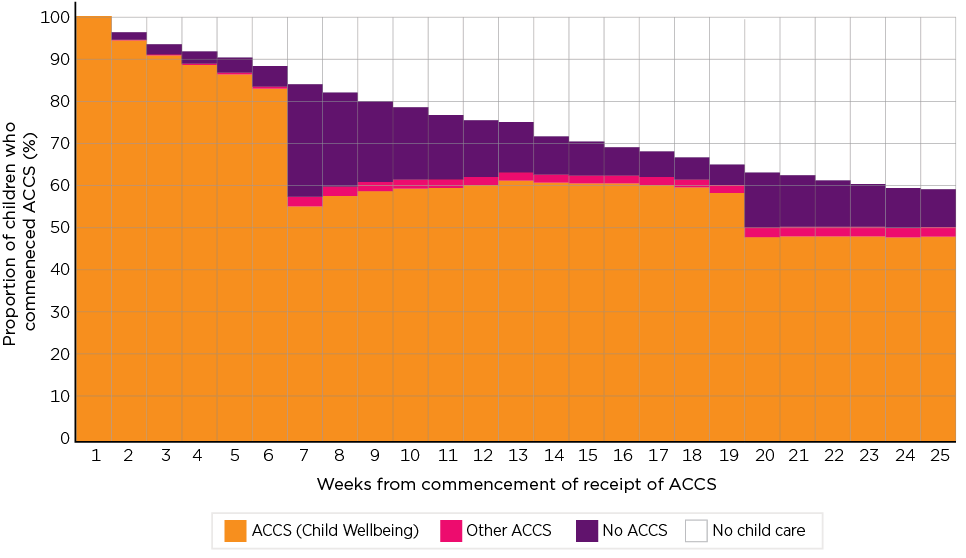

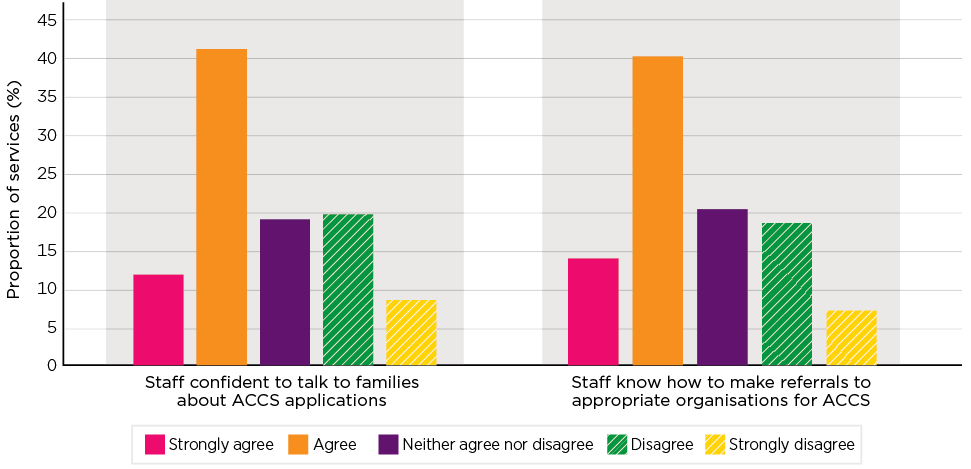

- Overall, the ACCS appears to be effective, but with a significant administrative overhead and with a number of aspects of its operation, including continuity of support, initial access, treatment of kinship and other caring arrangements and the concepts of child wellbeing and 'at risk' having potential for refinement.

Impact 3: Child care funding is sustainable for government

- There is little evidence of any changes to the economic fundamentals of child care provision. While the industry is robust, and there is evidence of continued investment, this appears to be more related to the maturing of the sector and competition for market share. The main driver of cost is wages and it is to be expected that these, consistent with wage growth, will increase at a rate above CPI.

- The evaluation did not identify any significant changes that would impact the ongoing drivers of costs in the provision of child care. Historically, while a series of other subsidy and related interventions have been successful in reducing the real cost of child care to families in the short term, none to date has changed the longer-term trajectory.

The assessment of the sustainability of child care funding is essentially an issue for government in terms of a balance of revenue and expenditure priorities. The evaluation did not address this question. From the evaluation findings there is little evidence of the Package impacting the fundamental drivers of cost in the provision of care. While indexation of the fees cap to the CPI will curtail the extent of cost increases to the government, this is by transferring these to parents.

Recommendations

- The evaluation has made a number of recommendations:

- Specific recommendations are made about improving processes when children commence care, review of approved hours under the activity test and safety net, especially for those with 24 hours a fortnight, the removal of the annual benefit cap, refinement of aspects of the ACCS, and reviewing the helpdesks and the calculator.

- More broadly, the evaluation notes there are significant challenges in the provision of early childhood education and care, including the balance between child care as an enabler of parental workforce participation and the role of early childhood education and care in child development and as an instrument to address disadvantage.

Glossary

| Abbreviation | Description |

|---|---|

| ABS | Australian Bureau of Statistics |

| ACCS | Additional Child Care Subsidy |

| ACECQA | Australian Children's Education and Care Quality Authority |

| AEDC | Australian Early Development Census |

| AIFS | Australian Institute of Family Studies |

| ANAO | Australian National Audit Office |

| ANU | Australian National University |

| ANZSCO | Australian and New Zealand Standard Classification of Occupations |

| ARIA | Accessibility/Remoteness Index of Australia |

| ASCO | Australian Standard Classification of Occupations |

| ATO | Australian Taxation Office |

| BBF | Budget Based Funded Program |

| CALD | Culturally and Linguistically Diverse |

| CAPI | Computer Assisted Personal Interview |

| CATI | Computer Assisted Telephone Interview |

| CBDC | Centre Based Day Care |

| CCB | Child Care Benefit |

| CCB/CCR CCB/R | Former funding model comprised of CCB and CCR |

| CCCF | Community Child Care Fund |

| CCSS | Child Care Subsidy System (formerly the Child Care IT System (CCITS)) |

| CCMS | Child Care Management System |

| CCPFamS | Child Care Package Families Survey |

| CCR | Child Care Rebate |

| CCS | Child Care Subsidy |

| CCTR | Child Care Tax Rebate |

| CPI | Consumer Price Index |

| CRN | Customer Reference Number |

| CSP | Community Support Program |

| Cpl | Couple |

| CWA | Complying Written Arrangement |

| DESE | Department of Education, Skills and Employment. Also refers to predecessors: Department of Education and Training to 29 May 2019, and Department of Education to 1 February 2020 |

| DET | (Former) Department of Education and Training - see DESE |

| DHS | Department of Human Services (On 1 February 2020, DHS became Services Australia) |

