Financial support between family members

Overview

This research snapshot looks at some of the ways that family members provide financial support to one another, and how giving and receiving financial support differs across life stages.

Financial support in this research snapshot refers to the support between adult family members who may not live together, not the financial provision for children (under 15 years of age) or sharing financial resources between partners.

Financial support between family members can take various forms. It can involve occasional or regular payments, paying for small or large purchases (including housing1), or an in-kind approach (e.g. paying bills).

Financial help is often valued during times of transition; for example, when there are housing or care needs and during times of financial difficulty, as can occur with accidents, illness or job loss.

Using the data from a range of sources, including the Longitudinal Study of Australian Children and the Household, Income and Labour Dynamics of Australia (see 'Acknowledgements' for details), this snapshot focuses on the extent to which people report giving and receiving financial support:

- levels of giving and receiving financial support

- financial support in the time facing financial difficulty

- financial support for young people during the pandemic.

It also looks at general attitudes towards inter-generational support.

Key messages

-

Family is an important source of financial support in times of need, with one-fifth of respondents in the Families in Australia Survey (2021) reporting having received occasional and or regular financial support in the past year. Such support tends to flow from older to younger generations.

-

Financial support from family when facing financial difficulties is especially important for young people. Nearly one in five respondents aged 20-21 years reported needing more financial help from family during the early stage of the pandemic in 2020.

-

Overall, the endorsement of intergenerational support remains strong in Australia, with one-half of participants in the Families in Australia Survey (2021) endorsing the provision of financial support between family members in times of financial need.

Giving and receiving financial support

Overall patterns of financial support

In the Families in Australia Survey of November-December 2021, 3% of survey participants said they regularly received financial help from family members they do not live with, and 18% said they occasionally received financial help. Overall, 21% either regularly or occasionally received financial help.

Against this, 12% said they regularly gave financial help to family members and 37% said they occasionally gave it. Together, 49% gave financial support occasionally and or regularly.

This difference between giving and receiving rates is partly related to the survey under-representing younger people. However, more generally, research (e.g. Mandemakers & Dykstra, 2008) has found that people tend to over-report giving help and under-report receiving it.

Another survey, the HILDA survey of 2020 (for the 2019/20 financial year) found that of those aged 15 years or older:

- 6.8% had received a payment from a parent

- 1.5% had received an inheritance or bequest

- 0.8% had received a payment from someone not in the same household

- 8.6% had received at least one of these forms of support.

Financial support by age

The giving and receiving of financial help between family members is strongly related to age (see Figure 1). For instance, in the Families in Australia Survey, November-December 2021, 39% of 18-29 year olds reported they received occasional or regular financial help - compared with only 14% of people aged 60 or more.

On the other hand, 62% of those aged 60 years and over occasionally or regularly gave financial help - compared with 33% of 18-29 year olds.

Figure 1: Proportion receiving financial help from family and giving financial help to family, by age

Source: Families in Australia Survey, November-December 2021

A similar story emerges from the 2019-20 HILDA data. Financial transfer from parents was reported by:

- 44% of 15-19 year olds

- 16% of 20-24 year olds

- 9% of 25-29 year olds

- 5% of 30-34 year olds

- less than 2% of those aged 35 or older.

Financial transfer from parents falls swiftly as their children age; for example, from 15% of 22 year olds to 9% of 24 year olds.

The proportions vary from year to year but the general pattern is a fall from around half of 15 year olds, to one in six 22 year olds, to around one in ten 24-year olds.

Amount of financial support

According to the HILDA data, in each of the years from 2016 to 2020, the median amount from parents to their adult children in the previous financial year was $1,000. For those aged 15-24 years the median was $500; for those over 24 it was $5,000 (see Table 1).

Inheritance/bequest amounts tend to be more substantial, although rarer. In 2019/20, the median inheritance/bequest amount in the previous financial year was $66,000.

Table 1 also provides a perspective of family financial support by comparing the extent and amount of government income support that young people received. An interesting finding is that very few people reported receiving payments from parents as well as from the government, such that these different forms of financial assistance are typically going to different groups of people.

For all age groups, the value of the government transfers is substantially greater than that of parental payments - but particularly for the group aged 15-24 years.

| 15-24 years | 25-34 years | 35 years and older | |

|---|---|---|---|

| Percentage received any in 2019/20 | |||

| Parental payments (transfers) | 29.6 | 7.1 | 1.5 |

| Government payments (transfers) | 20.1 | 30.4 | 47.2 |

| Parental and government payments | 2.5 | 1.7 | <0.0 |

| Inheritance or bequest | <1.0 | 1.2 | 1.7 |

| From another person outside the household | 3.4 | <1.0 | <1.0 |

| Median amount in 2019/20 ($) excluding non-recipients | |||

| Parental payments (transfers) | 500 | 5,000 | 5,000 |

| Government payments (transfers) | 9,750 | 9,668 | 13,750 |

Notes: Median amounts for inheritance/bequest and from another person outside the household are not shown as the sample sizes were too small to examine these statistics by age. There were also too few inheritances/bequests to tell if the age of the recipient made a difference to the value.