| DSS | Department of Social Services |

| ECE | Early Childhood Education |

| ECEC | Early Childhood Education and Care |

| ECEI | Early Childhood Early Intervention |

| EMTR | Effective Marginal Tax Rate |

| FDC | Family Day Care |

| FTB | Family Tax Benefit |

| FTE | Full-time equivalent |

| GCCB | Grandparent Child Care Benefit |

| GST | Goods and Services Tax |

| HILDA | Household, Income and Labour Dynamics in Australia Survey |

| IAS | Indigenous Advancement Strategy |

| IHC | In Home Care |

| IRSAD | Index of Relative Socio-Economic Advantage and Disadvantage |

| ISP | Inclusion Support Program |

| IS | Income Support |

| IT | Information Technology |

| ITRG | Implementation and Transition Reference Group |

| JETCCFA | Jobs, Education and Training, Child Care Fee Assistance |

| LDC | Long Day Care |

| LinA | Life in Australia survey |

| LOTE | Language Other Than English |

| NDIS | National Disability Insurance Scheme |

| NFF-OCC | Non-Formula Funded Occasional Child Care |

| NHMRC | National Health and Medical Research Council |

| NQA ITS | National Quality Agenda Information Technology System |

| NQF | National Quality Framework |

| NQS | National Quality Standard |

| OECD | Organisation for Economic Co-operation and Development |

| OLS | Ordinary Least Squares |

| ORIMA | ORIMA Research Pty Ltd |

| OSHC | Outside School Hours Care |

| PAES | Portfolio Additional Estimates Statements |

| PEP | Provider Entry Point |

| PIR | Post Implementation Review |

| PolicyMod | ANU Centre for Social Research and Methods microsimulation model |

| PRODA | Provider Digital Access |

| rhs | right hand scale |

| SCCB | Special Child Care Benefit |

| SEIFA | Socio-Economic Indexes for Area |

| SELCS | Survey of Early Learning and Care Services |

| SES | Socio-Economic Status |

| SNAICC | SNAICC (Secretariat of National Aboriginal and Islander Child Care) - National Voice for Children |

| SIH | Survey of Income and Housing |

| SP | Single Parent |

| SPRC | Social Policy Research Centre |

| SRC | Social Research Centre |

| UNSW | University of New South Wales |

1. Introduction: The Child Care Package

This is the final evaluation report on the Child Care Package that was introduced by the Australian Government, in large part, in July 2018.

Due to the impact of COVID-19, some aspects of the evaluation of this program were curtailed, and the timing of the final report brought forward from mid 2021 to early 2021. Specifically:

- The evaluation focuses on the implementation and outcomes of the program to end December 2019, as after this date parents using child care and services were significantly affected by the pandemic and policy responses to it. In the case of child care, this included the introduction of an Early Childhood Education and Care Relief Package which operated from 6 April to 12 July 2020 and which included the suspension of Child Care Subsidy payments, a Transition Payment over the period 13 July to 27 September 2020 involving a reintroduction of the payments, and a Recovery Package commencing on 28 September 2020 and which was anticipated to continue to 31 January 2021.

- A number of data collection activities envisaged as providing central inputs into the final evaluation were not able to be conducted. This included not being able to undertake the third wave of the services survey.

1.1 The Child Care Package

In July 2018 the Australian Government introduced the 'new Child Care Package' through the Family Assistance Legislation Amendment (Jobs for Families Child Care Package) Act 2017. The new Child Care Package has 4 key elements:

- Child Care Subsidy (CCS) - the main form of Australian Government financial support to parents as a subsidy for child care costs

- Additional Child Care Subsidy (ACCS) - additional fee assistance directed at families and children who may face barriers in accessing affordable child care

- Inclusion Support Program (ISP) - support for services to build their capacity and capability to include children with additional needs in mainstream services

- Community Child Care Fund (CCCF) -enables grants to child care services to help them address barriers to participation and to support service sustainability, and funding for services in areas of high unmet demand.

The Additional Child Care Subsidy, Inclusion Support Program and Community Child Care Fund are collectively referred to as the Child Care Safety Net that provides additional targeted assistance for disadvantaged communities and vulnerable children and their families to address barriers to participation in child care and employment. The structure of the program is illustrated in Figure 1.

Figure 1: Structure of the Child Care Package

1.1.1 Program objectives

The Package's core objectives include addressing issues of affordability and increasing costs, improving flexibility and increasing the targeting of financial assistance, in particular, to support those parents who are working or looking for work.

This was articulated in the second reading speech by the Minister for Social Services as:

Almost one million Australian families will benefit as a result of this child care assistance package. Low- and middle-income families will be the greatest beneficiaries …

Together, these reforms will ensure that, in a fiscally sustainable way, we can achieve three important goals:

- continue to assist families in raising their children and provide access to quality early learning opportunities over the long term

- enable and encourage greater workforce participation; and

- simplify our child care payments and social security systems …

Our objective is to help parents who want to work, or who want to work more, while still focusing on early childhood education.

Having two parents in paid employment has become the preferred choice for most families because of the changes in our society and economy over many years. More affordable access to quality child care puts the opportunity of work within far better reach of more families.

The Jobs for Families Child Care Package is designed to support more families, including jobless families, to increase their participation in work, training, study or volunteering. The government's significant investment is targeted to those who need it most - low and middle income families who are juggling work and parenting responsibilities. (Porter, 2016)

The policy was seen as a major initiative. Minister Porter referred to it as a 'once in a generation reform to child care' (Porter, 2017a), a sentiment reflected in the Departmental media release on the passing of the legislation:

This legislation gives effect to the most significant reform to the early education and care system in decades and will better target those who want work or work more. It will give around one million Australian families relief from out-of-pocket child care cost pressures and provide more children with the opportunity to benefit from early education.

Over the next 15 months, the Australian Government will implement a new child care system which is more affordable, accessible and flexible. (Department of Education, Skills and Employment (DESE), 2017)

1.1.2 Implementation

The Australian Government Department of Education, Skills and Employment (DESE)1 is responsible for the implementation of the Package, with the operationalisation of the CCS through the Centrelink element of Services Australia, an agency within the Social Services portfolio.

The Child Care Subsidy commenced operation on 2 July 2018. Its introduction was complemented by a new Information Technology system which was developed with the objective of providing a simpler interface for both parents and services, and to automate the payment system. This includes, as of January 2019, a requirement for services to report actual 'in' and 'out' times of children as part of sessional reporting.

Changes were also made to the child care services regulatory framework. These included a strengthened set of requirements that services need to comply with, including reporting on children's actual hours of attendance, as well as the removal of some requirements related to hours of operation.

Some elements of the Package were implemented prior to the introduction of the Child Care Subsidy, with the Child Care Safety Net being progressively rolled out from July 2016. At this time, the Inclusion Support Program was introduced, as was the Connected Beginnings program, which is part of the Community Child Care Fund. Another early element of the Child Care Package was the Nanny Pilot Programme, initially called the Interim Home Based Carer Subsidy Programme. A new In Home Care (IHC) program was introduced in July 2018, which replaced the previous In Home Care program and the previous Nanny Pilot Programme.

Since its initial implementation, a number of changes and other measures have been introduced. In addition to those associated with COVID-19, as detailed in the introduction, these include:

- A set of mainly technical reforms in a series of legislative instruments. Of note these included: an extension of the 'eight week' rule (see Chapter 3); increases in the In Home Care hourly rate (see Chapter 4); and the removal of the 50 per cent ACCS (Child Wellbeing) rule (see Chapter 7).