Source: Derived from HILDA Wave 20, cross-sectional weights

Family support in the time of financial difficulty

Family is a very common source of financial help and emergency money. The Australian Bureau of Statistics reported that in the December 2020 quarter, about one in 10 people had gone to family or friends for financial help in the past year.

Comments from Families in Australia Survey participants (November-December 2021) show some of the ways that family members help each other:

I have financially supported my daughter for 18 months or more as she lives alone, was unemployed and could not afford rent and living expenses from government support.

71-year-old female

Child who lives with me has taken over paying for all food/shopping requirements, which helps when unemployed.

63-year-old female

In the past year, the most important help was the loan of some money from a family member so I could buy a much-needed car at a time when my income was reduced.

69-year-old female

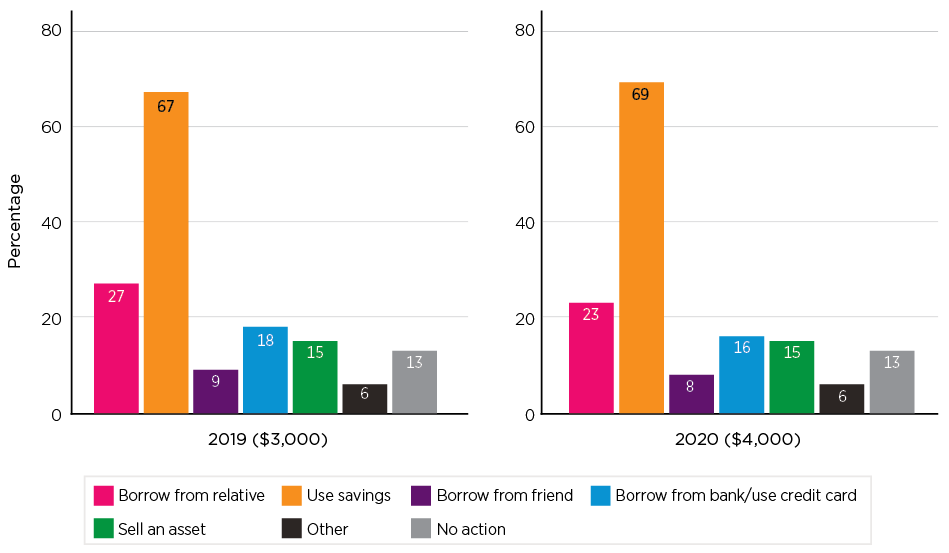

In the HILDA surveys of 2019 and 2020, survey participants were asked about financial actions they would take if they needed an emergency sum of money (see Figure 3; in 2019 the sum was $3,000, in 2020 it was $4,000).2

- The most common expected financial action at each time was to use savings (67% in 2019 and 69% in 2020).

- The second-most common expected action was that they would borrow money from a relative (27% in 2019 and 23% in 2020).

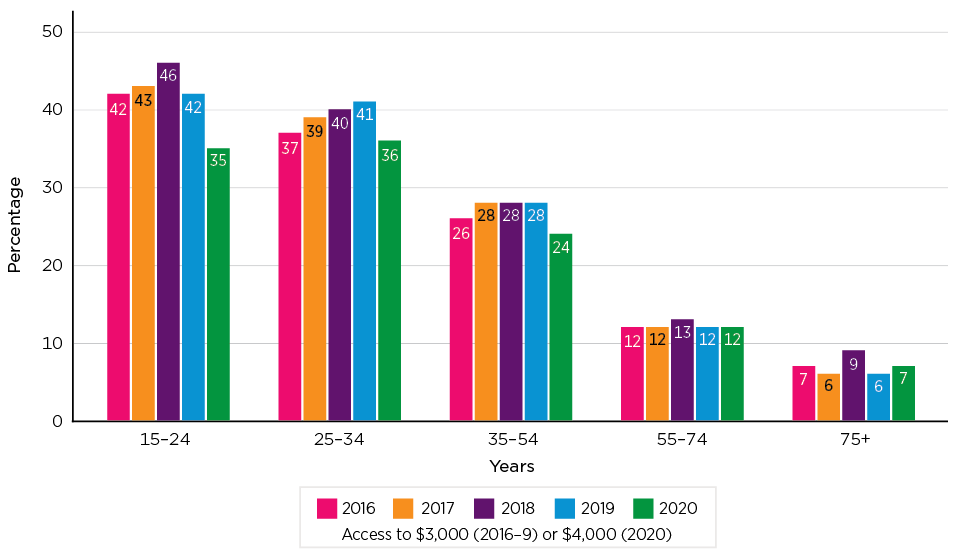

Younger people were most likely to go to a relative for emergency money. Figure 2 shows the proportion that would borrow emergency money from a relative, by age. It shows data from 2016 onwards, when the emergency money question was asked.