- Changes to the Inclusion Support Program, including revised guidelines issued in March 2020 and changes in the IT environment for this program.

- Additional emergency measures, mainly through the Community Child Care Fund (CCCF) program to support services adversely affected by drought and bushfires, but also including support for families in bushfire declared areas by exempting them from the CCS activity test for the financial year.

In addition to these, enhanced compliance activities in the child care sector, initially introduced in 2014, and mainly directed at addressing fraud and related misconduct, have been maintained. The impacts of these - in particular, with regard to Family Day Care services - are discussed in Chapter 9.

1.1.3 The Child Care Subsidy

The Child Care Subsidy (CCS) is the main element of the Package and provides targeted assistance with the cost of child care. The parameters of the system include:

- a cap on the hourly rate charged for child care to which the subsidy rate will apply

- a subsidy rate that declines as family income increases

- an annual cap on the total level of assistance paid to some higher income households

- a limit on the number of hours of care for which the subsidy is payable for each child based on an activity test applied to the parent(s).

In addition, parents are required to meet residency requirements, and the child must meet immunisation requirements, be aged 13 years and under, and not be attending secondary school.2

The change to the CCS also introduced the concept of a family co-contribution, so that families pay a portion of their child care fees.3 There are, however, intersections between this and the Additional Child Care Subsidy (ACCS), which tops up the subsidy for families and children facing barriers to accessing affordable child care (see discussion of ACCS below).

Notionally, the CCS is calculated as a direct offset to the charges that would otherwise be paid by the parents. However, in most cases, the actual subsidy paid to a provider is 95 per cent of the amount of CCS the parent is eligible for, as 5 per cent of parents' actual entitlement is initially withheld by government.4 After annual reconciliation, this withheld amount is either then paid to the family or is used to offset any debt they may have to the Commonwealth; in particular, where an underestimation of annual income has resulted in the subsidy being paid at an incorrect and higher rate.

- Key features of CCS are 3 parameters that determine the financial level of subsidy, and one on the quantum of child care that is subject to the subsidy.

- The hourly rate caps are a limit on the rate charged by child care providers that is subject to the subsidy. Where a provider charges a rate less than the cap, families will receive their applicable percentage of the actual fee charged, while where the rate charged is above the cap, the percentage applies to the hourly rate cap.5 As of 1 July 2019, the rate cap was: $11.98 for children below school age and $10.48 an hour for school-aged children in Centre Based Day Care and Outside School Hours Care; $11.10 per hour for Family Day Care, and on a per family basis $32.58 for In Home Care. These caps are to be indexed annually based on the All Groups CPI.

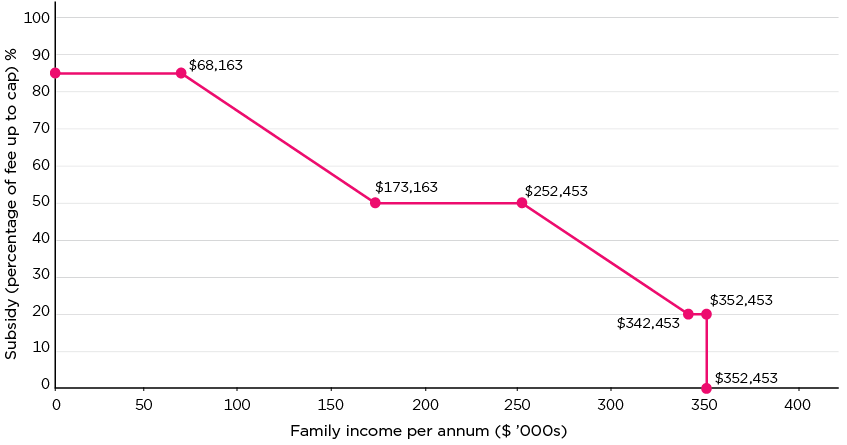

- The percentage of Child Care Subsidy rate is the proportion of the capped fee that is provided as a subsidy and is based on a sliding scale that reduces with family income. For 2019-20 the maximum rate is 85 per cent for families with an income of up to $68,163. The rate of assistance then tapers to 50 per cent at an income of $173,163, remaining at this rate up to a family income of $252,453, before again tapering to a rate of 20 per cent at $342,453, and holding at this rate until family income reaches $352,453.6 Families with an annual income at or above this amount have zero Child Care Subsidy entitlement. (See Figure 2).

Figure 2: Child Care Subsidy, rate of subsidy by family income, 2019-20

Source: Derived from program criteria

- The annual cap is the maximum level of subsidy that will be paid to a family in any one year. For 2019-20 it was $10,373 per child per annum and applies to families with a joint income over $188,163 (and less than $352,453) per annum.7 For families with lower incomes there is no cap.