Figure 2: Financial actions to raise emergency money

Figure 3: Proportion reporting they would go to a relative for emergency money

Note: The questions ask about financial actions that would be taken if $3,000/$4,000 were needed. Those who said they could not raise $3,000/$4,000 are included as not going to relative for help.

Source: HILDA Waves 16 to 20, self-complete questionnaire, weighted (Wave 20 release)

Financial support for young people during the COVID-19 pandemic

The COVID-19 pandemic and associated restrictions had financial impacts on some people, through changes to employment, job losses, standdowns and reduced working hours.3 In this section we consider how young people's financial help from parents may have changed with the onset of the pandemic.

Data collected for LSAC in late 2020 captured some insights about young people's need for financial support from parents, and how it had changed since the start of the COVID-19 restrictions.4 At this time, the younger (B) cohort of LSAC was aged 16-17 years and the older (K) cohort was aged 20-21 years.

Among these two cohorts, just over a half indicated they had not needed financial help from their parents or other family members in the previous year (57% of 16-17 year olds and 54% of 20-21 year olds). A very small percentage (around 4%) indicated they needed less financial help than usual during the restrictions.

One in five (19%) of the 20-21 year olds reported needing more financial help from family, compared to one in 10 (9%) of the 16-17 year olds.

Table 2 shows that not being employed made the 20-21 year olds nearly twice as likely (29% vs 16%) to need help during the restrictions.5

| 16-17 year olds | 20-21 year olds | |||

|---|---|---|---|---|

| Total % | Employed % | Not employed % | Total % | |

| Financial support not needed in past 12 months | 56.9 | 58.1 | 42.2 | 54.3 |

| Needed more financial support in COVID-19 restriction period | 8.9 | 15.8 | 28.7 | 18.7 |

| No change in financial support needed in COVID-19 restriction period | 30.3 | 22.5 | 23.5 | 22.7 |

| Needed less financial support in COVID-19 restriction period | 3.9 | 3.7 | 5.5 | 4.1 |

| Total, % | 100.0 | 100.0 | 100.0 | 100.0 |

| Total, n | 1,503 | 1,002 | 289 | 1,291 |

Notes: Employment status is as at the time of the survey. Unweighted percentages. Percentages may not sum to 100.0 due to rounding.

Source: LSAC, Wave 9C1 (2020)

Attitudes toward financial supports

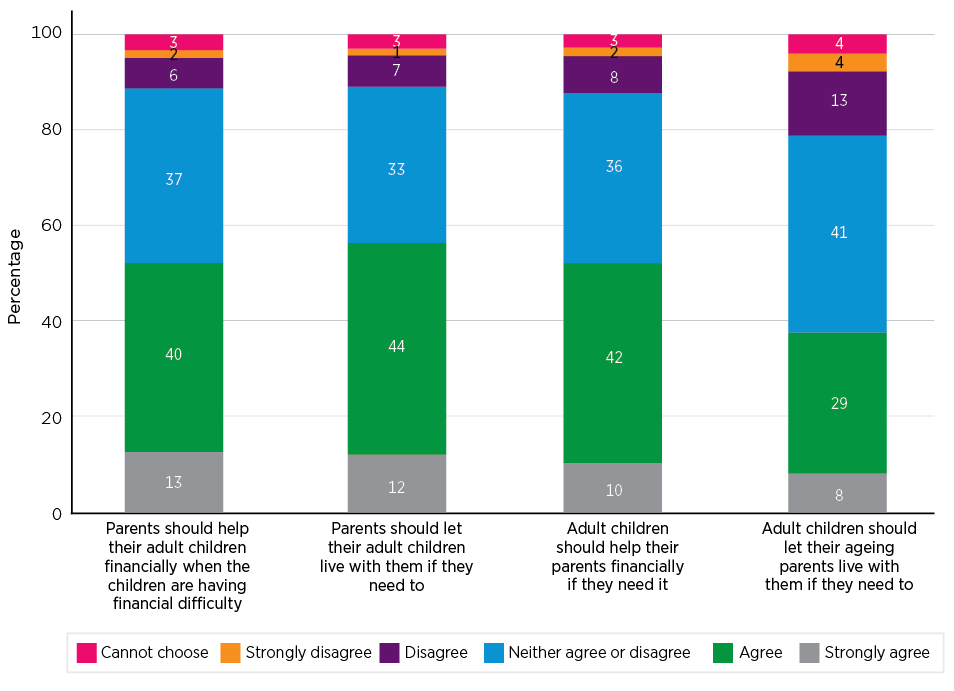

In the Families in Australia Survey in November-December 2021, participants were asked whether they agreed that grown-up children should support ageing parents if needed. Participants were also asked whether they agreed that parents should support grown-up children in times of financial need. See Figure 4.