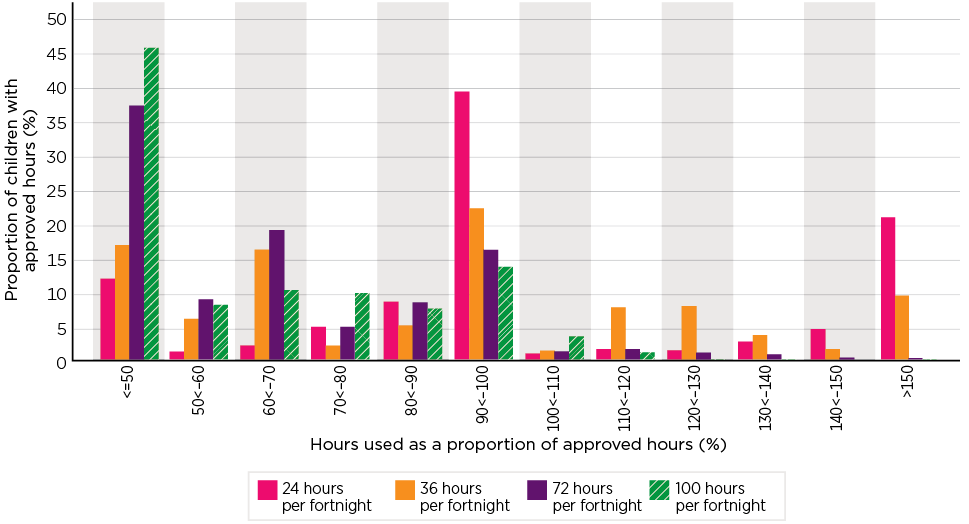

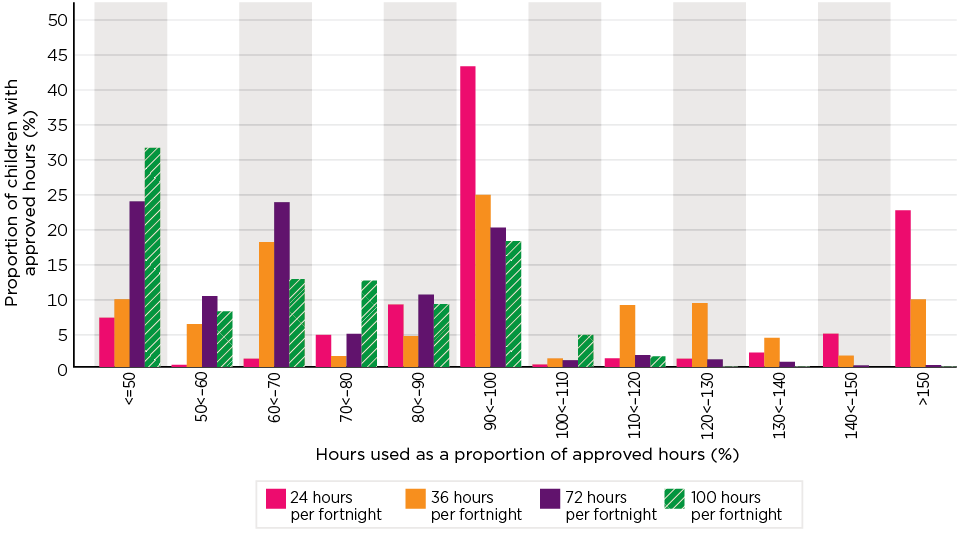

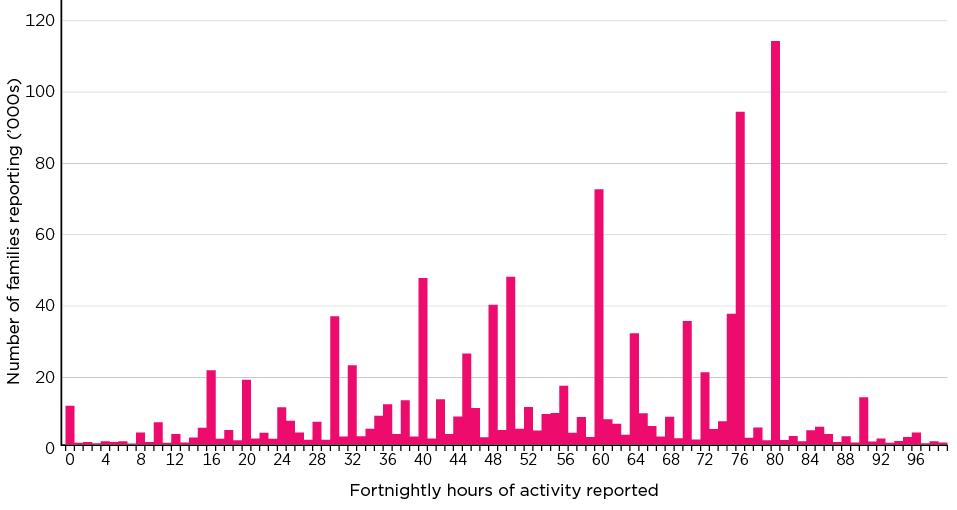

- The activity test operates to restrict the number of hours of Child Care Subsidy a family is entitled to, on a per child per fortnight basis, with the number of hours being determined by the level of 'recognised activity' parents are engaged in. Reflecting the program's focus on participation, and employment in particular, 'recognised activity' includes: paid work; self-employment; unpaid work in a family business; looking for work; volunteering; and studying. When applied to couples, the test is based on the hours of activity of the member with the fewest hours. There are a number of exemptions to the activity requirement for some families. Table 1 illustrates the operation of the activity test and details the main exemptions.

| Step | Hours of approved activity per fortnight | Maximum number of fortnightly hours of subsidy per child |

|---|---|---|

| Persons subject to the activity test | ||

| 1 | 8 hours to 16 hours | 36 hours |

| 2 | More than 16 hours to 48 hours | 72 hours |

| 3 | More than 48 hours | 100 hours |

| Activity test exemptions 8,9 | ||

| Child Care Safety Net - families with an annual income of $68,163 or less who do not meet the activity test | 24 hours | |

| Families who do not meet and are not exempt from the activity test and have a preschool aged child who attends preschool at a centre based day care service (for preschool child only) 10 | 36 hours | |

| Includes: Grandparent principal carers, Disability Support Pensioners and Carer Payment recipients 11 | 100 hours | |

1.1.4 The Child Care Safety Net

The 3 elements of the Child Care Safety Net have been identified above. The specific objective of these is described by the Department as giving 'the most vulnerable and disadvantaged children, as well as those from regional and remote communities, a strong start through access to quality early childhood education and care' (DESE, 2020a).

Additional Child Care Subsidy

The Additional Child Care Subsidy (ACCS) is a top-up payment to the Child Care Subsidy. It provides additional fee assistance to families and children facing barriers in accessing affordable child care. As with the Child Care Subsidy, it is paid to services as an offset to the charge on parents. It has 4 components:

- ACCS (Child Wellbeing) is for children who are at risk of serious abuse or neglect.

- ACCS (Grandparent) supports grandparent primary carers, who receive an income support payment.

- ACCS (Temporary Financial Hardship) is short-term increased child care fee assistance to families who, due to exceptional circumstances, are experiencing significant financial stress with the cost of child care.

- ACCS (Transition to Work) is for parents who are transitioning from income support to work by engaging in work, study or training activities.

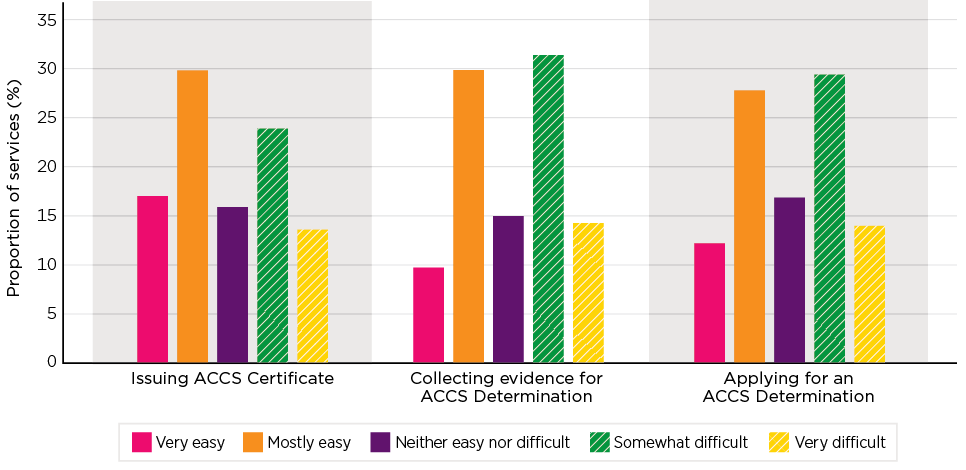

With the exception of the Transition to Work element, the subsidy is equal to the actual fee charged (up to 120 per cent of the hourly rate cap), and is provided for up to 100 hours per fortnight without an activity test. In the case of the Temporary Financial Hardship element, the activity exemption applies for a maximum of 13 weeks per financial hardship event. Under the Transition to Work element, the subsidy is equal to 95 per cent of the actual fee charged (up to a rate equal to 95 per cent of the hourly rate cap), with the number of hours of subsidised care being determined by the individual's activity test result, while the duration of assistance varies with the activity undertaken. In addition, the subsidy can continue for a further 12 weeks if parents gain employment and their income support payments cease. Assistance under the Child Wellbeing provision can be initially granted for 6 weeks on the basis of a certificate issued by the service provider, and for renewable periods of 13 weeks on the basis of a determination by Services Australia.

Inclusion Support Program

The Inclusion Support Program provides support to early childhood and child care services to build their capacity and capability to include children with additional needs in mainstream services. It commenced in July 2016 and replaced the previous Inclusion and Professional Support Program. It aims to increase the proportion of children with additional needs attending mainstream services, improve the capacity of the sector over time and ensure parents of children with additional needs have access to appropriate and inclusive child care services.

Under the program, support is provided to services to enable them to provide inclusive approaches to the provision of child care. This includes, but is not limited to, inclusive practices for children who may have additional needs as they:

- have a disability or developmental delay

- are presenting with challenging behaviours

- have a serious medical or health condition, including mental health

- are presenting with trauma-related behaviours.

And in meeting the needs and requirements of:

- Aboriginal and Torres Strait Islander children

- children from culturally and linguistically diverse backgrounds

- children from refugee or humanitarian backgrounds.

The program operates through 7 state/territory-based Inclusion Agencies (essentially community-based organisations), along with a national Inclusion Development Fund Manager responsible for the management of the Inclusion Development Fund. Support under the Inclusion Support Program is implemented through Inclusion Professionals, employed at the Inclusion Agencies. These agencies undertake a range of roles in providing support to services to generally develop more inclusive approaches, support in the development of Strategic Inclusion Plans, and specific in providing support to assist services address barriers that individual children or groups of children may face. Inclusion Agencies operate equipment libraries for use by services.

There are 4 streams of funding available through the Inclusion Development Fund:

- A subsidy for an additional educator in centre-based services to support ongoing high support needs, prioritised to assisting children with a diagnosed disability.

- A subsidy for immediate/time-limited (up to 8 weeks12) support for centre-based services where there is an immediate barrier to enrolling a child with disability or other additional needs and while an alternative and more stable solution is being determined.

- Top-up support for Family Day Care services where an educator is unable to enrol the maximum number of children they are permitted to because of the demands on the educator of including a child with a disability or high care needs.

- Innovative Solutions Support that allows all service types to receive financial support for creative solutions to address barriers to inclusion.

Services wishing to access financial support through the Inclusion Development Fund must first develop a Strategic Inclusion Plan, except those applying for immediate support. The Strategic Inclusion Plan, developed through collaboration with the Inclusion Agency, outlines the current inclusion practices of the service, barriers to inclusion, and strategies to address those barriers. It may also involve inclusion-related training, development of policies and procedures, sourcing resources from the local community, changes to educators' planning and pedagogy, and modifications to the child care and early learning environment. While part of this evaluation, it is noted that some aspects of the evaluation of the Inclusion Support Program are continuing beyond the scope of this report.

Community Child Care Fund

The Community Child Care Fund (CCCF), the third element of the Child Care Safety Net, provides grants to child care services to help them address barriers to participation. The purpose of the fund, as described in 2017 by the then Minister for Education and Training, was to help 'new and existing services, particularly in rural, regional or vulnerable communities, to reduce the barriers for families to access those services and to increase the supply of places in areas of high, unmet demand' (Birmingham, 2017). More specifically the fund is designed to:

- reduce barriers in accessing child care, in particular for disadvantaged or disadvantaged and vulnerable families and communities

- provide sustainability support for child care services experiencing viability issues

- provide capital support to increase the supply of child care places in areas of high unmet demand.

One specific objective of the program is to assist former Budget Based Funded services to transition to the new child care arrangements.

The program has 3 components:

- CCCF Open Competitive Grants: These are available to eligible, approved child care services and are intended to supplement fee income. Eligibility targets services operating in selected disadvantaged communities, with funding awarded for up to 5 years.

- CCCF Restricted Non-Competitive Grants: To help eligible former Budget Based Funded services (and a small number of other services, see Section 9.7) to build capacity and operate sustainably under the new child care system and support services to increase participation by Aboriginal and Torres Strait Islander children.

- Connected Beginnings: To help Aboriginal and Torres Strait Islander children in areas of high need to be well prepared for school by supporting pregnant Aboriginal and Torres Strait Islander women and Aboriginal and Torres Strait Islander children from birth to school age. Connected Beginnings has operated since July 2016 and provides support to integrate early childhood, maternal and child health, and family support services with schools in a selected number of Aboriginal and Torres Strait Islander communities experiencing disadvantage. This program is jointly funded and implemented by the Federal Departments of Education, Skills and Employment, and of Health, with an annual budget of around $12 million. While Connected Beginnings was separately evaluated, the findings from this have been drawn upon in Chapter 7.

1.1.6 Former child care funding model

Prior to the Child Care Package, there were 2 main forms of child care assistance: the Child Care Benefit (CCB) and Child Care Rebate (CCR).

CCB was a means tested benefit covering up to 50 hours of approved child care use per child per week provided that parents satisfied an activity test of at least 15 hours per week. Families that did not meet the activity test were eligible for CCB for up to 24 hours of child care per child per week. The maximum rate of CCB was $4.30 per hour for a non-school child ($215 for a 50-hour week), and 85 per cent of this rate for a school-aged child. The maximum rate of Child Care Benefit was payable for families with an annual income under $45,114 or families on income support with the rate then reducing up to a limit of $156,914 for a family with one child in care, with this cap increasing with the number of children.

In addition, parents were eligible for CCR. This was a non-means tested payment that provided up to 50 per cent of a family's out-of-pocket child care expenses (after CCB was deducted) to a maximum of $7,613 per child per year. To be eligible for the rebate, parents were required to have had some work, training or study related commitments during the week, although there was no minimum number of hours of such activity required.

There were a range of different payment options available to parents, including whether assistance was paid directly to services as an offset to fees, or was paid to parents periodically or annually. CCB was subject to an annual reconciliation process as it was paid on the basis of estimated income.

These payments were complemented by a range of other assistance including Jobs, Education and Training Child Care Fee Assistance, and Special and Grandparent Child Care Benefit, and the Community Support Program, the In Home Care and Nanny Pilot Programs and the Inclusion and Professional Support Program. Additionally, some child care services, including non-mainstream services in rural, remote and Aboriginal and Torres Strait Islander communities, were directly funded under the Budget Based Funded Program.

1.1.7 Other changes

The introduction of the Child Care Package also involved some structural and related changes.

Service classification

There was a consolidation of types of child care service. Specifically:

- Long Day Care services and Occasional Care Services were classified together as Centre Based Day Care Services.

- Before-School, After-School and Vacation Care services were grouped together as Outside School Hours services (in many cases involving what had been previously treated as 3 separate services even where they were run by the same organisation now being seen as a single service).

- Budget Based Funded (BBF) services were reclassified on the basis of their type of service - typically Centre Based Day Care services or Outside School Hours Care Services.

- The funding changes, along with this classification, also resulted in those children attending these services being recorded in the Child Care IT environment.