Out of 5,467 survey respondents, about half of the participants agreed that support should be given to ageing parents and about half also agreed that support should be given to grown-up children.

- 45% agreed (or strongly agreed) to one or both questions about supporting parents as well as one or both questions about supporting grown-up children

- 13% agreed (or strongly agreed) to one or both questions about supporting grown-up children but neither of the ones about supporting ageing parents

- 6% agreed (or strongly agreed) to one or both of the questions about supporting ageing parents but neither of the ones about supporting grown-up children.

If responses to all four questions are explored together, about one in five agreed (or strongly agreed) with all four statements.

The least likely to agree to all four statements were those aged 60 or more. Compared to younger age groups, these participants were not so likely to agree that adult children should let their ageing parents live with them if needed.

There was a strong 'it depends' element to many of the comments. The nature of the relationship between the adult children and their parents was seen to matter, along with factors such as the health or caring needs of one of the family members.

I feel uncomfortable saying kids or parents should support each other in particular ways. Families are too varied for me to want to take a strong stand on how they must act.

25-year-old female

It should depend on their means to be able to support others as well as where they are at in life.

36-year-old female

I think if adult children require financial assistance it should be given as a loan, not a gift, or they will remain financially dependent and live outside of their own means. If they need to move back home they should contribute financially and help around the house. In the same way, I have accrued sufficient superannuation to be sure that I am not a financial burden on my children in my old age, but I would like to live with my daughter when the time comes.

51-year-old female

Figure 4: Agreement about the support between adult children and parents

Source: Families in Australia Survey, November-December 2021

References

Cigdem-Bayram, M., Whelan, S., & Wood, G. (2018). The Bank of Mum & Dad: Intergenerational transfers and first-time homeownership in Australia. Paper presented at the 35th IARIW General Conference, Copenhagen, Denmark.

Mandemakers, J. J., & Dykstra, P. A. (2008). Discrepancies in parent's and adult child's reports of support and contact. Journal of Marriage and Family, 70(2), 495-506.

1 There is very little information on the extent to which people have financial help from parents in their home purchase. An analysis by Cigdem-Bayram, Whelan, and Wood (2018) used the longitudinal HILDA data to demonstrate that bequests from parents were associated with higher rates of home ownership. Information on 'the Bank of Mum and Dad' is published by financial institutions, suggesting parents are an important lender for this purpose. See What is the Bank of Mum and Dad? | Savings.com.au

2 Those who reported they did not think they could obtain this amount of money were coded as not taking any of the actions.

3 See Life during COVID-19: Financial wellbeing and COVID-19.

4 Participants were asked to reflect on circumstances experienced during the coronavirus restriction period, which was defined as the period when governments first put in place restrictions and recommendations designed to curb the spread of COVID-19. For most Australians, this was between March and May 2020. If they reported having needed some financial support from parents in the past year they were asked, 'Since the beginning of the coronavirus restriction period, how much support have you needed from your parent(s) or other family members, for financial support (e.g. giving/loaning borrowing money, or helping you purchase goods, paying bills/fees) compared to usual?' These data are sourced from the 9C1 release of LSAC. See data note at the end of the report.

5 The 20-21 year olds' reports of changing need for financial support were also compared according to whether they were living independently or with parents but responses did not vary significantly for these two groups.

Acknowledgments

This research snapshot draws on a number of data sources, including:

- AIFS' Families in Australia Survey

- AIFS' Growing up in Australia: The Longitudinal Study of Australian Children (LSAC)

- the University of Melbourne's Household Income and Labour Dynamics in Australia (HILDA) Survey

- the Australian Bureau of Statistics' Survey of General Community

The authors wish to thank Tracy Evans-Whip and Jennifer Prattley for the contribution of the LSAC 9C1 data, and the AIFS Communications Team.

Featured image: © GettyImages/Daria Nipot

Baxter, J., & Carroll, M. (2022). Financial support between family members (Research snapshot). Melbourne: Australian Institute of Family Studies.

16 November 2022