For ease of analysis, reporting about services uses the new classification even when reporting on child care prior to July 2018, except where there is specific analysis relevant to one of the old sectors.

In particular, some dedicated analysis of the former BBF services is presented in the report, given the need to explore the transition experiences and outcomes for those services. These services were eligible for CCCF-restricted funding upon transition to the Child Care Subsidy. However, the former BBF services were identified in survey and interview data to allow a focus on them, separate to other services in the Child Care Package that are eligible for CCCF-restricted grant funding.

Program nomenclature and change

Additionally, it is noted that while there appear to be a number of analogues between the old and new program environments, there are frequently considerable differences in the actual nature of the programs. This applies in particular to:

- In Home Care under the new arrangements and the former In Home Care Programme and Nanny Pilot Programme

- Additional Child Care Subsidy (Child Wellbeing/ Grandparents/Temporary Financial Hardship/ Transition to Work) relative to the Jobs, Education and Training Child Care Fee Assistance, and Special and Grandparent Child Care Benefit programs

- the Inclusion Support Program and the former Inclusion and Professional Support Program.

Priority placement

The introduction of the new program saw the removal of the 'Priority of Access Guidelines' that services were required to use to allocate available places. These identified 2 priority groups: Priority 1 - a child at risk of serious abuse or neglect; and Priority 2 - a child of a single parent who satisfies, or of parents who both satisfy, the work, training, study test, and a need to provide within these groups and in enrolling children outside of these groups, priority to: Aboriginal and Torres Strait Islander families; families that include a disabled person; low income families and those on income support; families from a non-English speaking background; socially isolated families; and single parent families.

1.2 The broader environment

The child care program operates in a wider context and there are interactions between it and other interventions. Three of particular note are:

- quality monitoring and assessment

- preschool education

- preschool education

1.2.1 Quality monitoring and assessment

The day-to-day monitoring of the quality of child care provision is a state/territory government responsibility being undertaken by these governments, usually through education departments or agencies. The activity fits into a broader National Quality Framework (NQF) that includes the Australian Children's Education and Care Quality Authority (ACECQA), an independent national authority, that assists governments in administering the framework; National Quality Standards (NQS) that establish a national benchmark for the provision of quality services across 7 areas, which then feed into the national quality rating system under the aegis of ACECQA; and the Education and Care Services National Law (National Law) and related regulations that form a national system for the regulation and enforcement of the NQS. While nationally consistent, this law is legislated individually in each state or territory.

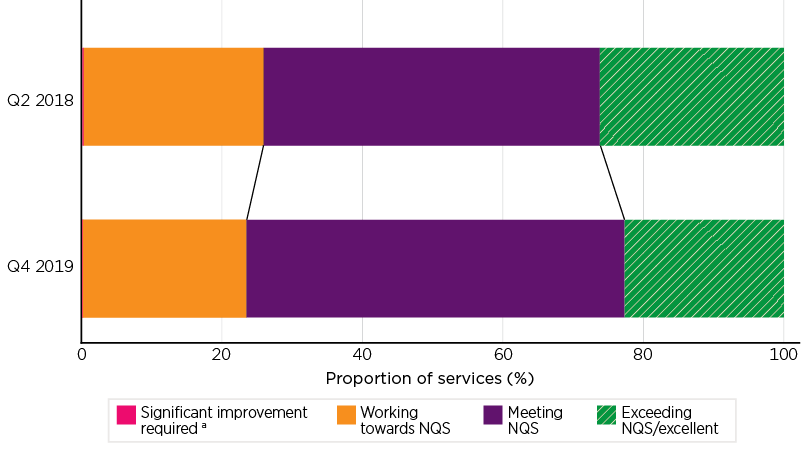

A total of 15,004 Early Childhood Education and Care (ECEC) services were rated under the NQF in Q4 2019. Of these 12,007 were child care services, with the others being preschools and kindergartens. The NQS quality ratings of child care services are considered in Chapter 2.

1.2.2 Preschool

The Australian Early Childhood Education and Care system encompasses both preschool and child care. The relationship between these functions, and the way in which they are delivered, varies significantly across the country. This is illustrated in Table 2. While in some states/territories including South Australia, Western Australia, Tasmania and the Northern Territory, preschool education mainly takes place in the education system, in New South Wales and Queensland it is overwhelmingly delivered in the child care sector, with this largely also being the case in Victoria, although that state also has a strong independent community based preschool sector.

NSW | Vic. | Qld | SA | WA | Tas. | NT | ACT | Aust. | |

|---|---|---|---|---|---|---|---|---|---|

Composition of preschool education delivery (%) | |||||||||

| Government School | 4.1 | 10.7 | 1.9 | 46.1 | 54.7 | 49.6 | 61.5 | 37.2 | 15.9 |

| Private school | 1.8 | 2.6 | 3.1 | 3.2 | 19.8 | 14.8 | 2.9 | 2.6 | 4.5 |

| Community | 22.0 | 31.2 | 23.1 | 0.7 | 0.0 | 0.0 | 0.0 | 0.0 | 19.9 |

| Other | 0.0 | 0.1 | 0.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Mixed provider type | 6.4 | 9.3 | 4.1 | 18.7 | 19.7 | 12.9 | 22.4 | 24.4 | 9.6 |

| Within CBDC | 65.7 | 46.1 | 67.8 | 31.4 | 5.7 | 22.7 | 13.1 | 35.9 | 50.1 |

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

Source: Australian Bureau of Statistics: Preschool Education, Australia, 2019

The nature of preschool provision within child care services was one of the aspects of the pre-transition child care structure examined in the Baseline Survey of Early Learning and Care Services (SELCS)13 undertaken in April 2018. Across services as a whole, excluding Outside School Hours Care where most children were of an older age group, 88.4 per cent of those responding that had children in the preschool age group reported providing a preschool or kindergarten program for children in the year before full-time school. Among Long Day Care services14 this proportion was 93.7 per cent, with a further 3.0 per cent arranging access to a program run externally. Just 3.3 per cent said they made no provision. Across the Family Day Care sector, 35.5 per cent reported having a program, with 33.6 per cent arranging access to an external program, almost a third (30.9 per cent) said they made no provision.

Nationally there is a commitment to 'universal access' to preschool. This seeks to ensure that a quality preschool program is available to all children in the year before full-time school. While states and territories are responsible for the provision of preschool, the Commonwealth provides funding as a contribution to 'top up' arrangements and to ensure families have nationally consistent access to 15 hours per week, or 600 hours per year, in the year before school. This is complemented in those cases where the preschool program is provided in a Centre Based Day Care service by support via the Child Care Subsidy, which allows families who do not meet the activity test to obtain 36 hours of subsidised care per fortnight for a preschool-aged child who attends preschool at a centre-based day care service. Parents are still required to meet the income test to obtain this assistance.15

As noted above, the role of ACECQA extends across both the child care and preschool sectors.

1.2.3 NDIS

Inclusion is a key objective of the Australian child care system. Under the Package this is supported by access to the Additional Child Care Subsidy, the Inclusion Support Program and the In Home Care program. Children who have an impairment, serious illness or condition that is likely to be permanent are also potentially eligible for support through the National Disability Insurance Scheme (NDIS). A specific objective of the NDIS is investing in people with disability early to improve their outcomes later in life.

The NDIS has been rolled out across Australia, commencing in 2013, including from the rolling out of the specific Early Childhood Early Intervention (ECEI) approach that began in 2016. This measure supports children aged 0-6 years who have a developmental delay or disability and their families and/or carers, with a focus on providing supports to families to help children develop the skills they need to take part in daily activities and achieve the best possible outcomes throughout their life. The approach is currently under review and it is anticipated that an implementation reset process will be finished by mid-2021.

With respect to child care, the focus of the NDIS is on providing 'individualised supports to enable a child to attend an early learning service'. The program approach, however, limits this to those 'situations where a child has very significant and complex care needs that are beyond a reasonable expectation for child care services to provide. For example, a child requiring ventilation, which must be supervised by a trained carer or nurse' (NDIS, 2014). With the exception of these specific circumstances, the early childhood and child care services have responsibility for the education and care needs of children, including children with disability or developmental delay.

1.3 The evaluation

The Australian Institute of Family Studies in association with the Social Research Centre, the UNSW Social Policy Research Centre and the ANU Centre for Social Research and Methods were commissioned by the Australian Government Department of Education, Skills and Employment to undertake an independent evaluation of the new Child Care Package. The evaluation commenced in December 2017, prior to the introduction of the Package, and was expected to continue until June 2021. The In Home Care program and the Inclusion Support Program, in addition to being within the overall evaluation scope, are subject to separate reporting, with as noted some of the Inclusion Support Program evaluation continuing past the date of this report.

As noted in the introduction, the evaluation was disrupted by COVID-19 and associated restrictions, as well as changes to government assistance to families and the child care sector, and as a consequence this report only considers outcomes to the end of 2019. This focus, while bringing some constraints as to what was able to be done and limiting the capacity to identify longer-term consequences of the introduction of the Package, ensures that the outcomes and impacts reported on are those that relate to the Package itself, and not the consequences of these other interventions, nor the evolving circumstances in which services operate.

In particular, it is noted that because of disruptions to the sector, it was not possible to undertake the third wave of the Services Survey that was designed to better understand the impact of the Package on service operations, rather than the more transitional experiences that dominated the earlier waves.

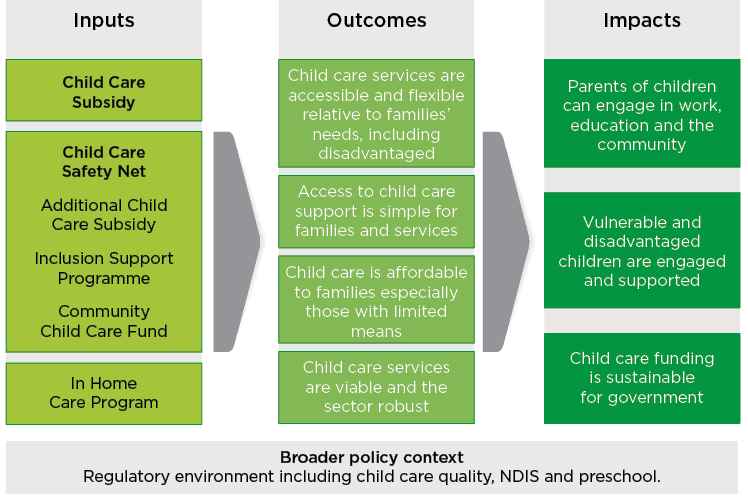

The evaluation is guided by the Evaluation Framework that was agreed with the Department.16 The Evaluation Framework, as detailed in Figure 3, sets out 4 key outcomes and 3 key impacts against which the new Child Care Package is being evaluated. These reflect the policy objectives set by the government for the Package. In large part, they relate to medium to long term effects of the Package and its consequences for families, children and the child care sector.

Figure 3: Evaluation Framework

1.3.1 The evaluation approach

The primary focus of the evaluation, as detailed in the evaluation framework, is on the outcomes and impacts of the Child Care Package. This contrasts with other evaluative tasks, such as process or implementation evaluation, that are more concerned with the way in which programs are implemented and the extent to which implementation has occurred as intended and whether the program has been fully and properly implemented in accord with its guidelines and procedures. Notwithstanding this focus, Chapter 10 addresses questions of implementation in the context of the transition to the new program.

In undertaking the evaluation, it is noted that a number of balances have needed to be struck in the approach. These include the degree to which comparative or absolute outcomes and impacts are considered, the effective weighting of positive and negative outcomes, the extent to which outcomes and impacts can be attributed to the policy and program changes, and the degree to which the time scale of this report and the data available to the evaluation can fully identify the effects of the program. Additionally, there are questions concerning the nature and role of child care provision that are not necessarily wholly reflected in the evaluation framework. These are considered further below.

Comparative and absolute outcomes

In large part, the focus of the evaluation is comparative. That is, comparing the outcomes and impacts being achieved following the introduction of the Package, relative to those under the previous arrangements. In terms of affordability, for example, this is a focus on whether child care is more affordable to families under the CCS than it was under CCB/CCR. This approach reflects the fact that few of the concepts can be measured in purely absolute terms, or where the metrics of an absolute measure - for example, what constitutes 'affordable child care' - tend to be value laden.

At the same time, consideration of absolute outcomes in some cases is also important. For example, treating access in purely relative terms, when it comes to questions such as access for disadvantaged groups, ignores the important social imperative to ensure that children at risk have access to appropriate child care and related services.

Balancing of outcomes

Some aspects of the new child care policy have the potential to have differential impacts across the population, benefiting some, and disadvantaging others, in either absolute or relative terms. In the evaluation both of these are important, and care needs to be exercised in not just focusing on average effects but also the distribution of these. Such a focus, however, tends to limit the ability to draw concise, as opposed to more extended, nuanced findings that take account of these diversities. While, alternatively, some summative measures can be considered, these involve a range of potential value judgements about how to weigh gains and losses, including the extent to which these may be recorded by quite different population subgroups. In some cases, though, it is noted that program objectives, such as the refocusing of assistance from higher income families to those on lower and middle incomes, provides a normative weighting for such considerations.

Attribution

Attributing changes in outcomes to the effect of the Child Care Package can be problematic. For example, parents' perceptions of affordability may be affected by changes in their income and in other expenses - as well as, more widely, by perceptions of their financial circumstances and opportunities. Similarly, changes in employment can result from changes in the labour market and the demand for labour, as well as other policies such as the rates and conditions related to income support, and shifts in attitudes relating to parental workforce engagement. Disentangling the roles of each of these factors is difficult; in particular, as there is no counterfactual, control population that can be used as a reference point, as the policy applies to the entire parental population. While not all parents use the assistance, given that take-up is impacted by individual circumstances, attitudes and aspirations, these operate effectively as a selection effect that renders non-user parents unsuitable as a comparator. Additionally, as will be discussed in Chapter 8, the impact of the program needs to be considered across parents as a whole.

More widely, other policies, including universal access to preschool and its interaction with different state preschool systems, the introduction of the National Disability Insurance Scheme, and a wide range of other initiatives all, in turn, also have impacts on the outcomes of populations of children and families who use child care. The interaction of these confound any attempt to attribute changes to child care programs alone.

Time scale

The evaluation is considering the impact of the introduction of the Package over an 18-month period, with much analysis, due to potential seasonal effects, the more limited focus of the November 2019 DESE ORIMA parent survey and the curtailment of the evaluation specific services survey, being restricted to a 12-month period. Little information is available to assess whether this time scale is sufficient to fully identify the impact of the program. Two potentially sensitive dimensions relate to the impact on labour force engagement where people may either plan an engagement trajectory over time or where changes in their engagement are triggered by external factors, such as a job loss or a specific job offer.

The role of child care

As identified earlier, the rationale for the Package was described as having the objective 'to help parents who want to work, or who want to work more, while still focusing on early childhood education'. The 2 elements of this statement reflect 2 facets of child care. Given the evaluation framework, and the overall legislative intent as described by the Department 'that, in relation to early learning and child care, the primary role of the Australian Government is to provide families with financial assistance to help cover the cost of child care, while supporting workforce participation' (DESE, 2020b, p. 2) the focus of the evaluation is primarily on the first, and even to the extent to which questions such as access are considered, the orientation of the framework is on achieving access - not what access provides.

We address this further in our concluding chapter.

Terminology

In describing the sector, we have chosen to use the language of 'child care' rather than the alternative of 'early childhood education and care'. This decision was based on 3 grounds:

- the terminology of the main program element, the 'Child Care Subsidy', and of the legislation Family Assistance Legislation Amendment (Jobs for Families Child Care Package) Act 2017

- the extent to which the evaluation, as noted above, is directed at the child care role, rather than the content of early childhood education

- the wider scope of the concept of 'early childhood education and care' that encompasses the preschool sector, and indeed some would also argue the early years of formal schooling.

Data and analysis

The evaluation draws very extensively upon administrative data provided by the Department; in particular, weekly records of child care use, surveys of parents, including one of the Department's surveys as well as those undertaken by the consortium, 2 major waves of surveys of services, a series of case studies, and extensive consultations. From these sources the evaluation has had a rich collection of quantitative and qualitative data that is reported on here. Data sources are described in detail in Appendix 1.

In addition to the direct reporting and interpretation of this data, the evaluation also undertook a major modelling exercise, reported on in Chapter 4, of the impact of the package on affordability.

1.3.2 Structure of report

This report is largely structured around the outcomes and impacts identified in the framework, specifically:

- Chapter 2 'Child Care in Australia' provides an overview of the child care system and of the state of child care at the end of 2019.

- Chapter 3 'Simplicity' addresses the second identified outcome - that of the simplicity of the system; in particular, for parents and services.

- Chapter 4 'Child Care costs, subsidies and affordability' responds to the third identified outcome - the affordability of child care. This also has implications for the third impact - that of the sustainability of the child care funding, although we note that the substantive consideration of this is for government, which needs to weigh up decisions on priorities both in expenditures and revenues.

- Chapter 5 'Flexibility' addresses the second half of the first outcome.

- Chapter 6 'Access' encompasses the second half of the first outcome.

- Chapter 7 'Vulnerable' focuses on the second impact, as well as aspects of these groups' experiences as identified in the first and third outcomes.

- Chapter 8 'Employment participation impacts' addresses the first impact. It also covers some of the specific aspects of the safety net programs, including ACCS.

- Chapter 9 'Viability and robustness of the industry sector' addresses the fourth outcome and informs on the third impact. The Chapter also discusses the operation of the CCCF and the impact of compliance activity.

- Chapter 10 'The transition to the Child Care Package', in contrast to these other chapters that are concerned with program outcomes and impacts, focuses on the processes of the transition, the experiences of services and families and of the policy responses to these.

- Chapter 11 'Conclusions and recommendations' presents the conclusions of the evaluation and recommendations for consideration drawn from these.

The evaluation framework also identified a series of cross-cutting issues, including the different sectors of child care provision, geographic outcomes, and the experiences of different families, as well as the effect of different program elements. In general, these are discussed across the chapters.

Appendix 1 'Evaluation process and data' reports more fully on the evaluation activities undertaken and the data sources drawn on, including those used in this report.

1 The Department of Education and Training became the Department of Education on 29 May 2019, then changed to the Department of Education, Skills and Employment (DESE) on 1 February 2020. In this report the Department, and its predecessors, is referred to as DESE or the Department.

2 In addition, where a child may be cared for by others, the person applying for the subsidy needs to meet a requirement with respect to the level of care that they provide to the child.

3 In the explanatory memorandum for the original Jobs for Families and Child Care Package legislation this was described as 'a provision that obliges approved providers to ensure that they recover, from individuals, the difference between a fee reduction (made available through CCS or ACCS) and the actual fee charged to the individuals, where there is a difference. The CCS payment is designed with a concept of co-contribution to the cost of child care. This provision intends to address an issue that has arisen with CCB where some child care services did not actually pursue the difference between fee reductions and actual fee charged to the individual' (Porter, 2017b, p. 87). In the accompanying Regulation Impact Statement (Department of Education and Training, 2015a), the Department indicated 'A minimum co-contribution from all child care users was seen by stakeholders as acceptable, fair and necessary. A co-contribution can encourage parents to be conscious of the fees charged and help keep downward pressure on child care fees' (p. 43).

4 Parents can apply to have this proportion increased.

5 Notwithstanding the introduction of the hourly rate cap, child care fee assistance continues to be calculated on the length of the session of care the parent is charged for, and not time actually attended. Where services charge by the session the hourly rate used to determine the relationship with the fee cap is derived by dividing the session charge by the session length.

6 In 2018-19 these values were $66,958, $171,958, $251,248, $341,248 and $351,248 respectively.

7 In 2018-19 the cap was $10,190 and applied to incomes above $186,958.

8 This is a summary of exemptions only. In some cases, exemptions apply to a specific child and, in other cases, to all children. It is further noted than in 2 parent families, where one person has an exemption, the hours of subsidised care for the family is based on the person with the lowest activity test result.

9 In exceptional circumstances families can make an application to Centrelink that it would be unreasonable for them in their circumstances to satisfy the activity test. This provision also allows for a subsidy for more than 100 hours per fortnight.

10 See Section 1.2.2 for further discussion of this provision.

11 The Department (Department of Education and Training, 2018a) indicates that people in the following circumstances are exempt from the activity test:

- people with disability or impairment, including those who receive Disability Support Pension or an invalidity service pension or who have been diagnosed by a registered medical practitioner or clinical psychologist as impaired to a significant degree

- people living or travelling outside Australia (the individual claiming Child Care Subsidy will usually be exempt for up to 6 weeks)

- recipients of Newstart, Youth Allowance (jobseeker), Parenting Payment or Special Benefit, with an exemption from mutual obligation requirements (with some exceptions)

- being in gaol or psychiatric confinement due to being charged with an offence